Surfactants Monthly - June 2026

Surfactants Monthly – June 2026

How was last month’s vacation – you ask?. Brilliant. We cycled from Pittsburgh, PA from Washington DC on the Great Allegheny Passage and C&O Canal cycling paths; 330 miles, 7 days. We passed through many fascinating towns which, while geographically may be considered mid-Atlantic / Eastern Seaboard, culturally – very far from it.

Now we focus on our next in-person get-together in Kuala Lumpur for the 12th ICIS Asian Surfactants Conference (https://events.icis.com/website/14105/) , co-produced by me on October 27 – 28th, with the one day training on October 26th. You should do the training if you haven’t already. There are many alums of the course out there now in positions of considerable responsibility.

End of Commercials.

The News:

Many people are saying we provide too much information here in the blog and we are literally spoiling the readers – so I’ll try and keep things tight this month…

Mid month Argentina’s YPF announced they were shutting down their LAB and LAS production capacity. The 55,000 MT/yr LAB plant will close along with downstream LAS production, by end of year. YPF will continue to produce n-paraffins at the site. As reported previously in the blog, paraffins are expected to be the bottleneck in the LAS value chain going forward, so maybe this is the right move. Maybe, and I am strictly just speculating here, maybe they got an offer they couldn't refuse for all of their paraffin output for the next 10 years or something like that? You guys know how to use the tip line by now I think…

Accepting long distance calls from various hemispheres (image by Grok)

Interesting, ICIS believes this may be the latest in a recent succession of plant closures in the Americas due to global weakening of demand across the board. Read that article here . What do you think. ?

Big news outta Syensqo. The Wall Street Journal says that the company is “reviewing strategic options” for the Performance and Care (P&C) business. This is code for – “it’s up for sale”. They want to be a pureplay specialty materials company and the P&C business, which is mainly surfactants related doesn't fit. P&C is about Euros 2 Billion in sales about a third of the company and generates about a quarter of the EBITDA (2025 figures). P&C itself is divided into Novecare (which is super-heavy in surfactants) and what they call Technology Solutions which seems to be mainly mining chemicals (also including some surfactants). I expect they’ve retained an I-Banker, but they have not said who. Anyone who knows should get over to the tipline, if, of course, that would not be betraying any duties of confidentiality.

Call from Belgium or Princeton, NJ or wherever… (image by Grok)

I have some thoughts. First off – can someone explain why they spun off the old McIntyre business which now competes in amphoterics and alkoxylates with Syensqo (under the ownership of Samyang of Korea)? How did that make any sense – especially when, in their reports and presentations they still tout leadership in mild chemicals? Second off, the current CEO, Mike Radossich was, prior to his promotion, heading up Novecare and so he clearly concluded during his tenure there that he’d taken it as far as it would go and it would never match the Materials division’s 28% EBITDA margins before corporate charges (P&C did 18% last year). There have also been other attempts at restructuring Novevcare over the years and so you could say they tried a number of times but weren’t satisfied with the results. Fair enough. That’s an owners prerogative.

For graduates of my surfactants business essentials course, I think what’s been happening at P&C is this:

