Surfactants Monthly - February 2026

Welcome new readers! Every so often as we add readers, I publish this reminder. What we put in the blog is publicly available information. That is material that has been published or otherwise disclosed in a public forum (such as at a conference, seminar or in securities filings or earnings calls and similar). We don't traffic in confidential information or rumors or anything like that. Hope that is helpful.

As noted last month, the beginning of February, saw the ACI annual meeting in Orlando (their 100th). I recorded a short video giving you my take on the surfactant vibes from that meeting. The above paragraph applies to our videos also. Here it is:

Macroeconomics:

I’ll be brief here as we have a plethora (that’s a lot) of news this month. Balmoral Advisors has carved out a position as one of the leading chemicals investment bankers in the world, focused on the middle market (BTW – they will be making a rare speaking appearance in May in Jersey City. How rare? Their MD last spoke there in 2011). They recently published an analysis of on liquidity in the US and Canadian Capital systems and what this means for M&A, which I encourage you to read on their website here. Key points:

•$11.5 Trillion Combined Liquidity Pool: The U.S. and Canadian capital systems operate as a single, integrated financial market. Together they hold a combined $11.49 trillion in total cash liquidity, providing a big capital base for transaction financing.

•$3.9 Trillion in Deployable Corporate Cash: Non-financial corporations hold $3.93 trillion in accessible domestic cash (net of a $1.18 trillion adjustment for U.S. offshore holdings), providing large balance sheet capacity for strategic acquisitions.

•$1.4 Trillion PE/VC Overhang: Private equity and venture capital funds are sitting on $1.43 trillion in uninvested commitments, creating pressure from limited partners to deploy capital into new investments.

•Institutional Capital Fueling Sponsors: Holding $850 billion in cash reserves, pensions and endowments are increasingly rotating away from low-yield fixed income into illiquid PE assets, providing potential continuous fund replenishment and sponsorship for middle-market M&A.

•Sustained Sellers' Market: The convergence of cash-rich strategic buyers and PE sponsors mandated to deploy record "dry powder" is driving competition for desirable middle-market assets, maintaining upward pressure on transaction pricing and accelerating deal timelines. So 🚀, I think, right?

Quite a pool of cash

The News

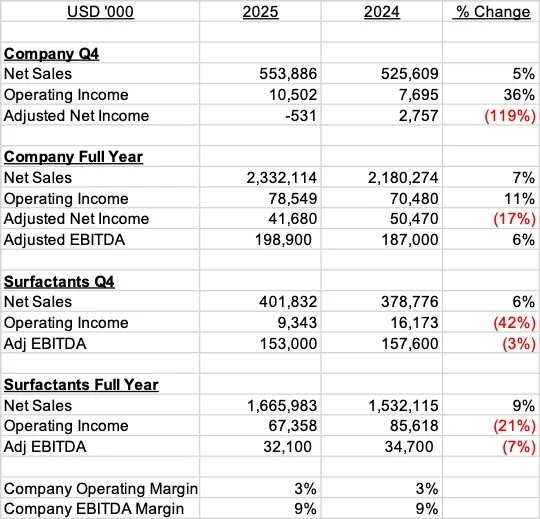

It’s the most wonderful time of the year – earnings season. Stepan (SCL) in particular is a surfactant bellwether and so I listened to their earnings call and pored through the earnings release. Here’s what I learned (with a heavy focus on surfactants).

Adjusted EBITDA for the company in 2025 at $198.9 M was 6.4% up on 2024’s $187.0 M. However there was trouble in surfactants where EBITDA for the year decreased 2.9% from $157.6 M to $153M. The 4th Quarter for the company was particularly difficult. Total EBITDA dropped from $35.0 M to $33.8 M. And most of that was due to surfactants which saw a 7.5% drop from $34.7 M to $32.1 M.

Here’s the box score:

For the company as a whole, Net sales in the fourth quarter of 2025 increased 5% year-over-year. This increase reflects higher selling prices, that were mainly attributable to the pass-through of higher raw material costs and more favorable product mix, and the favorable impact of foreign currency translation. A 3% decline in sales volume partially offset the above.

Here’s a little more color on the surfactants results:

Surfactant net sales were $401.8 million for Q4, a 6% increase versus the prior year. Selling prices were up 10% primarily due mainly to a pass through of higher raw material costs. Sales volume declined 7% year-over-year primarily due to lower demand within the commodity Laundry & Cleaning end markets, lower demand from distributors partners and lower volume in the Philippines due to the asset divestiture. Excluding the impact of the Philippines, volume declined 3%. These declines were partially offset by double digit growth in the Industrial Cleaning end markets and year-over-year growth within the Agricultural and Oilfield end markets. Foreign currency translation positively impacted net sales by 3%. Surfactant adjusted EBITDA for the quarter decreased $2.6 million, or 7%, versus the prior year. This decrease was primarily due to the 7% decrease in sales volume.

For the whole year Surfactants Adjusted EBITDA declined 3%, year-over-year, largely driven by higher start-up expenses associated with the new alkoxylation site in Pasadena, Texas, lower sales volume within Global Commodity Laundry & Cleaning end-markets, and elevated Oleochemicals raw material costs.

