Surfactants Monthly - May 2026

Surfactants Monthly – May 2026 (Early Edition)

We’re off on vacation starting today so you’re getting the blog a bit earlier.

Another big month. We had our 16th World Surfactants Conference in Jersey City where the world’s surfactant value chain leaders learned, networked and did a huge amount of building ideas and strategies around the over-riding issue that is the Iran Conflict. I normally don't do conference reports but The Great Doris De Guzman posted her top speaker quotes from the event on Linkedin. And by her kind permission I am reproducing some selected quotes here, so you get a flavor of what went on.

Heard from the stage at 16th World Surfactants:

"Europe and Asia face greater recession risks than the USA because of their higher exposure to energy imports, while North Americas natural gas advantage continues to support its chemical industry competitiveness relative to regions dependent on naphtha-based feedstocks." Robert Fry, PhD, Economist:

"Fossil feedstock volatility is raising interest in feedstock diversification, including sugar, bio-naphtha, renewable ammonia, renewable hydrogen, and other domestic agricultural inputs. China is now scaling several bio-based chemicals more aggressively, brand-owner collaboration is stronger, and renewable surfactants may have better traction than biopolymers, although million-ton scale remains difficult without policy support, standardization, and investment beyond pilot scale." - Doris De Guzman (Green D Market Analytics)

"We are seeing sharp regional differences, with China moving to daily pricing, Europe focused on energy-cost exposure, and the USA more insulated. Customers now want immediate visibility into Middle East exposure and mitigation plans." - Louis Snyders (Sasol Chemicals)

"Coast Southwest is benefiting from regionalization and reshoring but must manage longer lead times, tighter customer expectations, and credit constraints as prices rise." - Jarrod Kaltenbach (Coast Southwest)

"Oilfield chemicals business is seeing strong demand from US oil and gas activity, forcing inventory planning to stretch from roughly 30 days toward 120 days while relying heavily on supplier relationships and customer forecasts." - Jimmy Jett (Integrity Biochem)

"Lauric oil prices are likely to remain elevated this year, with biodiesel mandates, EUDR uncertainty, tariffs, and trade cases continuing to complicate sourcing, pricing, and supply chain planning for surfactant producers." Lucas Hall, ICIS

“CO2 should not be viewed as waste, but as a viable carbon feedstock for the next generation of surfactants and polyurethanes. Sustainability only succeeds commercially when it is combined with strong performance, credible economics, and clear accountability that brands can communicate to consumers.” - Keith Wiggins (Econic Technologies)

“In personal care, consumers increasingly associate sustainable surfactants and emulsifiers with mildness, gentleness, and better skin compatibility rather than performance compromise. Our focus is developing cellulose-based emulsifier systems that can outperform traditional chemistries at significantly lower use levels while maintaining stable long-term feedstock economics.” - Michael Fielding (DOT Ingredients)

“Sustainable surfactants will only succeed if they meet the three non-negotiables of the chemical industry: they must be sustainable, perform as well or better than incumbent chemistries, and ultimately be cheaper — not just cost competitive. By using captured CO2 as a drop-in feedstock within existing surfactant infrastructure, we can lower carbon footprint, reduce dioxane formation, improve production economics, and create entirely new surfactant platforms without requiring disruptive manufacturing changes.”: Nick Smith, Viridi

“Sh*t’s about to get real” – An honest and plain-spoken discussion leader (the best kind) in one of our roundtables.

You can read the full set from Doris at these links (https://www.linkedin.com/pulse/key-quotes-from-16th-icis-world-surfactants-conference-day-hlooe and https://www.linkedin.com/pulse/key-quotes-from-16th-icis-world-surfactants-conference-day-kn9pe )

By the way how has she earned the soubriquet “The Great” as in The Great Doris De Guzman? Not many people get this appellation (from me). Well it’s because she has been for over two decades now the most credible and comprehensive voice in the field of renewables. Her work, newsletters, reports, talks etc. is of the very highest quality. I have therefore been really privileged to collaborate with Doris on her most recent project on the renewable surfactants market.

On Day 2 of our conference, Doris presented several findings from that project, her company's new multi-client report, "Detailed Assessment of the Renewable Surfactants Market." This new 243-page report, offers the most comprehensive examination of the rapidly evolving renewable surfactants sector including 80 companies profiled along with their technology portfolios, TRLs, commercialization status, products in the market, milestones and select partnerships/investors. For more information on this report, contact admin@greendma.com . You won’t regret it. [Yes, that was a commercial.]

The other thing this month was SCC Suppliers Day at the Javits Center. I don’t have a top 5 or anything like that but it was good to see some friends there including a newly re-branded Galaxy Surfactants and Science Communicator par excellence Jen Novakovich holding court (it was kinda like that – and I mean that in a complimentary fashion) and livestreaming at the Independent Beauty Association booth. I was asked a few times during my few hours at the event about the Fatty Acid Anti-Dumping Petition which we wrote about earlier this year. I found I didn't have anything clever to say so I went home and brought myself up to speed and this is what I (assisted in the research by Claude Opus 4.7) can now say about it.:

Vantage Fatty Acid Anti-Dumping Petitions – Summary and Update

•Petitioner: Vantage Specialty Chemicals, Inc. (Deerfield, IL). No domestic co-petitioners.