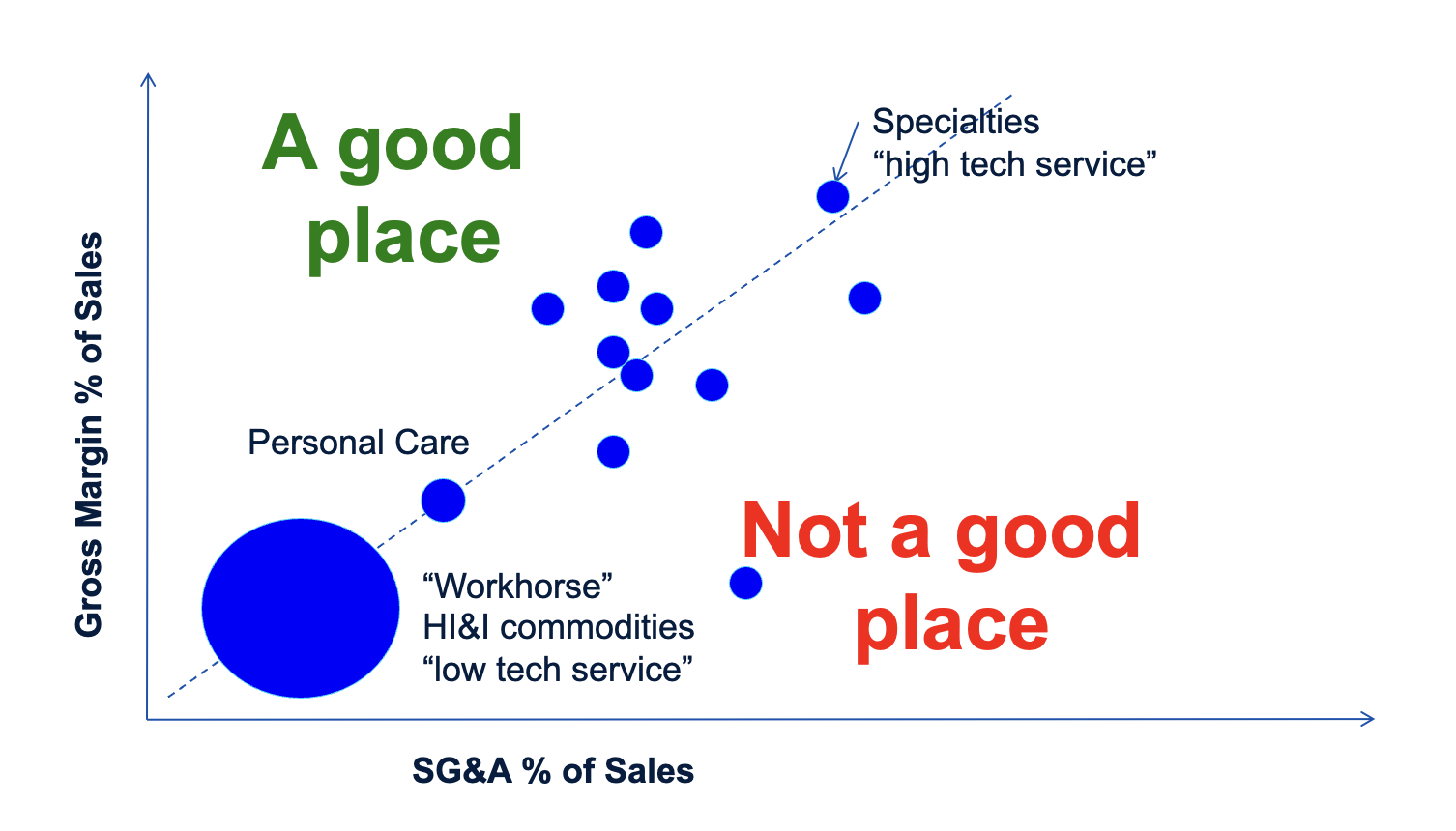

Remember this one?

Blue dots have been drifting down under the gravitational force of competition. If you don’t know what I’m talking about – enroll in the course in October!

So who is a logical new owner of P&C? I can think of a good fit for the mining piece and maybe that goes separately. For Novecare there is a plethora (this grammar is correct so don’t write in!) of obvious suitors and one or two not so obvious ones. I’m not sure I should list them here but if you want to talk about it, get in touch – tipline or otherwise. I mean, for sure, a big PE with some chemicals experience could do OK with it at the right price. Then, with the usual and unusual suspects, a banker could run a very decent process. I guess we’ll see. On a final note, I’ll say that I’ve known some good, conscientious, expert and insightful folks over the years at Syensqo and predecessors going back to the early 90’s. I hope the business lands somewhere they are appreciated.

Fatty Acid Anti-Dumping: This is a story still in progress form last months’ blog, but I’ve had a bit of feedback from folks, let’s say, without blowing any covers, who are in the value chain. One is not optimistic about a fair result for importers, given past history and the current political environment. Another was keen to emphasize that the Dept of Commerce has not yet had the opportunity to evaluate input and data from importers. So – there you have it. We’ll see. As a reminder, here is the upcoming timetable as published in last month’s blog.

• ~July 17, 2026: CVD preliminary determinations and first cash-deposit rates.

• ~July 27, 2026 (subject to extension to mid-September): AD preliminary determinations.

• Q1–Q2 2027: Final DOC determinations and ITC final injury vote.

The great Craig Bettenhausen wrote a great article in the great Chemical and Engineering News about solid detergents here (https://cen.acs.org/business/specialty-chemicals/solid-detergents-back-sheets-tiles/104/web/2026/06?sc=260603_news_eng_cennews_cen&elqE=17640&elqC=10303 ). Get over there and read it. Some interesting snippets:

•In the US laundry detergent market at $11.4 billion sales /year, detergent sheets were the primary laundry detergent for 21% of US households in 2025, according to Mintel. This seems high to me. Apparently it comes from a survey of 1,793 US adults who did laundry in March 2025). The full split came out - liquid 58%, single-dose pods 31%, powder 23%, sheets 21%. Anyone else find the first 3 about right-ish but sheets over-represented?

•Apparently retail shelf presence understates sheet/tile adoption as the growth tied to home-delivery purchasing of cleaning products. (still not quite buying it…)

•The article talks a lot about Tide Evo to which we’ve given more than enough free publicity already in the blog. It discusses PVA and the discussion around that.

•There’s discussion of some alternative (to PVA) matrix materials, such as microfibrillated (is that a word?) cellulose and polyitaconic acid.

