Surfactants Monthly - March 2026

It’s Earnings Season (still). We’ll cover Unilever, P&G and BASF this month – and maybe Henkel if we have time. I wrote about Croda’s 2025 results here last month. If you didn't get a chance to read it. Here’s a short video we made on the same:

Don’t forget: The 16th World Surfactants Conference, May 6 – 7th (Training on the 5th). https://events.icis.com/website/8544/

End of self-promos.

The News:

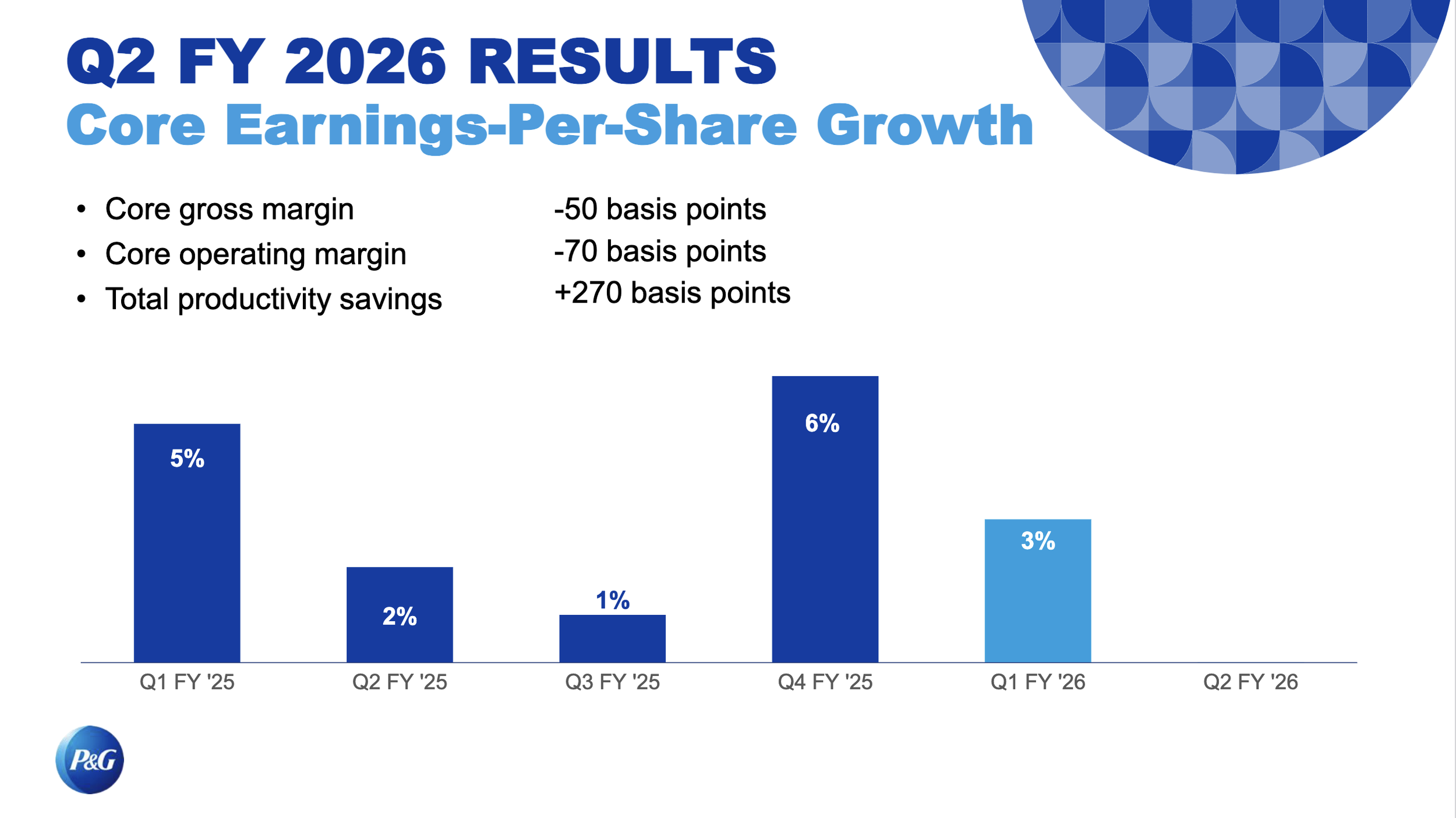

First up – P&G 2025 Earnings. Now P&G has a mid-year financial year and so at the end of 2025, they were reporting their Q2 2026 (got that?) Anyway, one of the world’s biggest consumers and makers of surfactants eeked out a 1% sales gain for the quarter. Netting out acquisitions, divestitures and currency exchange effects, sales were exactly flat. A product of volume down 1% and pricing up 1%. Only one segement grew volume and that was Beauty (comprising skin care, personal care and hair care) Earnings were down 5%, driven by decreasing gross margins and operating margins. Here’s the box score.

Here’s the earnings trend as presented on the earnings call.

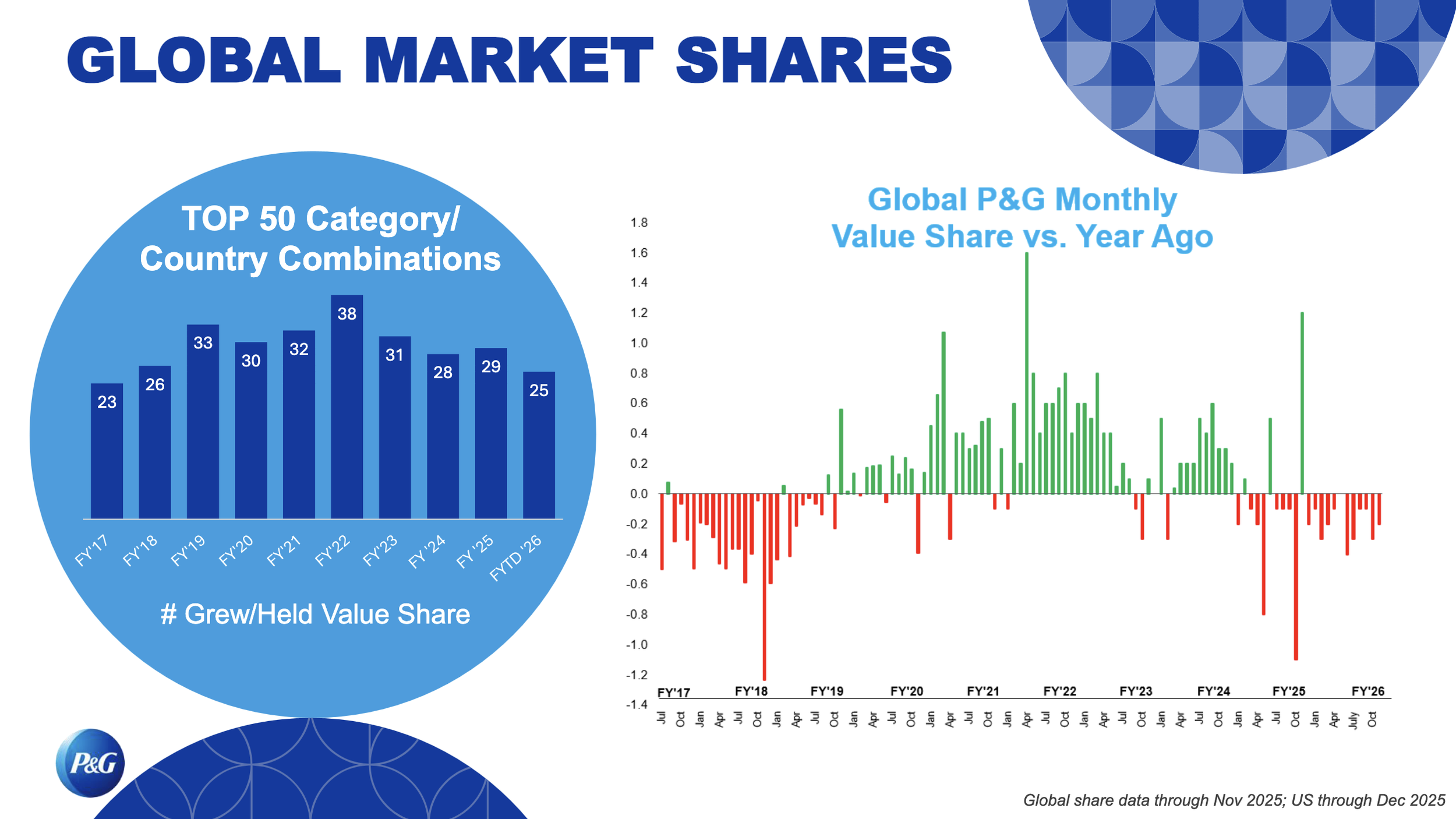

One slide I found worrying (for them) was this one, showing half of their top 50 brands lost market share.