•Filed: January 28, 2026, at both DOC (Dept of Commerce) and USITC (US International Trade Commission).

Subject merchandise:

•"Certain fatty acids" with chain lengths C6–C18, iodine value below 105 g/100 g, and degree of split of at least 97%.

•Covers stearic acid, oleic acid (pure-cut/distilled), and mixed/blended forms including coconut, palm kernel, palm, palm stearin, palm fatty acid distillate, and palm olein fatty acids.

•Excludes products with ≥90% C6/C8/C10 content and mixtures where the fatty acid is below 80% of total weight.

Subject countries:

•Indonesia and Malaysia.

•CVD (Countervailing Duty) petitions include transnational subsidy allegations against China.

Alleged and recalculated margins:

•AD (Anti-Dumping) margins alleged in the petition: Indonesia 20.08%–72.03%; Malaysia 64.67%–94.41%.

•AD margins as recalculated by DOC at initiation: Indonesia 18.38%–69.56%; Malaysia 59.56%–170.49%. The Malaysia upper bound exceeds the petition figure! [Whoa! That’s gotta be a signal right?].

•CVD: DOC initiated investigation of 16 Indonesia programs and 18 Malaysia programs. Government of China filed written comments on February 11, 2026.

Procedural status (through May 20, 2026):

•DOC initiated AD and CVD investigations on March 9, 2026

•USITC issued 3-0 affirmative preliminary injury determinations on April 1, 2026

•DOC postponed CVD preliminary determinations on April 29, 2026 from May 13 to the 130-day statutory maximum (~July 17, 2026), citing pending respondent questionnaire responses.

•AD preliminary determinations currently expected on or about July 27, 2026, subject to customary 50-day postponement.

Respondents:

•Petition identified 23 Indonesian and 16 Malaysian producers/exporters in Exhibits I-12 and I-13.

•DOC mandatory respondent selection was completed by mid-April 2026, but names were not publicly available as of May 20, 2026.

Industry-association response:

•Crickets. No public position taken by the American Cleaning Institute, Personal Care Products Council, or others (that I can see) as of May 20, 2026.

Key inflection points ahead

•~July 17, 2026: CVD preliminary determinations and first cash-deposit rates.

•~July 27, 2026 (subject to extension to mid-September): AD preliminary determinations.

•Q1–Q2 2027: Final DOC determinations and ITC final injury vote.

Hmm.. so what? (This is me talking, not Claude) Well if you are making your own Fatty acid here in the US you may be OK – or more than OK. If not, well, possibly not so much. It depends on the success of the petition. So what do I think it is going to happen with the petition? Well, I don’t know and I won’t be betting on Polymarkets either. However, these are the broad scenarios. If Dept of Commerce preliminary anti-dumping rates come in below 15%, downstream cost pass-through will be modest and supply continuity manageable. If the rates come in above 50% for either country, expect significant U.S. price increases and reshoring/substitution to domestic fatty acid producers like, P&G Chemicals, Emery, Twin Rivers etc, plus diversion attempts via Vietnam, Thailand, the Philippines and all sorts of other places, e.g. India ( I expect that the anti-circumvention provisions embedded in the petition will be tested early and often). If the US International Trade Commission final vote on the matter is negative (no material injury), all duties and cash deposits are refunded; this is highly unlikely given the earlier unanimous 3-0 preliminary affirmative determination. So, look, you can kinda get a sense of where this is headed unless there is significant organized opposition.

As we all know, fatty acids are a key component in many common household cleaning products and soaps and personal care products plus a huge variety of industrial products. If price increases of the type noted in the middling scenario above are implemented my expectation is one of clear demand destruction in the consumer market given the already severe stress the American consumer is facing. It will be interesting to see if and when US purchasers of fatty acids and trade associations, not just ACI and PCPC, but SOCMA for example, comment on this matter. Interesting times. Let’s check in at the end of July for the preliminary determinations by Commerce.

In the meantime, perhaps one of my connected and engaged readers would like to comment from the field (anonymously or otherwise) The vaunted 24 hour tip-line is open.