Are you one of the 21%? (image by Gemini)

Speaking of Tide EVO, the WSJ wrote an article on it this month with some interesting data. As I’m a bit cautious on copyright these days, I won’t reproduce it here. In summary it notes that P&G has ~60% of the U.S. laundry detergent market, with Tide at ~38% share. Despite that position, P&G initiated development of the new Evo format, a 3-inch, six-layer detergent tile shortly after the 2012 pod launch, driven by identified performance gaps: inadequate odor removal from synthetic fabrics, suboptimal cold-water efficacy, and a ceiling on pod chemistry complexity imposed by chamber-count constraints. Development took over a decade at P&G's Mason, Ohio R&D campus. The product entered Colorado test markets in March 2024 and is now in national rollout through Walmart, Target, and other major retailers. Pricing is approximately $19.99 for 42 tiles (~$0.47/load) versus $12.99 for a comparable count of pods (~$0.31/load). That’s 50% more per load for the consumer to pay! As of early national rollout, Tide evo holds a 0.6% share of the laundry category; incremental category growth in test markets was positive per Kantar, though the unmet consumer need the format uniquely addresses—relative to existing pods or detergent sheets—has not been clearly established by independent observers. Anyone have experience with the product? Write in!

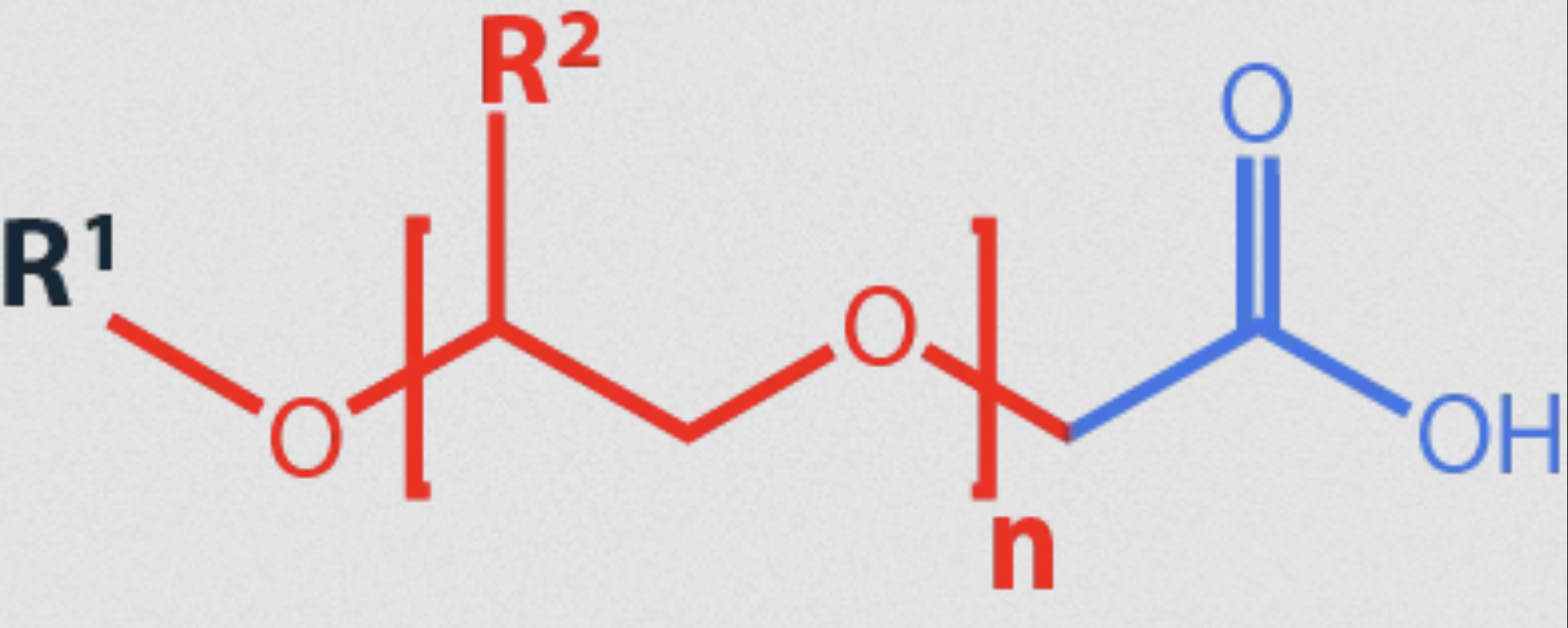

Colonial Chemical has an interesting blog and they recently wrote there about ether carboxylates. The generic structure looks like this:

What do you think?

There’s a lipophilic alkyl chain (R¹), a hydrophilic alkoxylate chain, and a terminal carboxylic acid group. The alkoxylate chain can be EO or EO and PO. The ionic state of the product is pH dependent due to the carboxylic acid group. They are thus known as crypto anionic (How cool is that !?)surfactants as they are anionic in alkaline conditions and nonionic in acid. They’re usually sold as either the free acid, an alkali metal salt or ethanolamine salt. According to Colonial (who makes these under the tradename ColaCarb) they are used in personal care but the bigger areas are in industrial lubricants, i.e. metalworking fluids, hydraulic fluids, treatment fluids, etc., oilfield operations, i.e., water-based drilling muds, enhanced crude oil recovery, etc., industrial cleaning, construction (concrete admixtures as superplasticizers), textile industry, and other industrial applications. I did not know any of this and now I, and you, do. There’s a part two to the Colonial blog post on this due out soon.