Stepan, to their credit, in response to difficult conditions in a core surfactants market, announced a two year program to cut $100M in pre-tax cost, dubbed Project Catalyst. They expect $60 M of that to be realized in 2026. They did mention that they still expected to see 3% inflation on their roughly $750M of fixed costs (so $22.5M) netted against these savings each year. As part of this project they announced 3 consolidations

•Closure of the Fieldsboro, NJ site (sulfonates, betaines and some specialties)

•Staleybridge, UK – Organics asset decommissioning

•Millsdale, IL – Alkoxylation asset decommissioning. Move production to new Pasadena, TX plant

As always, the Q&A session with the analysts following the stock, was instructive and took up more than half of the call.

The big news for me that came out of this portion was that Stepan was already seeing for Q1 of 2026, continued slowdown of surfactants sales (and a little in polymers) – particularly driven by the severe weather over much of the country. They expect this to have a $6M EBITDA impact (That’s almost a fifth of surfactants EBITDA for last year). However, they expect to make this up and still grow overall company EBITDA for the year. Tough start though.

A lot of discussion of oleochemical feedstock volatility:

•Coconut oil (CNO) prices escalated from $2,000/MT to $3,000/MT, which negatively impacted second-half 2025 margins.

•CNO prices have since declined to approximately $2,200/MT, and the spread between CNO and Palm Kernel Oil (PKO) has narrowed to roughly $200/MT (a more normal level). They are optimistic about relief in oleo inputs going into 2026.

•Because these raw materials are sourced from Asia and entail a long supply chain, the P&L benefit of these expected lower commodity prices will be delayed. The company anticipates working through high-cost inventory during H1 2026,. Margin recovery is expected from lower oleo prices in the second half of 26.

Some Macroeconomic points:

•Stepan expects that 2 interest rate cuts in 2026 will boost demand [let’s hope!]

•The company achieved mid-single-digit growth among Tier 2 and Tier 3 customers in 2025. They expect to capture further volume in this segment—particularly in sulfate-free personal care—as stretched middle-income consumers trade down.

•And finally, surprisingly (to me anyway), the subject of tarrifs came up last and with only two minutes to go. The company noted they would continue to leverage its diversified manufacturing footprint (US, Mexico, Europe, Asia) to optimize supply routes. A rather generic reply to a generic question and I’m not sure I could have done any better. There’ll be more to this topic no doubt.

Overall – It’s a good picture for Stepan in areas outside of the traditional core surfactants for cleaning business. Polyols, tier 2 & 3 accounts, Agrochemicals, Oilfield etc are all doing well but the mass market cleaning product sector which they do sell a lot into and has been the historic bedrock of the business is tough. Project Catalyst seems like an appropriate response for the near and long term. Capacity and facilities cost money when they are not fully utilized. We’ll be keeping a close eye on this as the year progresses.

I took a look at the stock price and, because the Q4 results missed analyst expectations, the stock took a roughly 11% hit on the day of the earnings release. Unfortunate as they’d been having a good run stock price-wise over the last couple of months.

I encourage you to read the full release here.

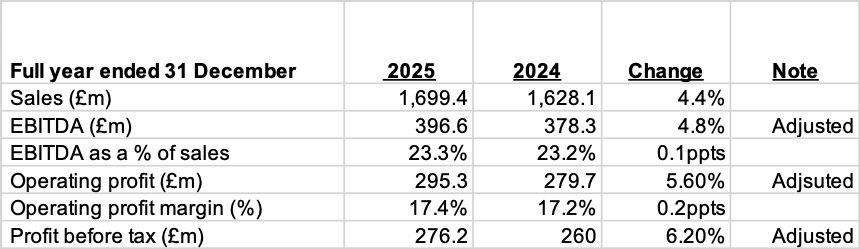

The day after the Stepan call, Croda (LON: CRDA) announced their results. They talk a lot about constant currency results, which just confuses things for me and I have taken that out of the box score below. But whichever way you look at it, the company had some good growth in a challenging market. Anyway here’s how they summarise it. [my comments are in these square brackets]

Group [that’s the whole company] sales +6.6% at constant currency [it still grew in regular currency – see below – at 4.4%] comprising:

•Consumer Care sales +8%

oBeauty Actives +6%, Beauty Care +4%, F&F +15%, Home Care +2%

•Life Sciences sales +8%

oPharma +4%, Crop Protection +14%, Seed Enhancement +8%

•Industrial Specialties sales (2)% [This is non-core these days. 20% of the sales are to Cargill to whom they sold a chunk of this business]

•Q425 sales +5%

Adjusted operating profit +7.9% at constant currency

•Adjusted operating margin 17.4% (2024: 17.2%); Consumer Care and Life Sciences margin improving

•Adjusted profit before tax +8.4% to £276.2m (2024: £260.0m); equivalent to £282.0m at constant currency

•IFRS operating profit of £110.1m (2024: £227.5m); adjustments included £107.3m impairment charges, £44.6m related to optimising lipids capacity, with an associated onerous contract provision of £15.9m

I can add the following: Volumes grew as well as £ in 2025. Their bridge chart showed a 2.2% volume increase effect on operating margins. [hope I’m reading that right].