Drop a dime before you hop on your next flight - Image by Grok

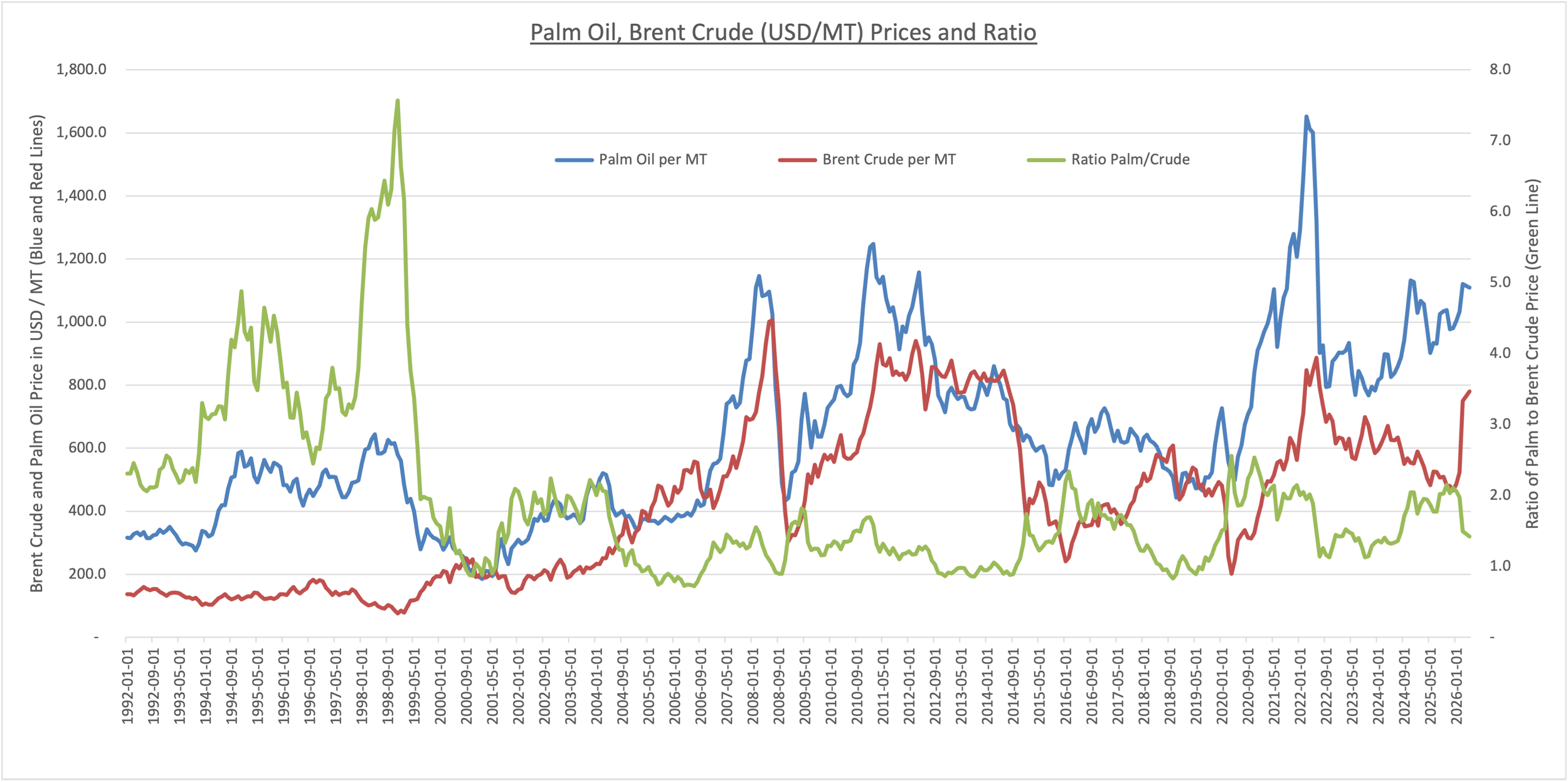

And the other thing I was asked about was MES (Methyl Ester Sulfonate). The deal is this. Now that the Strait of Hormuz is bunged up worse than your dog after getting into all that cheese, maybe palm-based MES’s time has come as a supplement to LAS in HI&I and a primary surfactant in PC. Maybe? What do I think? I think I don't know yet but I am leaning negative. The original idea back when there was a bit of a run on MES plants in Asia (and a really big one in the USA) was that the ratio of Palm price to crude was the thing to watch. I never understood though, what was the magic number for this ratio. Is it 1? Can someone opine? Anyway, here’s the last 25 years of the ratio.

Conclude anything from this?

It was also good that existing sulfonation assets could make MES. In fact back when Huish (remember them?) built that big sulfonation plant in Pasadena, TX, it could run LAS and MES (and various other odds and ends of interest). These days, it seems that Palm oil is ever more tightly tied to the crude oil market via biodiesel (and renewable diesel I suppose) with Indonesia pushing B50 and all. So I just don't know about MES right now. However, a lot of folks, a lot smarter than me have done a lot of technical work (that's a lot of lots!) on synthesis and formulation. One of them has already used the tipline. Perhaps you will too?

If you don't have a 50’s diner nearby, an email will do - Image by Grok

Recession Watch:

Maybe I have been a bit too pessimistic. Maybe not. But at my conference the other week, Robert Fry a top-flight original thinker and economist, argued that Middle East-driven oil price rises won't tip the US into recession unless Brent stays above $130/bbl for roughly two months. Brent had only briefly exceeded that level and was down about 7% to near $102/bbl (at that time) on optimism over a potential US–Iran deal. He also noted spot prices have been running $10–13/bbl above futures. Fry also said US gasoline near $4.50/gal is weighing on consumer sentiment (University of Michigan index at record lows), but the US is structurally less vulnerable than in past oil shocks: it uses one-third less energy per dollar of GDP than in 2000, two-thirds less than in the 1970s, and is now a net petroleum exporter. Europe and Asia are more exposed (this synchs with my ‘Merica! Theme in opening remarks).