Their guidance for the rest of the year is already going to be off, I think – as they probably weren’t considering more war in the Middle East. They were projecting flat to 4% organic sales growth and a neutral impact from commodities. Well, that’s got to be wrong now, right?

As always, the call itself was pretty interesting. But I found worrying sentiments about the macroeconomy (and bear in mind this is before the whole Iran thing blew up):

Some key points:

• Inflationary Pressures: They noted that cumulative inflation across food, energy, healthcare, and other essential spending areas has taken a toll on consumers. This sustained pressure is actively changing how consumers assess the "value" of products. [read – trading down]

• Supply Chain and Weather Disruptions: In the US, the quarter's baseline was heavily impacted by port strikes and hurricanes in early October, as well as the fear of additional port strikes in late December. This caused volatile trade and consumer "pantry loading" dynamics, particularly impacting the Baby, Feminine, Family Care, and Fabric/Home Care sectors.

• Regional Economic Challenges:

o Greater China: Was explicitly described as remaining a "challenging consumer environment."

o Europe: While countries like France, Spain, and Italy saw strong growth, Germany experienced a "softer period."

• Future Macro Risks: While forecasting the remainder of the fiscal year, management noted they are closely watching potential risks including significant currency weakness, commodity cost increases, geopolitical disruptions [this is the one], and major supply chain issues, though current commodity costs are roughly in line with the prior year [this is not happening now though].

• Retail and Media Fragmentation: The company noted a shift in the macro retail environment, characterized by media fragmentation, the rise of social/retail media, and e-commerce growth vastly outpacing offline sales (e.g., in China, e-commerce is growing at nearly 10x the pace of offline retail).

The Q&A session yielded some gems. :

There was some skepticism about the second half being better than the first – well I think that honestly is not happening now for obvious reasons.

Analysts asked for specifics on how P&G will win in a fragmented market. Management introduced their focus on a "Stronger Core, Bigger More" approach. [what an awful sounding program – to me] They admitted they need to execute better on their flagship items (like the Tide liquid relaunch) while successfully introducing premium innovations (like Olay treatments and Venus razors) to capture consumers willing to pay for higher-tier benefits. This sounds similar to the Unilever Top 30 premiumization strategy we talked about last time.

So, in my opinion – not a great set of results for P&G and the outlook, given what’s happening with oil and such (more below), I don't think is that great.