Two of my favorite companies (BTW I have lots of favorites, so don’t be offended if I don't name you this month. Your company is probably on the favorites list, potentially) Sironix and Ballestra announced a collab in Furasoft LFS an anionic surfactant. It’s based on Furan and is called lauroyl furan sulfonate (Yeah! A freely disclosed INCI name.) The product is made using Ballestra’s market leading air/SO3 reaction and the press release gives a fair bit of detail about the mild reaction conditions and high yields. Great progress for both companies.

Speaking of Furan based surfactants, Bioataraxis registered a new INCI name for one of their products, Sodium Lauryl Furoate Sulfonate. Nice. And as you probably know, because you read it here, Bioataraxis and Ballestra also collaborated on sulfonation and drying of these surfactants.

Interesting news from Church and Dwight. Apparently they’ve acquired the delightfully named “Miss Mouth’s Messy Eater” (Yep) for $325 M which is 4X sales and 11.6 X EBITDA. It’s a stain treatment product line and Miss Mouth, contrary to what you might expect, is based in NC, not NJ. Anyway the name is a sort of double entendre, because you know if you’re a messy eater you’re going to miss your mouth with food right? I love it. I love this name. Now, I did some digging and this is the formula of the spray as listed on the company website: Water (7732-18-5), Ethoxylated Alcohol C12-C15 (68131-39-5), Glycerin (56-81-5), Sodium Sulphite (7757-83-7), Ethanol (64-17-5), Citric acid (77-92-9). Yes, I know what you’re thinking – you ethoxylators out there – I could put a little of my product in water, stick it in bottle with a dopey name on it – and get 4X sales for the company. Sure. Go ahead then. Give it a shot.

In a similar vein (stick with me here), I read here (https://www.beautyindependent.com/the-inkey-list-oat-balm-cleanser/) in the Beauty Indendent about the Inkey List’s Oat Balm Cleanser. Customers complained about it for six (6!) years. A typical complaint went like this “My latest one has bits in it that don’t dissolve,” They took another two years to fix it. And the article holds the company up as an exemplar of transparency. Can you imagine if we (the chemical industry) conducted ourselves like that?! Here's the IL: Prunus Amygdalus Dulcis (Sweet Almond) Oil, PEG-20 Glyceryl Triisostearate, Avena Sativa (Oat) Kernel Oil, Cera Microcristallina, Helianthus Annuus (Sunflower) Seed Wax, Sorbitan Olivate, Polyglyceryl-10 Stearate, Polyglyceryl-6 Caprylate, Polyglyceryl-4 Caprate, Jojoba Esters, Phenoxyethanol, Aqua (Water), Hippophae Rhamnoides (Seaberry) Fruit Oil, Tocopherol, Polyglycerin-3, Acacia Decurrens (Early Green Wattle) Flower Wax, Helianthus Annuus (Sunflower) Seed Oil, Ascorbyl Palmitate. Ethoxylators. How are you feeling now?

As I perused my well-thumbed copy of Formulation and Adjuvant Technology magazine here https://www.agropages.com/magazine/detail-374.htm , I came across a nice description of Clariant’s surfactant offerings in this space and a good primer on how to approach the market (in my opinion). If your interests lie in this direction, check it out.

I read in HAPPI that Unilever will invest $270 million in a new Global Innovation Center in New Haven, CT (Well, fancy that!), with $50 million allocated to capital expenditure; total public and private investment in the project will exceed $300 million. The center, slated to open in spring 2029, will house approximately 300 employees and consolidate R&D for Unilever's personal care, beauty, and wellbeing businesses, replacing the existing Trumbull, CT facility that has operated since 1972. Capabilities will include a polycultural (A real word apparently) skin and hair center, a human performance lab for ingestibles testing (not edibles, I’m sure) , the Unilever Fragrance House (relatively new) , and a packaging innovation studio, with stated plans to incorporate AI and quantum computing for materials discovery (of course!). The investment extends Unilever's cumulative US spending to approximately $15 billion over the past decade. Very nice! Dear UL – don't forget to send my invite for the ribbon cutting.

As an advisor to Dot Ingredients and PureSurf, I’m keenly interested in chemicals from wood routes. C&E News wrote this article (https://cen.acs.org/business/biobased-chemicals/can-you-really-make-chemicals-from-wood-at-industrial-scale/104/web/2026/05) about UPM’s latest big bet on this technology. The company has commissioned a $1.6 billion lignocellulosic biorefinery at Leuna, Germany, designed to process 220,000 t/year of European beechwood at full capacity, targeted for 2027. The facility separates wood into cellulose (50%), hemicellulose (25%), and lignin (25%) via enzymatic hydrolysis, then converts the C6 sugars catalytically into ethylene glycol and propylene glycol, and upgrades lignin into functional fillers (carbon black replacement) and other derivatives. Lignin/derivatives production has started; glycols production is being brought online over 2026. According to UPM, the global lignin market projected to grow from 25.2 million t (2023) to 29.6 million t (2030). Let’s keep an eye on this one.