He cited tailwinds supporting US resilience: AI-driven productivity gains and data-center buildout, and fiscal stimulus from the One Big Beautiful Bill Act (OBBBA), particularly immediate expensing of capex, though OBBBA worsens long-run deficits and debt. Nondefense capital goods orders ex-aircraft are up ~10% year-over-year. Consumer spending (PCE) was strong in February and March 2026, auto sales held up, but housing remains depressed. Unemployment claims are at their lowest since 1969 (Go figure?!).

On monetary policy, headline PCE inflation is at 3.5% (core 3.2% - and that, to me is bad), which Fry expects will keep the Fed on hold for some time. He argued rate cuts are far less stimulative than commonly believed — and possibly contractionary — though they matter for small businesses and housing. Long-term, he sees US GDP growth around 2%, with AI offering upside to a 1.8% baseline. [What do you think. I understand, logically, the confidence. I’m just not feeling it. How about you?]

War Watch:

Part 1: Chemicals and Surfactants:

BTW - ICIS has been doing an incredible job monitoring on a daily basis what’s happening the chemical markets. I really do encourage you to subscribe to their service. And yes, I know I’m biased because I have that conference with them but still..

As we’ve discussed, the war began on 28 February 2026. The Strait of Hormuz, which carries roughly a quarter of global seaborne oil and the bulk of Middle East petrochemical exports, has been effectively closed since then.

Pricing moved in two phases. March–April registered the fastest rise in global chemical prices in two decades. European spot benzene reached its highest level since July 2022. LAB prices in Asia exceeded $4,000/MT CFR, against a prior level near $1,500/MT. By May, prices reversed course across most chains as downstream buyers stopped absorbing costs and Chinese exports filled gaps. Smaller detergent makers exited the market at peak prices, contributing to demand contraction. Feedstock kerosene (n-paraffin source) and benzene declined from recent highs and traded in a narrower May range. South Asia spot supply remains tight as Middle Eastern shipments are not yet normalized, but reduced demand has freed up some spot lots. Related ICIS coverage from 14 May indicates LAB sulphonate (LAS/LABSA) prices in Asia declined on dull demand and competitive pricing, consistent with the LAB pullback.

Feedstock and energy costs remain very high. Brent traded volatile around peace-talk headlines; the ICIS TTF gas benchmark crossed back above €50/MWh ($17/MMBtu) in the week of 18 May. Asian refiners declared force majeure on Middle East crude contracts. Qatar LNG output stopped on 2 March with damage reported at Ras Laffan on 18 March. Asahi Kasei reported naphtha cover only through July. Asia naphtha supply has risen modestly without triggering buying, given soft petrochemical demand. M&A activity seems to be reorienting toward supply security. ICIS analyst commentary notes that duration, not severity, will determine whether triple-digit oil and chemical plant shut-ins materialize.

Sulfur (feedstock for SO3 / sulfonation). China sulphur imports in April fell 72.4% year-on-year to 295,510 MT, against over 1 million MT in April 2025. Cumulative January–April imports were down nearly 50% year-on-year at roughly 1.8 million MT. China imports about 10 million MT annually, with roughly half sourced from the Middle East in normal conditions. UAE volumes fell 90.8%, Oman 94.2%, Saudi Arabia 55.3%, and Iran 47.2% (one or two vessels dispatched pre-war). Russia contributed zero on a sulfur export ban running through 30 June. South Korea, Japan, Canada and Taiwan partially backfilled but at lower absolute volumes. The implication for SO3 / sulfonation economics is reduced feedstock availability into China at higher cost.

So – the net of all this is : Surfactant feedstock chains saw a sharp March–April upward move (LAB roughly 2.5x baseline, benzene multi-year highs, China sulfur imports cut roughly in half), then a May pullback driven by demand destruction rather than supply normalization. Hormuz transits remain at limited to zero.

Part 2 – Energy and the Economy:

For this part, I’m relying on the International Energy Agency’s Oil Market Report for May 2026 and their Middle East Topic page. I also reference Goldman Sachs 7th May Interview with their head of Global Oil and Products Trading, Jerome Dortmans [I like this perspective because he has skin the game- metaphorically. It’s dollars not actual skin.].

The economic shock reaches the global economy through two channels: higher prices and the physical closure of the Strait of Hormuz for various goods.

Prices rose sharply but have since come off their peak. Brent futures finished April more than 55% above pre-conflict levels. Cash crude rose more. North Sea Dated averaged $120.36/bbl in April, having traded a roughly $50/bbl range within the month; it touched $144/bbl, fell below $100/bbl, and was near $110/bbl in mid-May.