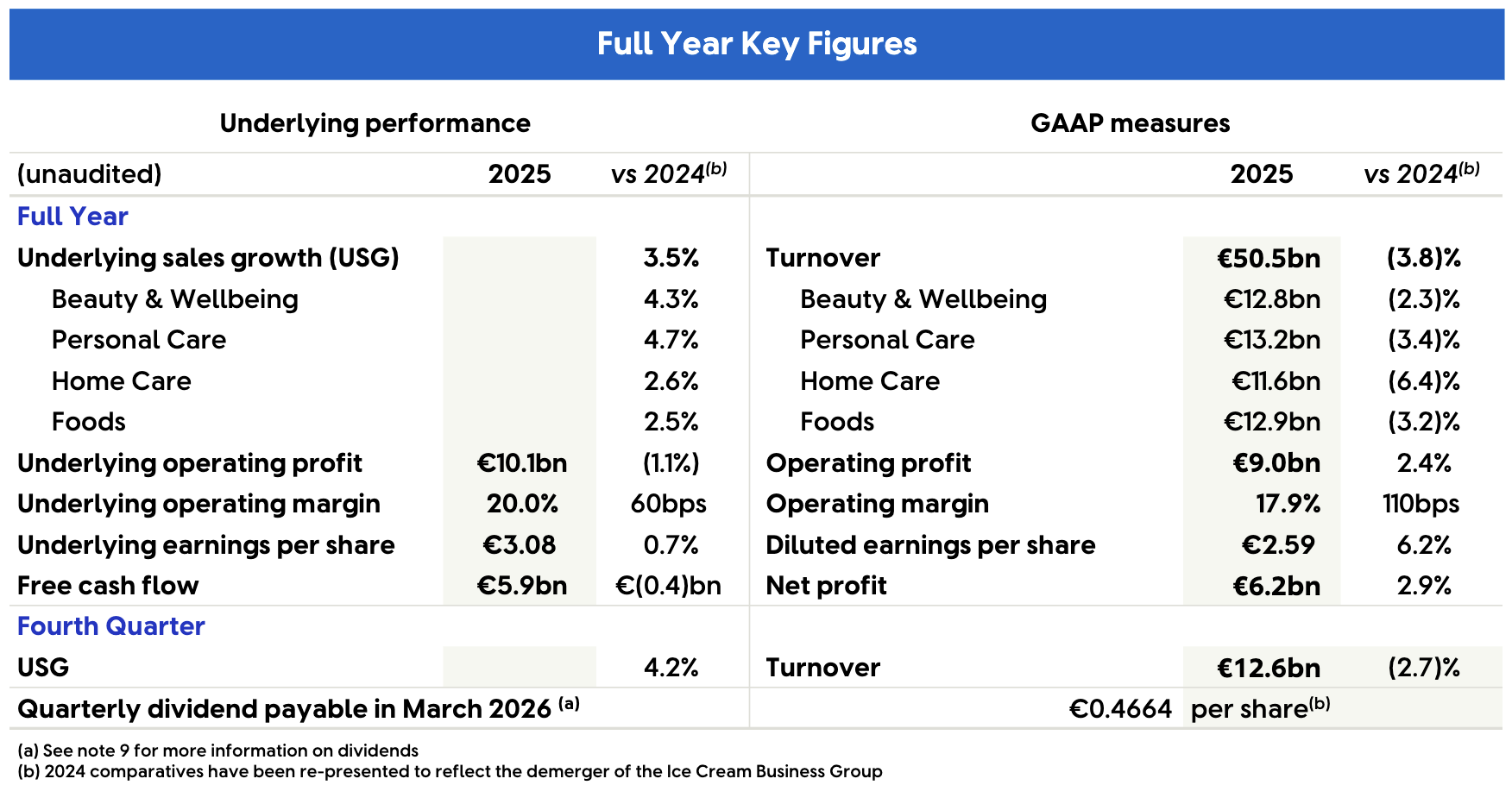

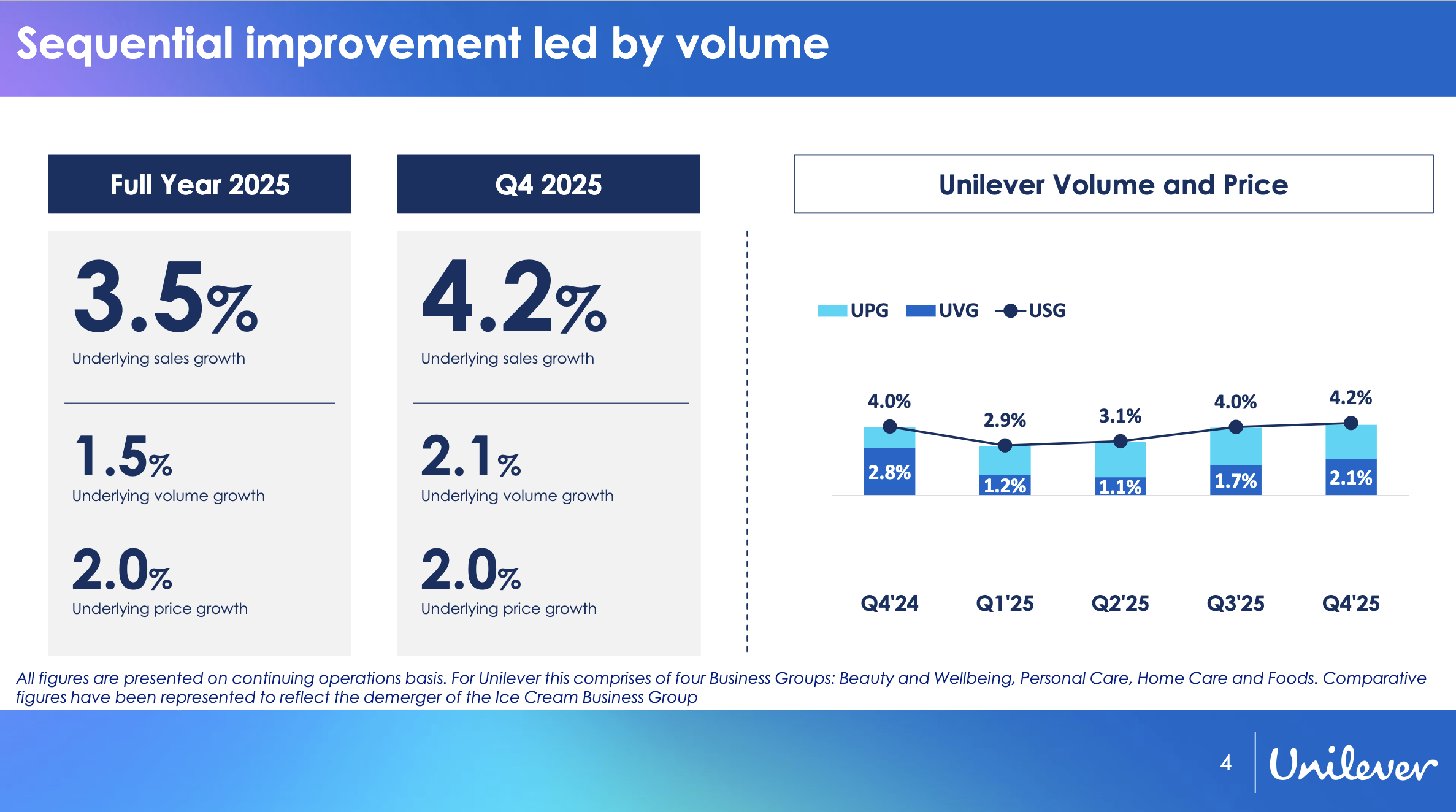

Unilever’s up next. They were reporting full year results for 2025. And again, this was before all the Iran mess kicked off. Overall, it seems the company saw stronger growth than P&G. While GAAP measures saw decreased sales and increased margins and profit, underlying sales growth clocked in as positive. Here’s the box score.

The underlying sales growth of 3.5% came 2% from price and 1.5% from volume. Good. Power Brands (I think that’s their top 30) continued to lead growth delivering 4.3% underlying sales growth in 2025, with 2.2% volume.

Segments:

Beauty & Wellbeing: 4.3% underlying sales growth was led by double-digit growth in Wellbeing, Dove and Vaseline. Underlying sales growth of 4.7% in the fourth quarter was driven by a stronger Asia Pacific Africa delivery which offset slower growth in the Wellbeing market.

Personal Care: 4.7% underlying sales growth was supported by market share gains, premium innovations, and commodity-driven price increases. In the fourth quarter, underlying sales growth remained strong at 5.1%.

Home Care: 2.6% underlying sales growth was led by volume. Underlying sales growth accelerated to 4.7% in the fourth quarter with 4.0% volume supported by a sequential improvement in key emerging markets.

Foods: [Did ok, but not going to mention here because it’s not core and, subsequently was announced will be spun off to McCormick]

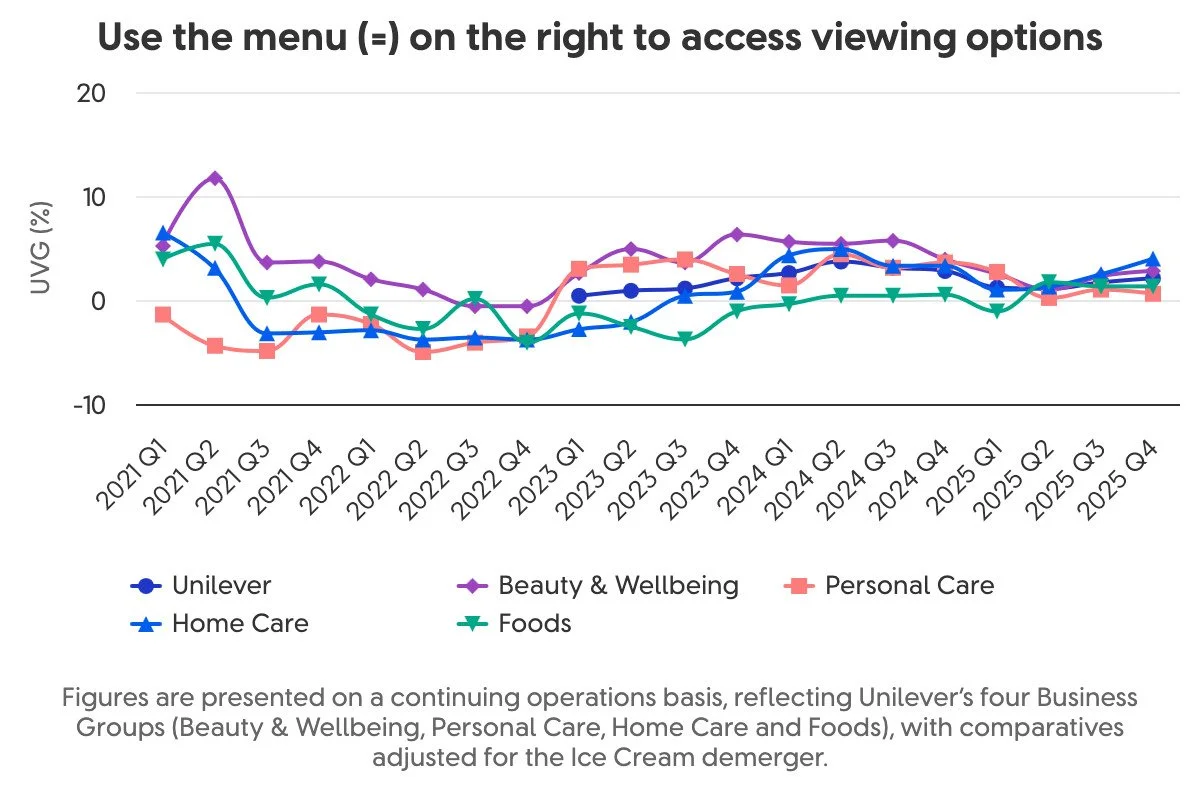

The website featured some interesting growth charts, ie this one showing historic segment growth:

In the presentation and call, they stressed growth – for example in this chart:

So – what about the macroeconomy? (reminder Pre – war) In the call and presentation they noted:

• Uneven Market Conditions: UL described the macro and consumer backdrop as "uneven" and "subdued," noting that consumer conditions softened particularly in the second half of the year. They expect conditions to remain challenging with soft markets in many parts of the world moving into 2026.

• Developed vs. Emerging Markets: Developed markets saw softer retail conditions and weaker consumer demand (particularly in North America and Europe towards the end of the year). Conversely, emerging markets showed resilience and improved performance throughout the year, acting as a competitive advantage for Unilever.

• Latin American Challenges: A broad-based market slowdown was noted in Latin America, driven by ongoing macroeconomic and political uncertainty, specifically highlighting tough environments in Brazil and Mexico.

• Inflation Dynamics: Overall commodity inflation for 2026 is expected to be lower than in 2025 [interesting! Again pre-war]. Inflation is not broad-based; it is currently concentrated in specific materials like palm oil, palm kernel oil, and surfactants [since the war LAB etc. also ]. Conversely, the company is seeing deflation in other areas, such as packaging and certain food commodities. However, wage inflation remains a factor across global markets.

Then some interesting snippets from the Q&A:

• Unilever expects overall pricing growth to be around the 2% level for 2026, normalizing from recent years.

• Gross margins are expected to expand further in 2026, driven by productivity savings, mix (portfolio and geography), and active commodity risk management.

• Power Brands vs. The Rest: Unilever is heavily prioritizing its top brands. "Power Brands" (which make up 78% of revenue) grew strongly at nearly 6% in Q4. Non-Power Brands saw a volume decline of 1% for the year, accelerating to -3% in Q4. The company will continue to aggressively funnel incremental investment into Power Brands.

• Productivity: The company delivered €670 million in savings in 2025 (mostly in SG&A/general overheads) and is on track to complete its €800 million savings program in 2026.

• Capital Expenditure (Capex): Capex will remain around the 3% level. 55% to 60% of this spend is specifically allocated to productivity and margin-enhancing initiatives, while still fully covering the capacity needs required for growth.

OK – a decent 2025 but I have concerns about ’26 turning out as well as projected given a clear run up in chemical input costs due to the Iran situation.