I still get asked a lot about the sulfate free trend and formulations. It’s a thing for sure. Even the sulfate producers are pushing their sulfate free bona fides. Coast Southwest, in their April blog talked about a couple of blends they are selling and I thought I’d put them here.

Endinol® MILD BSB-1 (fully sulfate-free): A gentle blend of Cocamidopropyl Hydroxysultaine, Sodium Cocoyl Isethionate, Sodium Methyl Cocoyl Taurate, and HoliSurf LF glycolipids. It provides optimized mildness and premium feel, ideal for facial cleansers, micellar waters, sensitive-skin body washes, and other gentle rinse-off products.

Endinol® MILD BSB-2 (SLS/SLES-free): Combines Sodium C14-16 Olefin Sulfonate, Cocamide DIPA, Cocamidopropyl Betaine, and HoliSurf HF glycolipids for versatile, high-foaming performance. Perfect for shampoos, body washes, and multi-use cleansing systems that require rich lather without compromising mildness.

In related sulfate free news, Clariant recently launched a new salt-free sodium methyl cocoyl taurate surfactant, called Hostapon CT Solid (90% active). The release cites Mintel data showing dry skin claims in new soap/bath/shower launches increased from 0.6% in 2023 to 3.9% in 2025 (OK), and states 51% of German adults report dry skin (is that true?), as market context for the launch. Stated technical attributes include foam stability, oil stability relative to other taurates, and formulation flexibility attributed to lower salt content. Sustainability claims include an 80% Renewable Carbon Index and ready biodegradability, with RSPO Mass Balance certification available.