Demand has started to give way, but unevenly. Dortmans puts market-wide demand destruction at 3–5 mb/d so far, concentrated in emerging markets and Asia, with no meaningful loss yet in the United States or Europe at current prices. The IEA's measured figure is a 420 kb/d contraction in world oil demand for 2026 as a whole (to 104 mb/d), which is 1.3 mb/d below the pre-war forecast, with the sharpest hit in 2Q26 at about 2.4 mb/d year-on-year. The petrochemical and aviation sectors are absorbing the steepest losses first.

Policy responses have been coordinated. IEA member countries released 400 million barrels of emergency stocks from 11 March, the largest such action in the Agency's history. The IEA, IMF and World Bank set up a joint group on the economic and energy impacts, meeting first on 13 April. There is a secondary inflation and food-security channel: more than 30% of global urea trade and around 20% of ammonia and phosphate (i.e. fertilizer inputs) trade pass through the Strait.

Effect on global energy markets:

Supply: Global oil supply fell to 95.1 mb/d in April, down 1.8 mb/d on the month and 12.8 mb/d since February. Gulf output was 14.4 mb/d below pre-war levels, with more than 14 mb/d shut in and cumulative Gulf losses above 1 billion barrels. Offsets are material but partial. The IEA raised its 2026 Americas supply growth estimate by more than 600 kb/d, to 1.5 mb/d on average. Atlantic Basin crude exports rose 3.5 mb/d since February (notably the US, Brazil, Canada, Kazakhstan and Venezuela), redirected toward East-of-Suez markets. Russian exports also rose, helped by a temporary US sanctions waiver on oil already on water. Saudi Arabia and the UAE are rerouting some volumes through the only Strait-bypass pipelines, with 3.5–5.5 mb/d of available capacity. OPEC+ effective spare capacity is now minimal, given how much is already shut in.

Inventories: Observed global stocks drew 250 mb across March and April, about 4 mb/d: down 129 mb in March and 117 mb in April. On-land stocks fell 170 mb (5.7 mb/d) in April while oil on water rose 53 mb. OECD on-land stocks fell 146 mb. This is the buffer that has kept prices off their highs, and it is depleting every day.

Refining and products: Refinery crude throughput is forecast to fall 4.5 mb/d in 2Q26 to 78.7 mb/d, and 1.6 mb/d for 2026 to 82.3 mb/d. Nearly 3 mb/d of Gulf refining capacity is offline. Crude imports were cut hard in Asia: China down 3.6 mb/d (February–April), Japan 1.9 mb/d, Korea 1.0 mb/d, India 0.76 mb/d. Refining margins are at historically high levels, with record middle-distillate cracks. Jet fuel prices nearly tripled.

Gas and LNG. Global LNG supply is down about 20%. Qatari and UAE LNG fell by over 300 million cubic metres per day since 1 March, more than 2 bcm per week. Qatar's Ras Laffan, the largest liquefaction facility, has been offline since 2 March. Dutch TTF rose more than 45% between late February and early May. Asian gas prices rose to pull cargoes, prompting rationing in some countries. Over 110 bcm of LNG transited the Strait in 2025 (about 93% of Qatar's and 96% of the UAE's exports), with no alternative routes.

The points most directly relevant to chemical operations:

•Petrochemical feedstock. The IEA reports the steepest demand losses in the petrochemical sector, driven by constrained feedstock availability. Dortmans confirms petrochemical run curtailments in Asia tied to high feedstock prices.

•Naphtha and diesel bottlenecks. Refiners shifting yields to maximize jet fuel create downstream tightness in naphtha and diesel. Dortmans expects light ends (naphtha, gasoline) and diesel to be the products competed for through summer, even as crude normalizes.

•LPG. Gulf producers exported 1.5 mb/d of LPG in 2025; this flow is exposed to the same chokepoint.

•Sulphur. About half of global seaborne sulphur trade moves through the Strait. Sulphuric acid feeds fertilizer, chemicals, petroleum refining, and processing of copper, nickel and zinc.

•Fertilizer inputs. Urea (>30% of global trade), ammonia and phosphate (~20% each) all transit the Strait.

•Aluminium. The Gulf supplies about 8% of global aluminium, roughly 5 million tonnes shipped annually through the Strait.

Outlook for the rest of 2026 and 2027:

The single most important variable, on both the IEA's and GS’s read, is when / whether Strait flows resume and how quickly and evenly.

Rest of 2026 — oil. The IEA base case assumes flows resume gradually from the third quarter. On that basis, 2026 supply averages 102.2 mb/d (down 3.9 mb/d for the year) and demand averages 104 mb/d (down 420 kb/d). The market stays in deficit until the fourth quarter, because supply recovers more slowly than demand. The IEA expects continued price volatility into the summer demand peak.

Dortmans frames the near term as binary around the diplomatic track. If talks fail and the conflict re-escalates, cash markets re-tighten and refined products run hotter in the West into summer. Even in the favorable case, he does not expect the Strait to reopen as a flood. He estimates roughly three months before the market prices more bearish scenarios, and six to nine months for normalization. Through that period he expects refined products to trade at elevated levels while crude eases, a shift from a directional to a relative-value market, with continued competition for crude, light ends and diesel. Producer hedging has picked up in anticipation of barrels returning; consumer hedging would likely resume near $85/bbl.