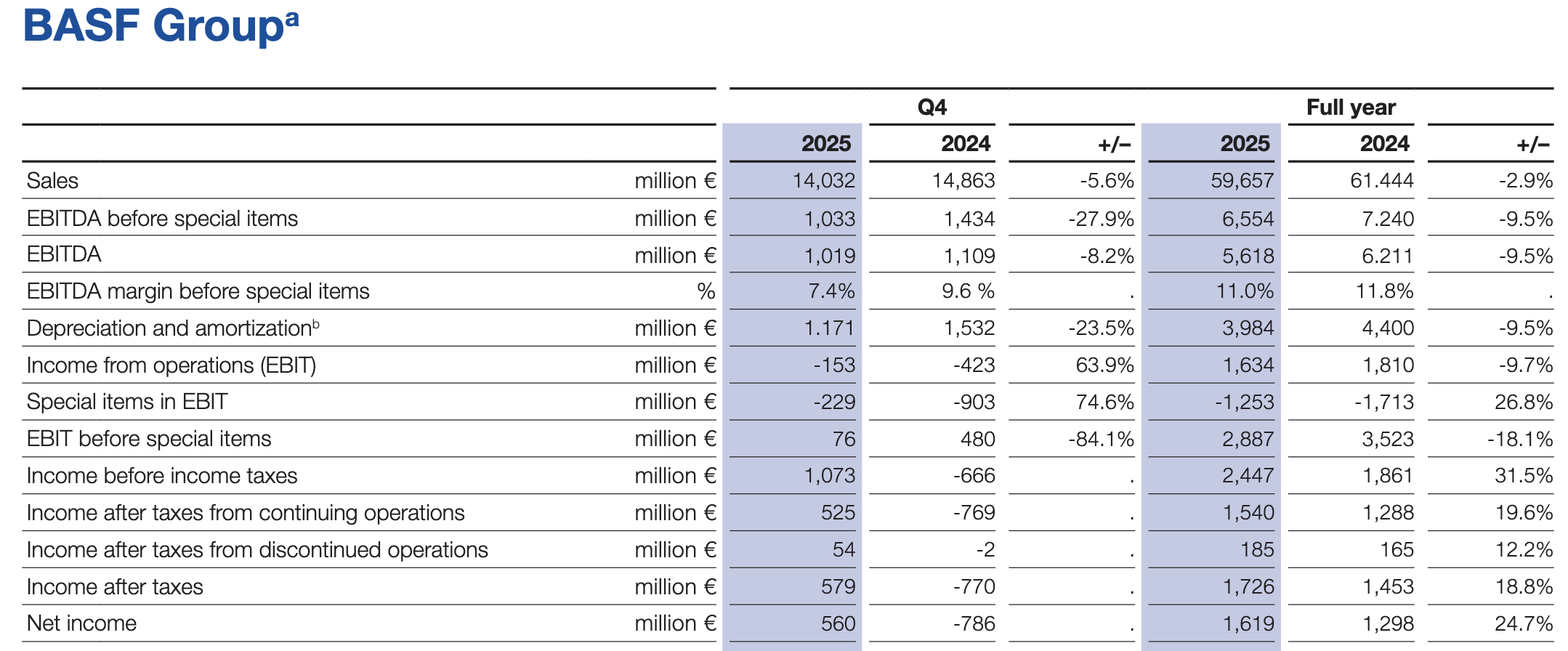

Next up, BASF. Sales were down 2.9% on the year. EBITDA down 9.5%. Although net income grew. Here’s the box score.

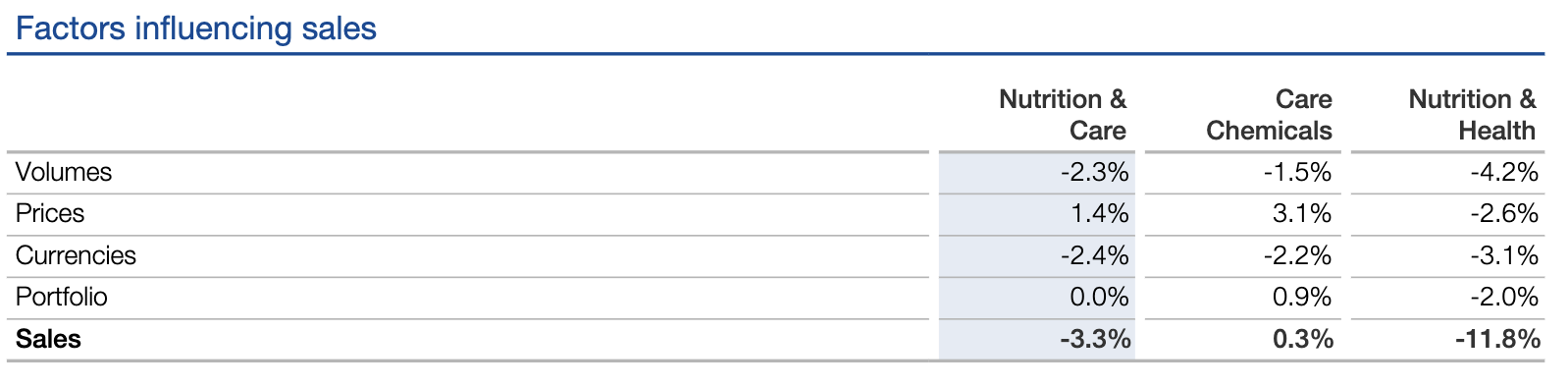

Now, we’ll dig right into the Nutrition & Care (N&H) segment because that’s where all (most) of the surfactants are. In fact they are concentrated in the Care Chemicals division inside N&H. Sales in the Nutrition & Care segment amounted to €6,509 million in the 2025 business year, a decrease of €221 million, primarily due to the decline in sales in the Nutrition & Health division. The Care Chemicals division, on the other hand, recorded a slight improvement in sales, mainly due to positive price trends. Volume was also down in Care though. Here’s a bit more detail:

The company called out lower demand, especially in home care and industrial & institutional cleaning and in the oleo surfactants business area.

In the earnings call, not much discussion of surfactants. However it was noted:

• Consumer Behavior Shift: Because of low consumer confidence, shoppers have increasingly switched to "white label" (store brand) products. This shift resulted in lower demand from global brand owners, which is traditionally a stronghold for BASF.

• Pricing and Margins: Despite the challenges, the Care Chemicals division was able to almost maintain its price levels compared to Q4 2024. However, the segment reported considerably lower margins overall due to competitive pressure and challenging market dynamics.

• Management Clarification: During the Q&A, an analyst characterized the Care Chemicals business as "challenged." CEO Markus Kamieth pushed back, clarifying that he did not want to portray the business too negatively.

• Market Health & Recovery: Kamieth stated that while the last six months had challenging dynamics, the overall Care Chemicals market (including home and personal care) remains "healthy." He noted that BASF is currently seeing a volume recovery in this space.

• Future Profitability: The company is implementing strong "self-help" measures and bringing new capacities online, specifically mentioning new capacity in China. Kamieth noted that these actions will lead to a "pretty significant" incremental increase in profitability for the segment.

A few interesting points on the global macroeconomy:

• Slowing Global Growth: BASF expects global GDP growth to be slightly lower and global industrial production growth to be significantly lower in the near future compared to 2025 levels. They forecast a further decline in chemical production within mature economies and weaker growth across emerging markets.

• Persistent Geopolitical and Market Volatility: The macroeconomic environment remains "highly uncertain and very volatile." BASF explicitly noted that they do not expect a meaningful market upswing or any significant easing of geopolitical and trade-related tensions in the near term.

• Regional Demand Divergence: Demand is highly fragmented by region. While China showed positive volume development early in the year (partly aided by the timing of the Chinese New Year), volume development in the rest of the world has remained weak. Europe, in particular, continues to face severe structural competitiveness challenges and subdued demand.

• Baseline Commodity and Currency Assumptions: For its future macroeconomic planning, BASF assumes an average oil price of $65 per barrel [uh oh…] of Brent crude and an exchange rate of $1.20 per Euro. The company also highlighted that strong currency headwinds—specifically the depreciation of the US Dollar, Chinese Renminbi, and Indian Rupee—have been a persistent drag on global sales.

• Regulatory and Carbon Cost Pressures: The macroeconomic landscape in Europe is being heavily influenced by regulatory costs, specifically the Emissions Trading System (ETS). BASF noted that the rising costs of CO2 certificates create a significant competitive disadvantage for European industrial production, incentivizing the transfer of production to other regions globally.