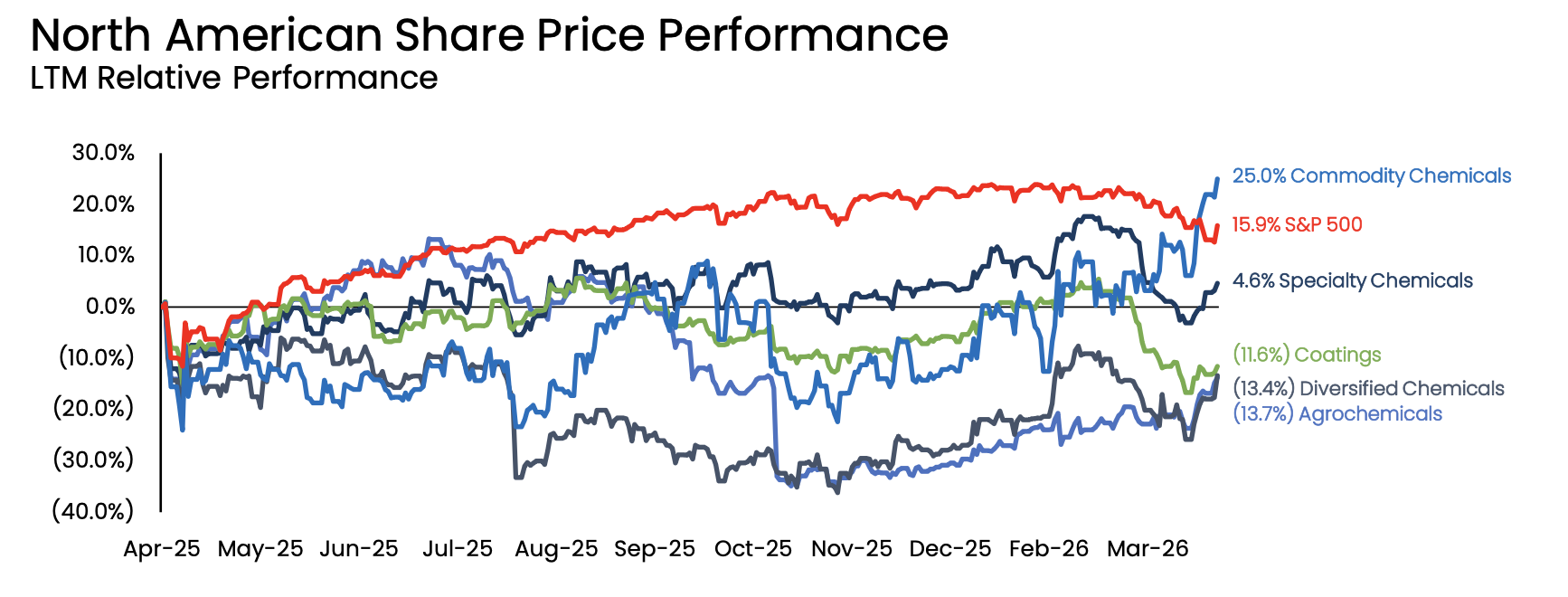

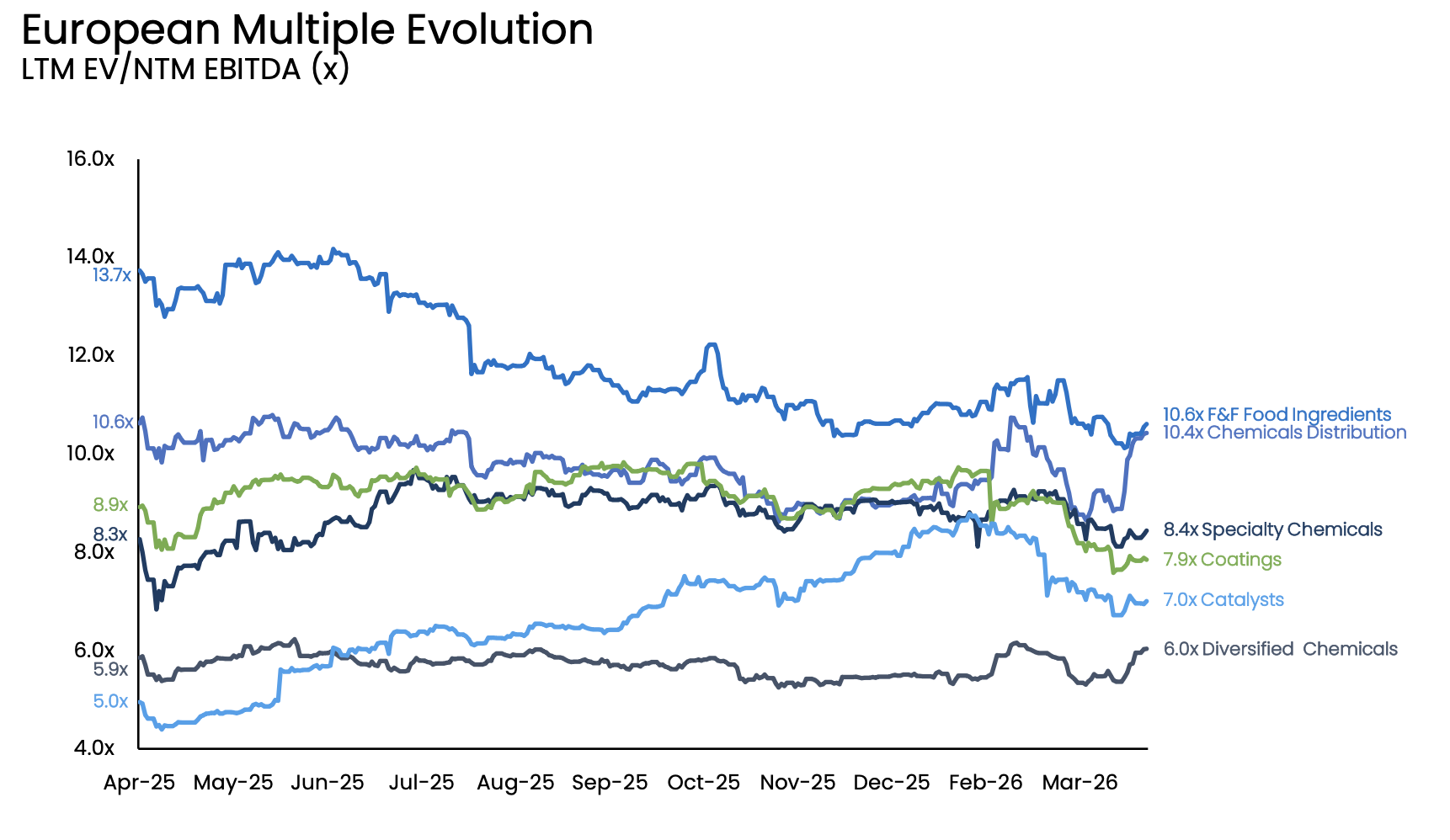

I-Bank insights: The great Balmoral Advisors, published their quarterly newsletter and you should get in touch with them to get on their list. Couple of charts in there caught my eye.

First, US commodity chemicals had a stock price field day since things kicked off with Iran due to the US’s cost advantaged position in gas and oil.