2026–2027 — gas. The most durable effect in both sources is structural and is in gas. Damage to Qatari liquefaction delays the anticipated global LNG supply wave by at least two years. The IEA estimates a cumulative loss of around 120 bcm of LNG supply between 2026 and 2030, with effects felt through 2026 and 2027. New liquefaction elsewhere is expected to offset this over time, but not on a timely schedule.

So for chemicals: the most direct exposure is on feedstock (naphtha, LPG, gas) and key inorganic inputs (sulfur, ammonia, phosphate, urea). Product and feedstock tightness is likely to outlast crude-price normalization, because yield shifts and constrained Gulf refining keep light-end and distillate balances tight. And the gas channel is the one effect both sources expect to persist into 2027 even if oil markets settle.

Phew!! If you have war-stories to share, you know how to get in touch.

Reports from the front lines welcome. - Image by Grok

El Nino Watch:

As of the 14 May 2026 NOAA Climate Prediction Center ENSO Diagnostic Discussion, the alert status is El Niño Watch, with ENSO-neutral conditions still present, an 82% probability of El Niño onset during May–July 2026 and a 96% probability for December 2026–February 2027; the weekly Niño-3.4 index reached +0.9°C centered on 13 May 2026, while the seasonal February–April 2026 anomaly was +0.1°C. NOAA assigns no strength category above a 37% probability and estimates a one-in-four chance of a very strong event (Niño-3.4 ≥ +2.0°C). Fastmarkets projects Malaysian 2026 Crude Palm Oil production at 19.60 million MT, a 400,000-MT reduction from 2025. GAPKI Chairman Eddy Martono has stated that Indonesian production will stagnate in 2026 as the B50 biodiesel mandate (effective July 2026) reduces exportable volumes. The Bursa Malaysia FCPO benchmark third-month contract ranged between RM4,484 and RM4,650/MT during 18–22 May 2026, having risen from RM4,019/MT in January to RM4,568/MT in April; Kenanga Investment Bank's 2026 average assumption is RM4,250/MT and Hong Leong Investment Bank's is RM4,350/MT, with Kenanga estimating that a very strong El Niño would reduce regional palm output by 2–9% in the following year and add 5–10% to CPO prices. The characteristic 6-, 18- and 20-month lag intervals between water stress and FFB-yield decline imply that physical production impacts from the 2026 event, if it materialises at moderate-or-greater strength, would mostly be felt in 2027 and into 2028; the 2015 strong El Niño reduced Malaysian FFB yield by only 0.8% nationally and by 6.3% in Sabah, indicating the order of magnitude of plausible impact at moderate intensity.

Palm kernel oil supply tracks fresh-fruit-bunch processing with the same lag structure but operates in a thinner global market that amplifies price moves: the World Bank Pink Sheet records CPKO CIF Rotterdam at USD 2,332/MT for the Q1 2026 average, rising from USD 2,125/MT in January to USD 2,574/MT in March 2026, against a 2025 annual average of USD 2,093/MT and a 2024 average of USD 1,412/MT; the implied lauric premium over CPO Malaysia reached approximately USD 1,471/MT in March, with CPKO trading at roughly 2.3× CPO and at an unusual USD 214/MT premium over CIF coconut oil. Bursa Malaysia palm-kernel-oil futures were at the upper end of their 52-week range (MYR 5,852–8,336) at MYR 8,336/MT in early May 2026. MPOB April 2026 CPKO stocks fell 7.93% month-on-month to 192,654 MT despite the production rise. Because PKO and coconut oil together constitute the lauric pool that supplies C12–C14 fatty alcohols and lauric fatty acids, an El Niño-driven contraction in 2027 PKO output would hit an already-tight market: A 5–10% lift in CPO and a sharper lauric move would compress margins for oleo-route C12–C14 fatty alcohols and lauric fatty acids

The main near-term risk for surfactant and oleochemical manufacturers is therefore not the 2026 crop year but a 2027 lauric-tightness episode triggered by Q3–Q4 2026 drought stress, layered onto pre-existing supply constraints from Indonesia's land-seizure programme (3.3 million hectares total, of which 1.5 million hectares of oil-palm planted area have been transferred to state-owned PT Agrinas with a further 1.8 million hectares under verification, placing 2–5 million MT of CPO at risk), the December 2026 EUDR effective date, and the B50 biodiesel uplift effective July 2026, which Indonesian agriculture-ministry official Baginda Siagan estimates will reduce 2026 palm-oil exports by 11–12% relative to 2024–2025.

Think and plan ahead! BTW - If you make or buy petrochemical alcohols, 2027 may not be a bad year, interestingly.

The Other News:

Given all the ructions in the LAB/LAS market, I’m sure this is not the only company doing this, but I noticed PCC has a page on their site touting alternatives to LAS https://www.products.pcc.eu/en/labsa-alternatives/ Interesting? What are they – AES and AE of course.

Ravi Raghavan has written about the LAB situation in India (they import a lot) here https://www.linkedin.com/posts/ravi-raghavan-b7942512_lab-ugcPost-7457617277736194048-wqHh? Worth a read.