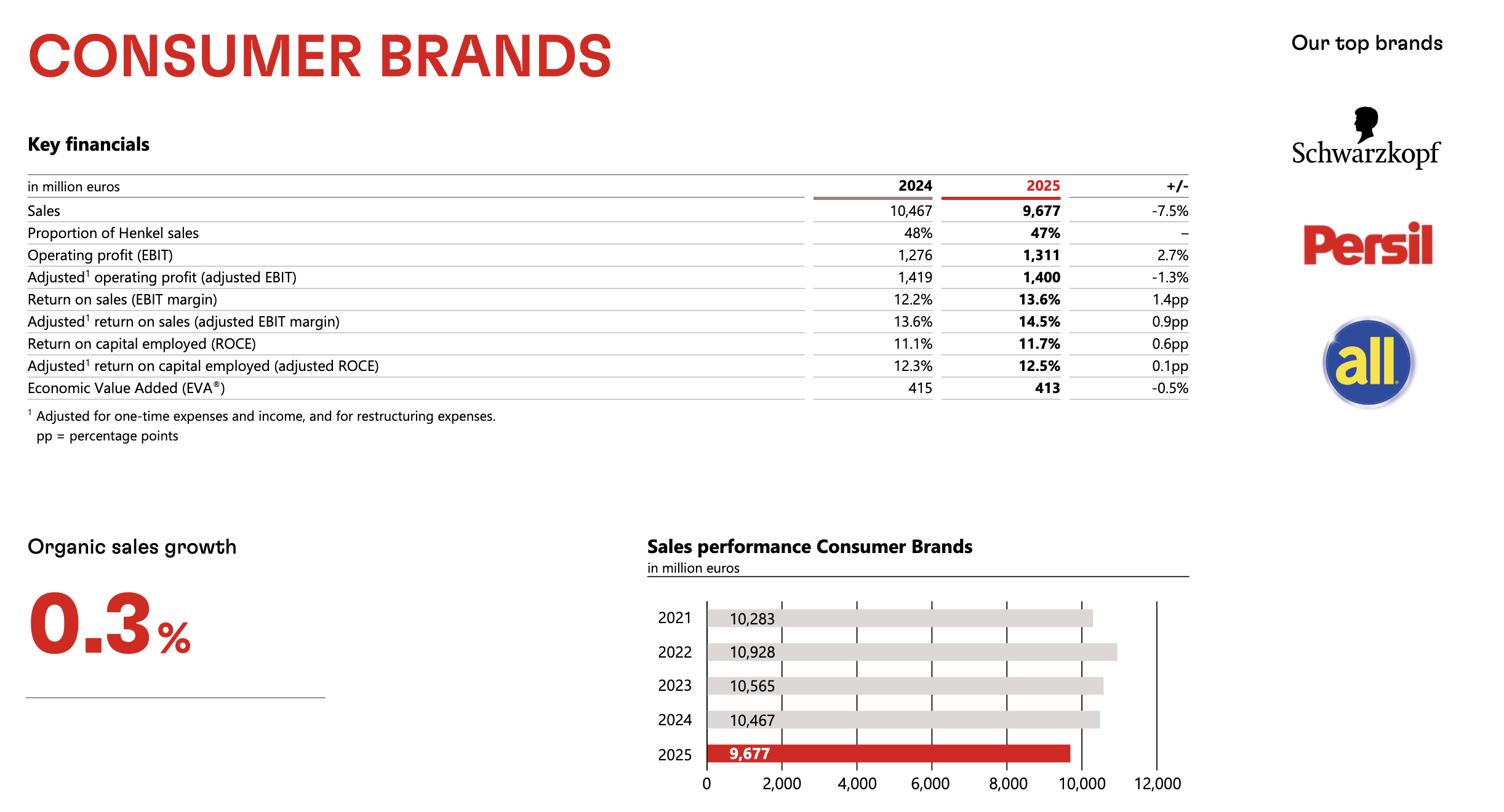

Alright – let’s do Henkel real quick. Sales and EBIT down. Let’s home in on consumer brands, a 9.7 Billion Euro revenues business. Having a struggle to grow as the chart below shows.

More details on consumer brands:

• Nominal sales were €9,677 million, a decrease of -7.5% from 2024. However, this drop was largely driven by negative foreign exchange effects (-4.4%) and divestments (-3.4%), notably the sale of the North American retail brands business. Organic sales grew by +0.3%, which apparently had a bit of pricing and volume in there.

• Adjusted return on sales (EBIT margin) rose by 0.9 percentage points to 14.5%, generating an adjusted operating profit of €1,400 million.

• Sub-Segment Performance:

o Hair: Delivered organic growth of +3.2%, driven by both consumer products (core brands like Syoss, Schwarzkopf Creme Supreme, and got2b) and professional salon businesses.

o Laundry & Home Care: Saw an organic sales decline of -0.9%. While fabric cleaning and finishing categories declined, fabric care saw some increases (driven by Perwoll). Home Care grew, particularly in hand-dishwashing (driven by Pril).

• Subdued Consumer Sentiment: Global private consumption grew by a moderate 3%, but growth was hampered by subdued consumer sentiment due to persistent inflation (around 3.5% globally). Henkel noted a "noticeable weakening" in consumer sentiment in North America during the second half of the year, which weighed on volumes in that region.

• Geopolitics & Trade Policies: Ongoing regional conflicts and protectionist trade policies (including new US tariffs) created supply chain uncertainties.

• Core Inputs: The primary direct materials for this unit include washing-active substances (that’s what they call surfactants) and inorganic raw materials.

• Input Pricing Trends: Overall direct material prices increased by a mid-single-digit percentage in 2025. Interestingly, while the prices of oil and petrochemical derivatives declined over the course of the year [Well that’s over now], the prices for natural raw materials (like palm kernel oil) rose.

• Transition to Sustainable Chemistry:

o Palm & Palm Kernel Oil: These are the most critical renewable raw materials for the production of Henkel's detergents, household cleaners, and cosmetic products. Henkel is heavily focused on supply chain traceability and achieved 98% responsibly sourced/certified palm (kernel) oil in 2025, partnering with groups like Solidaridad to support smallholder farmers and prevent deforestation.

o Substances of Very High Concern (SVHC): Henkel is actively executing a "Responsible Chemistry" approach to phase out potentially harmful chemicals ahead of regulatory bans. For example, in 2025, the Consumer Brands unit successfully reduced the use of cyclosiloxanes across its hair care portfolio globally.

o Biodegradability: Because most Consumer Brands products (like detergents and shower gels) pass into wastewater after use, the unit’s raw material strategy is highly focused on replacing non-circular, petrochemical ingredients with renewable, biodegradable alternatives, even though this sometimes leads to higher raw material costs.

The investor call was in German but Google Gemini 3.1 had no problem with it and gave me the following key points from the Q&A relating to the consumer brands business.

• No Plans to Split the Company: CEO Carsten Knobel gave a "very clear no" when asked if creating independent legal entities for the business units was a step toward splitting or spinning off parts of the group. The legal restructuring is solely intended to make internal processes and structures more agile and to support the company's future growth agenda.

• Top 10 Brands are Driving Growth: Profitability in the Consumer Brands division was largely fueled by its top 10 brands. These leading brands contributed disproportionately to the division's success, growing roughly 300 basis points above the average of the overall business. This growth was achieved through both volume and price increases.

• Strong Performance and Expansion in Hair Care: The hair business has developed very positively over the past few years. Henkel has actively strengthened this segment through strategic acquisitions, including the professional business of Shiseido and Vidal Sassoon in Asia, as well as the recently announced acquisition of the fast-growing brand "Not Your Mother's."

• Integration Savings Exceeded Targets: The integration of the formerly separate consumer businesses into a single Consumer Brands platform was successful. It generated €540 million in savings.

OK – well that’s it for earnings. I’d say all companies had a tough 2025 but I worry that their uniformly sanguine* outlooks for 2026 (note that $65 / barrel oil assumption for BASF!) are now derailed due to the Middle East fracas. And that all of course, ripples back through the supply chain. I hope it all ends up being worth it. What do you think?

[*Cool word right? It’s from the latin word sanguis – blood. During the Middle Ages, health and temperament were believed to be governed by the balance of different liquids, or humors, in one's body. If any of those four humors – phlegm, black bile (also called melancholy), yellow bile (or choler), and blood – predominated, then your disposition and health were said to be ruled by that humor. A "sanguine" temperament was governed by an abundance of blood, believed to make a person confident, cheerful, and optimistic.]

For those that follow this type of thing; L’Oreal brand Garnier signed blog favorite, the great Gisele Bundchen as global ambassador. This is in contrast to L’Oreal’s engagement of a literal card-carrying pornstar (Do they carry cards? Readers, please let me know…) for their brand the aptly named Urban Decay (as reported in prior blogs). Now this is the point at which a lesser blog might feature a photograph of Ms Bundchen. However, for reasons detailed at the end of the blog, you will just have to use your imaginations here.

I’ve always considered Beiersdorf a canary in the European skin-care coalmine (what a mixed metaphor) so while 2025 results were OK the outlook is a bit depressing. i.e.:

• Beiersdorf reported 2025 group organic sales of €9.9bn (+2.4%), with the consumer business growing 2.5% to €8.2bn.

• Eucerin and Aquaphor drove overall growth, up 11.7%.