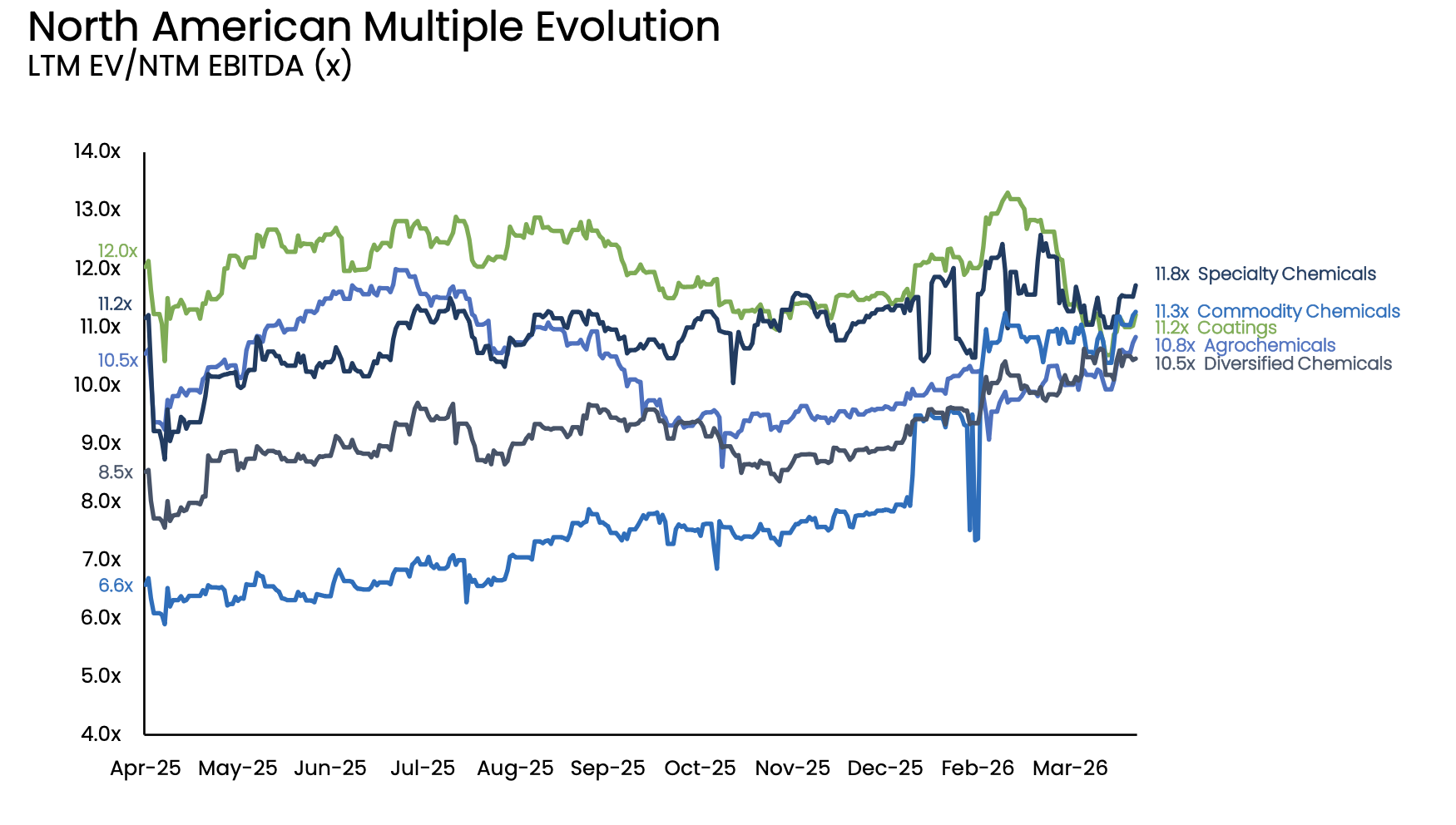

And North American transaction multiples kinda bunched up toward the high end.

In contrast to European multiples.

In case you missed it, June 16th was World Refill Day and L’Oreal was all over it. On 6/16 the company launched the third edition of its #jointherefillmovement. Refill options now span 18 brands and 28 products across all four business divisions (Luxe, Dermatological, Consumer Products, Professional). New entrants include Youth to the People, Helena Rubinstein, La Roche-Posay, Vichy, CeraVe, and Garnier (Ultra Doux). Refill manufacturing capacity is sited at Gauchy and Aulnay (fragrance), Burgos (hair care), and Vichy (skin care), supported by the L'AcceleratOR programme for next-generation packaging materials (seaweed-based packaging, sugarcane bio-plastics, recyclable paper bottles). What do you think? Implications for ingredients?

Seventh Generation has launched a line of Ultra Deep Multisurface Cleaners. The IL is on their site and I won’t reprint it here. But – they’re built on C10 APG as the core surfactant. I thought you should know that.

Vogue magazine (well-thumbed) tells me Elf, the famous skincare company has got into haircare. So what are the shampoos built on? The full (and frankly, ridiculously long) IL is below but – TLDR; it’s that now famous combination of isethionate and AOS for a sulfate free experience. Interesting. : Water (Aqua), Sodium Cocoyl Isethionate, Sodium C14-16 Olefin Sulfonate, SodiumLauroyl Methyl Isethionate, Glycerin, Cocamidopropyl Hydroxysultaine, CocamidopropylBetaine, Fragrance (Parfum), Phenoxyethanol, Sodium Chloride, Amodimethicone,Disteareth-75 IPDI, Citric Acid, Argania Spinosa Kernel Oil, Panthenol, GuarHydroxypropyltrimonium Chloride, Polyquaternium-7, Potassium Sorbate, StarchAcetate/Adipate, Trideceth-12, Trisodium Ethylenediamine Disuccinate, Arginine,Ethylhexylglycerin, Glycereth-26, Tetrasodium Glutamate Diacetate, Sodium Benzoate,Divinyldimethicone/Dimethicone Copolymer, Cocamidopropyl Dimethylamine, SodiumHydroxide, Hydrolyzed Pea Protein, Hydrolyzed Vegetable Protein, C12-13 Alketh-23,C12-13 Alketh-3, Hexyl Cinnamal, Linalool, Hexamethylindanopyran, Benzyl Salicylate,Linalyl Acetate, Hydroxycitronellal, Citronellol, Citrus Limon Peel Oil, Geraniol,Limonene, Terpineol, Dimethyl Phenethyl Acetate, Pinene, Alpha-Isomethyl Ionone,Hexadecanolactone, Cananga Odorata Oil/Extract [B-00002]