In related news, Sasol is restarting their August Italy LAB plant as noted in LI by Louis Snyders here https://www.linkedin.com/posts/louis-snyders-3a28333_sasol-ha-deciso-di-riavviare-lunit%C3%A0-di-paraffine-activity-7460515314271797249-rOLa?

Last month I gently ribbed Eastman about not immediately publishing the INCI name for their new additive for sulfate free formulations. They have utilized the tipline and also accosted me in person about it. And so Kalidex's INCI name is Ethylhexyl 3-Hydroxybutyrate and you can find more information about the ingredient here: https://www.eastman.com/en/products/industries/personal-care/applications/hair-care/kalidex . So get over there and consider sampling and so forth!

[calm down. I’m not putting yet another tipline image in here]

Personnel News, Pilot Chemical named ex CEO Mike Clark to their board of directors. Nice. Good luck and continued success to Mike and the Company. Hey by they wa, it’s not directly surfactants related but I had the chance to feel the new D5 silicone replacement from Pilot at SCC-NY and it is excellent. Goes on really nice and dries perfectly (those are not the technical terms). If you wear (or formulate) makeup you’ll appreciate what I’m saying. Get in touch and check it out.

Biocatalysis is an emerging tech. Norfalk of Denmark applies it to carbohydrate based surfactants. (I’m an advisor to their board. ). Check out this article by their CEO https://chemanager-online.com/en/topics/biocatalytic-surfactants

I agonized over whether to print this. But is any more proof needed that we are living in a simulation? There’s an ingredient called PDRN. (That’s polydeoxyribonucleotide) It’s a biological compound made of DNA fragments, primarily extracted from salmon… er… sperm and it’s behind a thing known as the salmon sperm facial, popularized by, among others, Kim Kardashian. Serious people are writing long articles about it with a perfectly straight face. Will this merit a sentence in the book on the decline and fall of Western Civilization. Am I getting too old, cynical. Is it me.. or?

[nope – no image for this one]

Ruby Bio: We’ve written about them before here. In my well thumbed copy of Ag Funder news – I noticed the following https://agfundernews.com/ruby-bio-to-launch-world-first-fermentation-derived-clean-label-emulsifiers-in-2027 The comapny plans to launch emulsifiers and polyols. Interesting. Worth another close look, I think.

More Personnel News: This time from P&G. Friend of the blog Erik Roberts has been promoted to Chief Purchasing Officer at P&G. Wow! That’s a big deal. Congrats Erik! https://www.pgchemicals.com/news/executive-perspective/may-2026-meet-pgs-new-chief-purchasing-officer-a-conversation-with-erik-roberts

Apparently Tata Chemicals has been working on a new biobased surfactant, which I read about here: https://www.tatachemicals.com/capabilities/innovation/innovation-centre and here https://www.indianchemicalnews.com/interviews/working-on-new-sustainable-chemistries-and-bio-based-surfactants-rajesh-kamat-head-sales-and-marketing-tata-chemicals-355 and here https://www.tata.com/newsroom/business/chemistry-sustainability-tata-chemicals-aalingana All a bit light on details. Can anyone point me to further information on actual structures, CAS #, even INCI names? Use the tipline if you like.

Couldn’t resist it. Sorry. - Image by Grok

Big news from blog friends, BioAtaraxis. They have successfully scaled up the EcoSAF technology to a 3-ton production scale. The scale-up campaign also enabled the collection of primary industrial data for Life Cycle Assessment (LCA) studies, alongside further improvements in product colour and active content performance. The company claims that EcoSAF represents the first industrial-scale surfactant derived from biomass residues implementing furan chemistry as a novel surfactant design platform. Large-scale samples are now available for evaluation in home care and personal care applications, with supply formats ranging from laboratory quantities up to 200 kg SKU pack sizes.

The aforementioned Jen Novakovich has published an article called Surfactant Myths and Misconceptions. It’s great. Read it here https://cmstudioplus.com/blog/surfactant-myths-things-you-should-know-as-a-formulator/ Big line: “Sodium Lauryl Sulfate (SLS) is actually fine!” You are so right, Jen.

Market News:

Asia's fatty alcohol ethoxylates Market: During the period from late April to late May, the Asian fatty alcohol ethoxylates (FAE) market experienced a continuous downward trajectory. This trend was driven by consecutive weekly declines in feedstock fatty alcohol mid-cuts and ethylene oxide costs, alongside bearish market sentiment. Buyer demand remained subdued, characterized by a wait-and-see stance as purchasers anticipated further price reductions and sought to offset higher costs incurred during earlier supply chain disruptions in the Strait of Hormuz. A wide buy-sell gap hampered spot trades, which were restricted to minimal volumes on a need-to-basis. Production was impacted by an ongoing maintenance shutdown at a regional FAE plant scheduled through the end of May. Chinese domestic markets also saw price declines amid limited trading following the Labour Day holidays. As a general reference, FAE moles 7 and 9 Drummed CIF Asia SE Spot started the period in late April at $2,400 per MT and toward the end of May pricing was at $2,250 per MT.