• Nivea (the company's largest brand) grew by only 0.9%, missing targets due to a global skincare slowdown and business restructuring in China. Luxury line La Prairie saw a 4.5% decline in sales.

• Beiersdorf is adopting a "conservative" outlook for 2026, citing continued market volatility and cautious consumer demand. The company expects organic sales in its consumer business to be only "flat to slightly growing."

• Furthermore, the company expects its EBIT margin to dip slightly below 2025 levels, pressured by rising raw material costs among other things.

Beiersdorf per Grok

A few blogs ago, we reported that First Quality (of Great Neck, NY) bought some non-core detergent brands from Henkel. I now read in HAPPI that the company plans to build a $300Million plant for the business in Archbold, OH (40 milese SW of Toledo). They’ll also be putting together an R&D center in Trumbull. I wish them much success. By the way, potential suppliers, they have an ingredient library online here https://www.firstquality.com/products-and-services/ingredients/Library It may not cover all their end products yet, but it’s a good start.

Speaking of Henkel. As noted they recently acquired haircare brand Not Your Mother’s which seems targeted at young folks despite claiming to be for all ages. They support the SVP Food Pantry though, so that’s good. Ingredients? I took a look at their Aura Boost thickening shampoo and it’s built on Sodium Cocoyl Isethionate, Sodium Lauroyl Methyl Isethionate and Cocamidopropyl Hydroxysultaine. Is it my imagination or am I seeing more and isethionates these days? Anyway, here’s Blythe - at this link - explaining why she uses it (Aura boost, that is, not isethionates).

And also speaking of Henkel the company announced another (much bigger) haircare deal, an agreement to acquire the fascinating Olaplex company at a transaction value of $1.4 EBITDA. As noted by Henkel, Olaplex is a premium channel hair care brand with a portfolio of science- led, high-performance products. Olaplex maintains a balanced global footprint, with sales split between the U.S. and key international markets. In fiscal year 2025, OLAPLEX generated around 370 million euros in sales. Now I read further in Beauty Independent here, an excellent article. They opine that Olaplex is not at its peak and will take some fixing up by Henkel. Henkel buys the company at 10% of (that’s of not off) it’s $14Bn IPO valuation in 2021. This decline is attributed to competition from newer brands (so faddishness then?) and an ultimately dismissed lawsuit alleging their products caused hair loss. Following this a new CEO, Amanda Baldwin was brought in to turn the company around. Is there any further proof needed that we are living in a simulation? (Hair loss, Baldwin?.. sorry that’s just puerile, I know). Anyway, I’m no expert but 13.7X doesn't seem like a crazy price and if anyone can right the ship on this type of brand it’s Henkel. I wish them well. What’s in there? I picked one of their best-selling shampoos Olaplex Number 4 – Bond Maintenance. It’s built on – guess what? Isethionate! But look at the entire list. That’s a lot of ingredients. I think too many right? What do you think?

Water/Aqua/Eau, Sodium Lauroyl Methyl Isethionate, Cocamidopropyl Hydroxysultaine, Potassium Cocoyl Glycinate, Disodium Cocoyl Glutamate, Sodium Lauroyl Sarcosinate, Potassium Cocoate, Decyl Glucoside, Glycereth-26, Bis-Aminopropyl Diglycol Dimaleate, Cocamidopropylamine Oxide, Disodium Laureth Sulfosuccinate, Glycol Distearate, Sodium Cocoyl Glutamate, Methyl Gluceth-20, Acrylates Copolymer, PEG-120 Methyl Glucose Dioleate, Amodimethicone, Citric Acid, Sodium Lauryl Sulfoacetate, Polyquaternium-10, Ethylhexylglycerin, Divinyldimethicone/Dimethicone Copolymer, Polyquaternium-11, Trisodium Ethylenediamine Disuccinate, Guar Hydroxypropyltrimonium Chloride, C11-15 Alketh-7, Laureth-9, Glycerin, Trideceth-12, C12-13 Alketh-23, C12-13 Alketh-3, Panthenol, Acetic Acid, Hydrolyzed Vegetable Protein PG-Propyl Silanetriol, Pentasodium Triphosphate, Glyoxal, Sodium Hydroxide, Helianthus Annuus (Sunflower) Seed Oil, Disodium EDTA, Tocopherol, Prunus Armeniaca (Apricot) Kernel Oil, Pseudozyma Epicola/Argania Spinosa Kernel Oil Ferment Filtrate, Pseudozyma Epicola/Camellia Sinensis Seed Oil Ferment Extract Filtrate, Quaternium-95, Propanediol, Helianthus Annuus (Sunflower) Seed Extract, PEG-8, Euterpe Oleracea Fruit Extract, Punica Granatum Extract, Rosmarinus Officinalis (Rosemary) Leaf Extract, Musa Sapientum (Banana) Fruit Extract, Origanum Vulgare Leaf Extract, Morinda Citrifolia Fruit Extract, Arctium Lappa Root Extract, PEG-8/SMDI Copolymer, Sodium Hyaluronate, Palmitoyl Myristyl Serinate, Sodium Polyacrylate, Pentaerythrityl Tetra-Di-T-Butyl Hydroxyhydrocinnamate, Biotin, Phenoxyethanol, Chlorphenesin, Benzoic Acid, Potassium Sorbate, Sodium Benzoate, Fragrance (Parfum), Hexyl Cinnamal, Limonene, Citral

Do you know the US’s number 2 detergent brand? Well, I read in HAPPI, it’s P&G’s Gain (Number 1 is Tide). And Gain is launching a new range of products, Gain Plus. Gainiacs will love it, no doubt. What’s in this new product? Here’s the complete IL: Cleaning Agents (C10-16 alketh; sodium and MEA C10-16 alkylbenzenesulfonate; C10-16 alkyldimethylamine oxide; sodium laureth sulfate), Stabilizers and/or Process Aids (calcium and/or sodium formate; hydrogenated castor oil), Water Softener (sodium and MEA citrate), Enzymes (subtilisin; amylase enzyme; cellulase enzyme; mannanase enzyme), Cleaning Aids (polyethyleneimines alkoxylated; tetrasodium glutamate diacetate), Odor Removers (methyl di-t-butyl hydroxyhydrocinnamate; diethylenetriamine), Solvents (alcohol; ethanolamine; may contain: propylene glycol, sodium cumenesulfonate), Preservative (benzisothiazolinone), Colorants, Fragrances, Water. Do you see any surprises? (I don’t but curious if any readers do)

By the way, I also read that Mr. Clean is launching a new magic eraser for tubs and showers and such. Here’s that IL. Much simpler: C9-11 Alketh-8, PEG, Fragrances, Colorants. Yes, it’s Neodol 91-8 (I’m guessing).

Ever wondered about polyglyceryl esters used in skincare and other personal care apps? Well check out this article in the Great HPC Today. It says the market is $690 Million. This seems a bit high to me, but that’s just my gut feel. Interested in what others think.

Around the middle of the month (March 18th), I got the announcement from BASF. Prices are going up. Way up. How could they not? According to the company BASF is increasing prices on all products in its Home Care, Industrial & Institutional Cleaning (I&I) and Industrial Formulators portfolio in Europe by up to 30%, or more for selected products, effective immediately or as existing contracts allow. You can read the whole thing here. https://www.basf.com/global/en/media/news-releases/2026/03/p-26-052

For those concerned about scrutiny and limits on EO, The Environmental Protection Agency said repealing the rules, which fall under the National Emission Standards for Hazardous Air Pollutants, would “safeguard the supply of essential medical equipment” — saving approximately $630 million for companies over 20 years. You can read more in the LA Times here.

Industry in Europe seems finally to be growing a pair getting more vocal about government regulatory overreach. L'Oréal Groupe CEO Nicolas Hieronimus and Beiersdorf CEO Vincent Warnery are among the top business leaders to warn over the regulatory burden being placed on the beauty industry in Europe. The Value of Beauty Alliance – a group of top executives from 17 beauty and personal care companies – has called on EU policymakers to take action, or risk a weakening of one of the region’s most competitive and globally influential industries. You can learn more here. I hope it’s not too late.

And also more vocal; APAG and CESIO published a letter on LI (and other places) critiquing Europe’s Dumbest Regulation (EUDR). They highlight that it: undermines industries' competitiveness, puts18,000 direct EU jobs at risk, prompts oleochemical and surfactant production relocation and a shift to fossil-based alternatives. Read the whole thing here.