Market News:

Asia's fatty alcohol ethoxylatesMarket: Saw spot prices increased, tracking a rise in feedstock fatty alcohol mid-cuts and upstream palm kernel oil costs. While downstream surfactant demand remains weak due to global economic conditions, buyers are anticipated to initiate restocking activities in the upcoming quarter to secure inventory ahead of potential price increases. Most transactions are restricted to contract shipments, with spot purchases limited to urgent requirements. In China, domestic consumption is flat amid macroeconomic headwinds and declining crude oil prices, which are depressing petrochemical futures. Upstream, the European Union Deforestation Regulation and El Nino weather conditions are supporting demand for feedstocks, while ethylene oxide markets remain steady with muted demand.

Global fatty alcohol markets.:

In Asia: spot prices for mid-cut fatty alcohols increased due to rising feedstock palm kernel oil costs alongside expanded buyer restocking. Market demand is further supported by purchasing ahead of the European Union Deforestation Regulation implementation and anticipated upstream supply disruptions from an active El Niño climate event. Conversely, long-chain fatty alcohol prices contracted due to seasonal off-peak conditions and available alternative feedstock, while short-chain markets remained stable or weak. Regional outlook indicators include projected growth in crude palm oil demand and upcoming production capacity expansions from new facilities

In Europe: mid-cut fatty alcohol spot prices maintained a downward trajectory due to earlier feedstock cost reductions, though a recent recovery in Asian palm kernel oil values indicates prices might stabilize or reverse upward. Spot supply varies between balanced and tight depending on the vendor, with expectations of increased volume entering the market later. Significant administrative and geopolitical developments include a legislative delay regarding compliance deadlines for the European Union Deforestation Regulation, a postponed implementation of Indonesian export controls on palm oil, and the reopening of the Strait of Hormuz following the so-called peace agreement between the United States and Iran

In the USA: The United States fatty alcohols market faces downward pricing pressure during current contract negotiations, driven by declining feedstock lauric oil costs and below-average seasonal demand. Domestic supply is sufficient, while import volumes are trending lower due to compressed margins and the sustained cost advantage of petro alcohols over natural alternatives. Upstream crude oil and ethylene feedstock prices are decreasing amid improving supply availability. In geopolitical and regulatory developments, the so-called peace agreement between the United States and Iran has eased logistical disruptions through the Strait of Hormuz, raising expectations for higher crude exports and alleviating pressure on oleochemical feedstocks. Additionally, the United States Supreme Court invalidated prior reciprocal tariffs, leaving a subsequent universal tariff regime active.

The Asian linear alkyl benzene (LAB) Market: The Asian linear alkylbenzene market indicates downward pricing trajectories driven by lower upstream crude, kerosene, and benzene costs, alongside increasing regional supply. Purchasing activity remains limited, particularly in India, as the monsoon season and anticipated El Niño patterns reduce consumption expectations. Similarly, the linear alkylbenzene sulphonate sector indicates pricing contraction due to increased supplier competition. Market participants are monitoring geopolitical developments concerning Middle East peace agreements, the lifting of sanctions on Iranian crude, and the resumption of shipping through the Strait of Hormuz.

In Asia's fatty acids markets short-chain fatty acid pricing exhibits stability, whereas lauric and myristic acid valuations increased due to higher palm kernel oil feedstock costs. Pricing for palmitic, oleic, and stearic acids remained flat amid limited transaction volumes and reduced demand. Market indicators suggest valuation support for upstream crude palm oil and palm kernel oil stemming from implementation of the European Union Deforestation Regulation, supply variances associated with the El Niño climate pattern, and a revised Indonesian biodiesel mandate. Purchasing activity remains constrained, although inventory replenishment is projected to increase in the upcoming period.

The Music Section:

Guns and violence last month so peace and love and no more war this month – OK?

Todd Rungren. I have this album. Saw him at Reading early 80’s

Entre Nous by Rush. This is an absolute monster of a love song. Perhaps the best ever by anyone. God bless Neil Peart.

Reggae - What a genre for peace and anti-war songs….

This is a classic

And this

Two minutes to midnight. The hand that threatens doom.

An unusually sensitive ballad from Motorhead, 1916 (July 1st, the 110th anniversary of the start of the Battle of the Somme.

Hmm.. well I want to try and finish a little more upbeat after that. Here we go: Elvis: What’s so funny ‘bout peace love and understanding.

Hey! Happy 250th birthday America, you old git. Only kidding you’re still young!

That’s it folks!

When will I see you again? October 27th – 28th in Kuala Lumpur of course https://events.icis.com/website/14105/home/

I got a really nice email in response to this song last month, so I think I’m just going to keep it here until the conference. It is an aural and visual cornucopia, is it not? And, by the way, it’s beat together right? Not be together… Good either way though.