Global fatty alcohol markets.:

In Asia: Over the last month, the Asian fatty alcohols market exhibited a downward pricing trajectory for mid-cut and long-chain grades. This decrease correlated with declining feedstock palm kernel oil costs and general market caution tied to geopolitical conflicts. Buyers utilized delayed procurement strategies, fulfilling only immediate operational requirements while anticipating additional price reductions. In contrast, short-chain alcohol prices increased due to steady downstream demand and restricted availability of synthetic alternatives. Regional supply dynamics were influenced by a scheduled production facility maintenance shutdown and regulatory uncertainty regarding proposed commodity export controls in Indonesia. The period started with mid-cut spot pricing at 3,100 dollars per MT and toward the end of the period pricing was at 2,750 dollars per MT.

In Europe: During the last month, the European mid-cut fatty alcohols market transitioned from elevated price stability to a downward trajectory. Initially, spot prices held at elevated levels due to regional supply constraints and steady second-quarter demand. As the period progressed, spot prices decreased, tracking sustained declines in feedstock palm kernel oil costs. Supply availability showed localized improvement as a regional supplier re-entered the merchant market to clear inventory accumulated from ethylene oxide production constraints. Additionally, market participants monitored regulatory developments in Indonesia, where proposed export controls on commodities, including palm oil, introduced uncertainty and prompted isolated offer withdrawals. The period started with Fatty Alcohols C12-14 Alcohol FD NWE Spot pricing at 3,150 euros per MT and toward the end of the period pricing was at 3,060 euros per MT.

In the USA: Over the last month, the United States fatty alcohols market experienced cost increases driven by supply chain disruptions in the Middle East. The closure of the Strait of Hormuz elevated raw material and freight costs across the petrochemical value chain. Declining feedstock palm kernel oil values in Asia did not transfer to the domestic market. Synthetic alcohol producers operated at capacity, maintaining a production cost advantage over natural feedstocks. Natural alcohol import volumes slowed, with pending shipments delayed until mid-summer. Sellers allocated available inventory to contract customers, restricting spot market transactions. In regulatory developments, Indonesia announced plans to centralize commodity exports through a state-owned agency. The period started with Fatty Alcohols C12-15 Alcohol Truck and Rail DEL USG Contract pricing at 147.5 cents per pound (USD 3,245 per MT) and toward the end of the period pricing was stable at 147.5 cents per pound.

The Asian linear alkyl benzene (LAB) Market: Over the last month or so, the Asian linear alkyl benzene market transitioned from an uptrend to a downtrend. Initially, reduced output from global plant outages and rising upstream crude costs drove seller offers higher, causing the downstream sulphonate market to follow. As the period advanced, buyer resistance increased, widening the bid-offer gap and pushing purchasers to the sidelines. Reduced buying interest, combined with stabilization in the upstream benzene and kerosene sectors, balanced the constrained supply and reversed the price trajectory. The period started with linear alkyl benzene CFR Asia SE spot pricing at $4,100 per MT and toward the end of the period pricing was at $3,700 per MT. Still darned high!

In Asia's fatty acids markets - demand is set to weaken further amid market uncertainties and bearish sentiment. Volatile fossil fuel prices and swings in upstream crude palm oil, palm kernel oil, and palm stearin values have made buyers cautious, leading them to hold back on large forward spot purchases. Geopolitical tensions, the shipping impasse in the Strait of Hormuz, and the prolonged Middle East conflict are compounding the wariness, while rising CPO production and stocks in Malaysia along with falling PKO prices in Indonesia have added downward pressure on C12 lauric and C14 myristic acid prices—both, as you know, key inputs for soaps, detergents, and personal care products.

The Music Section:

Guns and violence is our theme for obvious reasons.

Police and Thieves – Junior Murvin

This one can get really dubby, e.g.

Sticking with reggae, Johnny was a good man

I know you want me to play the Stiff Little Fingers version but here’s this from SLF instead. Fits with the theme. It’s a sus sus sus sus sus sus sus-suspect device.

We don't put enough ACDC on this blog. Big Gun.

Then YT just put this in my feed because I was listening to the stuff above and, forgive me, I like it! – And as usual – you gotta love the comments. Check this one out.: Drummer: “Mom, I gotta go, we’re shooting a video today!” Mom: “Not in that outfit you’re not! Put this shirt on!”

You know, Youtube sometimes has an uncanny knack for picking ‘em. Here’s the wonderfully named Uncle Acid and the Deadbeats with Bloodlust.

OK let’s elevate the tone a little bit. Barbarian.

And… then bring it down again. Motorhead – The Hammer. What a curious crowd there though right? [caution: not nice lyrics if you could actually understand what Lemmy is saying]

That’s it folks!

When will I see you again? October 27th – 28th in Kuala Lumpur of course https://events.icis.com/website/14105/home/

Oh man, hey is that not an outrageously great song!? I wonder is it “when will our hearts be together” or “when will our hearts beat together”. I like to think beat. What do you think?