Members finally speaking up

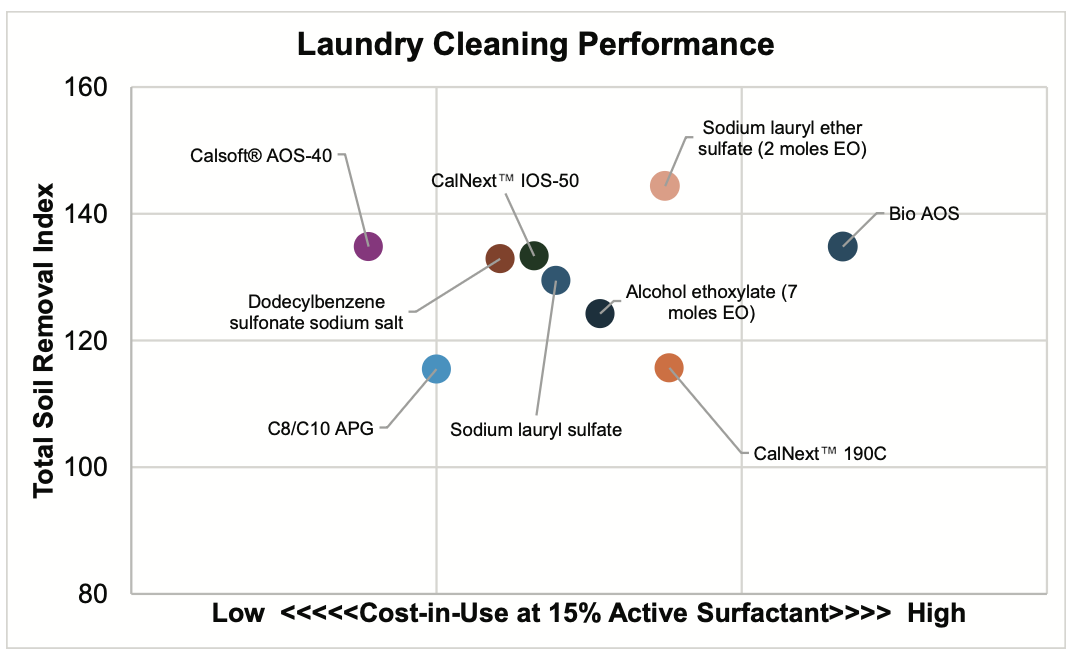

The great Pilot Chemical (where I cut my teeth, earned my spurs and all that) has published a pamphlet called “Calsoft AOS Anionic Surfactant- An Oldie but Goodie”. I have a copy of it but now I can’t find a link to it on their website. So anyway – maybe you can ask your sales rep. There’s some cool data and graphs in there, including this one:

Cool right?

The publication focuses on household applications and so I eagerly await a companion focused on personal care. It’s very good marketing for an old classic surfactant. Of course Pilot has always had excellent marketing since, oh .. back in the early 90’s. My objective assessment anyway.

Also on AOS, the great Colonial Chemical has published a succinct guide entitled “A Case Study in Substitution: From Sodium Laureth Sulfate to Sodium C14-16 Olefin Sulfonate” In summary they note, among many other things, that “While SLES remains a well-established surfactant, AOS is an increasingly popular option with superior short-term advantages in cost efficiency, regulatory compliance, formulation ease, and consumer acceptance.” Read the whole thing here. It has some great information.

More Unilever. I read in the great HAPPI that Unilever’s Dirt Is Good—its Persil and Comfort fabric care brands—unveiled SmartSeries, billed as the first detergent and conditioner designed specifically for auto-dose washing machines. I am surprised by that claim but fine, I’ll take it at face value. The products, designed for use in auto-dose washing machines with reservoirs, was created in collaboration with Samsung Electronics. But what’s in there? I couldn't get a lot of detail, unfortunately (unlike for the P&G products noted above … ahem). But here’s what’s on the website:

Persil Smart Series Advanced Clean Non-Bio

• 15-30%: Anionic surfactants.

• 5-15%: Non-ionic surfactants.

• <5%: Phosphonates, Perfume, Soap, Optical brighteners, Benzisothiazolinone.

Comfort Smart Series Azure Bliss

• 5-15%: Cationic surfactants.

• <5%: Non-ionic surfactants, Perfume, Alpha-Isomethyl Ionone, Citronellol, Dimethyl Phenethyl Acetate, Eugenol, Linalool, Linalyl Acetate, Pogostemon Cablin Oil, Terpineol, Tetramethyl Acetyloctahydronaphthalenes, Benzisothiazolinone.

Terra Mater, the Belgian company continues to do very interesting things. Their latest is Guerbet esters based on Castor Oil. Liquid emollients, silicone alternatives etc. The process involves a multi-step process cracking of castor oil to 1-heptanol. Guerbet dimerization of 1-heptanol to 2-pentylnonanol followed by esterification with undecylenic acid or ricinoleic acid. Learn more about the company here: https://www.terra-mater.be/

I am quite close to the company, Norfalk of Denmark. One of their folks published an interesting article in the great HPC Today on biocatalysis in surfactants. In summary, they look at conventional chemical synthesis, fermentation, and biocatalysis. They claim that, while traditional synthesis remains scalable but relies on non-renewable (or sustainability challenged) feedstocks, fermentation offers natural pathways yet faces challenges. The article highlights biocatalysis as a promising technology. It’s worth a read in full here.

And from Stepan, something on LI that says, in part – and I quote “Discover NOVATENSIA™ SL: Stepan’s newest biosurfactant brand. Following the exclusive distribution partnership between Stepan and AmphiStar, we are pleased to announce the launch of NOVATENSIA™ SL, a new brand developed to support more sustainable solutions for the Home Care and Industrial & Institutional (HI&I) cleaning markets in EMEA.” [That’s not a bad name in my opinion, Novatensia. So it looks like Stepan is re-branding the sophorolipids from Amphistar to sell in Europe. Let’s see how it goes. I wish both companies well. ]

And speaking of Amphistar, the EU’s SurfsUp project posted on LI that they were exhibiting in Brussels at a circular conference “𝘿𝙞𝙨𝙝𝙩𝙧𝙤𝙮𝙚𝙧", the new dishwashing liquid developed by SurfsUp partner AmphiStar, formulated with biosurfactants produced within the SursUp project. Dishstroyer eh? OK – it’s a fun name to be sure.

Is building a plant part of your new surfactant business plan? If so read this article from Liberation BioIndustries. It’s called. Learn Before You Lock: Protecting Capital in FOAK Biomanufacturing. FOAK stands for First of a Kind. It’s quite relevant.

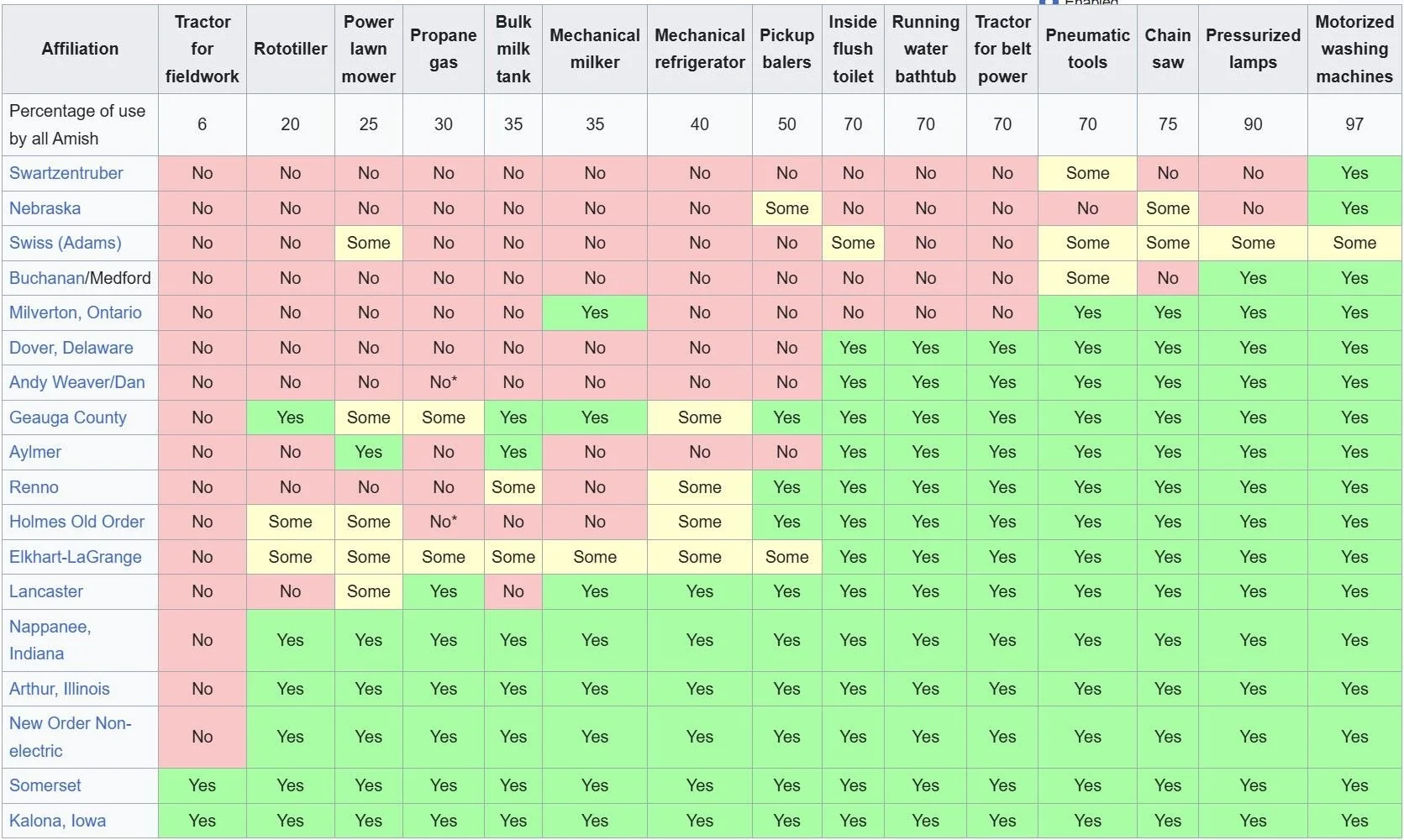

And finally, Rodrigo Menabrito of Novonesis posted a fascinating piece of information on LI, here. He says that The washing machine might be the only modern invention embraced by every Amish group — at least partially. Here’s the chart. I love this for obvious reasons.

Interesting?

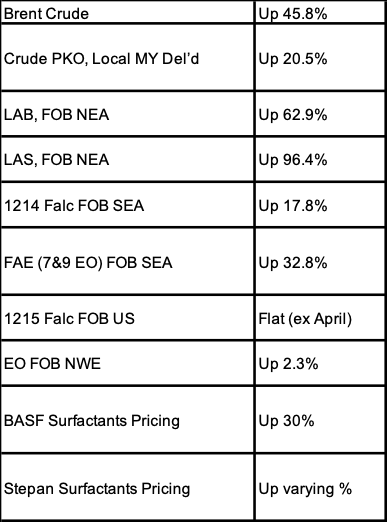

Market News:

What a crazy time. I’m going to depart from our normal format a bit, just to give you a sense of, overall what’s been going on with prices and costs in the surfactant markets.

Between February 27th and April 2nd (day of writing this):

And more to come…

Qualitatively, this is what’s going on in some key markets:

Asia's fatty alcohol ethoxylates (FAE) market is seeing an upward price surge for May shipments, driven by escalating feedstock fatty alcohol mid-cuts and a supply crunch in ethylene oxide. Spot availability for FAE is limited due to regional plant shutdowns for maintenance. Demand remains tepid despite Chinese players returning from the new year and sluggish trades in Southeast Asia due to Ramadan. Indian FAE imports are seeing higher demand, but face competition from cheaper Chinese material. China's domestic FAE prices have also risen due to cost pressures. The outlook suggests FAE spot offers will remain elevated, demand will pick up as inventories are replenished, and China-origin material will continue to compete in India. Upstream, PKO costs are fluctuating with strong demand in Indonesia, while China's ethylene oxide prices are firm due to tight supply and sharply rising feedstock ethylene costs.

Global fatty alcohol markets are under upward price pressure, with Asia seeing broad increases across all cuts due to escalating feedstock costs and rising demand as buyers restock, though supply is limited by plant maintenance. The US market is also experiencing upward pressure from geopolitical conflicts, which are driving up feedstock and input costs, lengthening lead times, and reducing spot availability, even as Q2 contract negotiations finalize higher. In Europe, mid-cut spot prices are firming on high feedstock costs and tight supply, despite Q1 contract prices reflecting earlier softer feedstock values. Notable developments include the refined timelines for the EU Deforestation Regulation and a new trade deal between Indonesia and the EU aiming to eliminate tariffs.

The Asian linear alkyl benzene (LAB) market is on an uptrend due to tightening supply from reduced plant output and escalating feedstock costs, particularly kerosene and benzene. Buyers are actively seeking material, especially for Q2 manufacturing, and this strong buying interest has pushed LAB sulphonate (LAS) prices even higher than LAB. Geopolitical tensions in the Middle East are contributing to the protracted supply crunch and rising crude oil values, further impacting refining margins and increasing freight/insurance costs. India's market remains tight due to domestic plant maintenance. Several plants across Asia and the Middle East are undergoing or have recently completed maintenance, with new capacity expected from a Middle Eastern supplier. The global sulphur market is facing uncertainty and price increases due to tight supply and strong demand from various industries, while China's soda ash market is stable amid inventory drawdowns and strong downstream demand.

Welcome trolls! As alluded to above in the piece about Garnier and Gisele Bundchen, I have recently been made aware of the existence of so-called copyright trolls. This is a thing. Google it. It’s about images. There’s a Wikipedia entry on them here. Seems the blog has attracted a lot of their attention in recent years. As a result we have gone through the site to make sure that whatever images we use are unimpeachable in terms of copyright. I hope this does not make our blog boring! (let me know). There’s an old trope about only reading Playboy for the articles. But I think most of you read the blog for the keen analysis and information right? And a healthy minority of you head straight to the music section. So, anyway, here’s a troll (made for me by Grok).

Music Section

I’ve not listened to that much new recently but I just had an idea. What about before Rush. What was I listening way back before I really got to know how all-encompassing music could be? There was some good stuff. Here’s some of what I consider formative in my own personal musical canon.

Actually – before we get into this, can I just say something? Forgive me this personal indulgence. A number of people have asked me whether and where I have got my tickets to see Rush in their re-union tour with the new drummer. I have given various vague and non-committal responses. Here’s the thing. I don't have any. Why not? I haven’t been to a concert for a number of years now (the last one was Rush) because I suffer from tinnitus and hyperacusis. I have done so since childhood but recently, I’ve become more protective of my hearing as it naturally deteriorates with age. Today, if I went to a rock concert, it would be physically painful for me. Earplugs help but not much. So, now you know. I usually don't like to share personal stuff like this but I think I owe it to readers who spend time down here in our music section and who indulge me at our conferences as I play various rock anthems to illustrate surfactant related points. Thanks for reading this.

Polovtsian Dances by Borodin – Dude was also a chemist and a doctor!

Well, after Borodin and before Rush there was ELP (and before Neil Peart, Carl Palmer). Here's my favorite track from each of their first 5 albums.

The Barbarian off Emerson Lake Palmer. Note how they pack in rock, prog, jazz and just incredible musicianship in one short track.

The album Tarkus was incredible. Heck - let’s just listen to side one. Honestly there was a time when I thought the first 3 minutes of this was the greatest thing I’d ever heard and would ever hear. Then I heard 4:00 to 5:40. Wow!

Pictures at an Exhibition was recorded at the great Newcastle City Hall, scene of many great concerts (including many by Rush). The Curse of Baba Yaga. Bands weren’t afraid be get experimental in front of audiences back then.

And here’s Trilogy off of Trilogy. You have to just accept the song as it starts. But then, that transition at 3:00 was one of the many things I loved about ELP. Stay with it to the end.

And then the great Brain Salad Surgery. This was my favorite album until it was finally usurped by … you know what (four numbers in a row). Here’s the not often played Karn Evil 9 2nd Impression.

Around the same time as ELP, there was Yes. The album Relayer had 3 songs on it and we thought that was too many! This was my second favorite album before, you know, the one with the images of the brain on it came along. There was always something cold and metallic about this. It was not comfort-music, for sure. And the lyrics! I just got into reading some Emily Dickinson and some of her stuff reminds me of those impenetrable Yes lyrics. Like this… Faster moment spent spread tales of change within the sound / Counting form through rhythm electric freedom / Moves to counterbalance stars expound our conscience / All to know and see the look in your eyes. What the heck? Anyway here’s Sound Chaser. BTW Rush inducted Yes into the Rock ‘n Roll half of fame. This should not surprise you.

And there was also Genesis (proper Genesis with Peter Gabriel). Supper’s Ready was right up there before I heard the song about the Prince and the Dog. This is truly beautiful though, isn’t it? Switch off your phone and listen to all 23 minutes. One of the greatest ever musical pieces demonstrating the genius of this group is between 15:35 and 18:50. BTW that’s not an excuse to skip forward. You gotta listen to the whole thing!

That's it! I will see all you great readers and friends in Jersey City, May 6 – 7th. https://events.icis.com/website/8544/