Here’s the box score:

Like Stepan they are going after costs, although they don't have an uplifting name for the effort. It’s just called a transformation programme (yawn..). Anyway they promise £100 Million savings annually by 2028. Two thirds out of the supply chain and one third from simplifying the organization (ie headcount reduction mainly). As part of this programme (I really wish they’d come up with a clever name.. Project White Rose maybe – given their Yorkshire heritage? Project Pudding (Yorkshire pud) – nah that doesn't work). I noted a few things.

•Reduce SKU’s. There’s about 100,000 right now. (Wow that’s a lot, even for a specialty chemicals company) and increase minimum order quantities (it sounded like these were quite low today).

•Croda operates 40 sites worldwide (sounds like a lot and it probably is but they are a specialty chemical company). 11 are what they refer to as shared sites, meaning they service multiple Croda business units and in fact support 60% of sales and 70% of volumes (so the higher volume type products like ethoxylates and esters – I’m guessing).

o 8 of these shared sites are alkoxylation sites and they will consolidate these down to 4 by 2027.

o They don't seem to identify these 11 sites but I’m going to take a shot here (Croda people – the tipline is open!) Atlas Point, Rawcliffe Bridge, Chocques, Singapore, Thane, Shiga, Gouda [not sure about this as it may be Cargill now], Campinas, Mill Hall, Hull, Mevigal.

•They will close and outsource their UK distribution centre.

•5% headcount reduction already done in 2025. More to come

•Centralise procurement [interesting- it didn't sound like it was centralized at all]

•Reducing capex to a normal level of £108 Million/yr and no more (big) M&A (for a while).

•Pricing stuff

•AI etc..

Looking forward they see: 3 – 6 % organic sales grown and a Q1 of 2026 similar to Q1 of 2025 (which itself was a big quarter). They are targeting an operating margin of over 20% in 2028 (vs 17.4% today) and this will result in around a 25% EBITDA margin (awwright! Now that’s the Croda we know and love!). Growth will come from Consumer Care (3 – 6%), Life Science (4 – 7%) and Industrial Specialties (-3 to +3 % - ie flat)

Q&A was interesting. I learned that overall plant utilization was 93% in 2025. That’s pretty good, I think. They want to get to 100% which I didn't think was truly possible, but if there’s even a few points of juice to squeeze there that’s gotta be great for operating margin. They point to solid growth over the last 18 months including 10% volume growth in 25 vs 24 – which is really good. A lot of emphasis on innovation, direct selling (no distributors!) and customer co-development.

Overall not a bad start for the Croda recovery (started in 2025). The transformation programme (Project White Rose…) has similar elements to what Stepan is doing – including the 100 Million ($ vs £) and site rationalization. They also talked a lot about L&R( local and regional ) customers, which sounds a lot like Stepan’s tier 2 and 3 focus. Of course the Stepan and Croda businesses are radically different. Croda does not sulfonate and that is Stepan’s bedrock. Both alkoxylate. Croda has typically been more niche product and application focused, smaller volumes, more functional type ingredients etc. (Interestingly the word “surfactant” appeared once each in the 32 page Croda earnings release and 49 slide presentation and I did not hear it spoken at all during the call) Nonetheless it will be interesting to see how the two companies progress in the coming 2 – 3 years.

And finally, how did the almighty market react to what Croda had to say? At least one thumb up, I’d say.

Sasol also announced 6 month results ending December 30, 2025 recently. Not as much to chew on in there relating to surfactants but I teased out what I could. The surfactants business is part of International Chemicals. Last year, the company’s CEO indicated that segment / business “could” be for sale and they refer to it being a candidate for “future value unlock” in the materials. I think this is the right stance. Let’s see. Anyway – here is what they say about International Chemicals.

The segment is undergoing what they call a structural reset to mitigate softer global demand, global overcapacity, and elevated feedstock costs. [Ugh! sounds familiar] Despite a challenging macroeconomic environment, the segment achieved a 10% year-over-year increase in Adjusted EBITDA. The company has, however, revised its near-term guidance downward due to market pressures and an unplanned cracker outage, while maintaining its long-term FY28 profitability targets.

• Revenue & Profitability:

• Total segment turnover: R39.43 billion. (about $2.5 Bn)

• Adjusted EBITDA: R3.09 billion (US$178 million combined for America and Eurasia), representing a 10% YoY increase.

• Adjusted EBITDA margin: 8%.

• Operational:

• Sales Volumes: America total external sales volumes were 933kt (+15% YoY); Eurasia external sales volumes were 472kt (-5% YoY).

• Pricing Dynamics: Average International Chemicals sales basket price declined 3% YoY to USD 1,614/MT

• Capacity Utilization: The LIP JV ethylene cracker operated below nameplate capacity due to an unplanned outage in Q2 2026.

• A "value over volume" commercial strategy is being executed, particularly in Eurasia.

• CapEx: Decreased by 49% in America (reflecting the completion of East Cracker repair work) and decreased by 37% in Eurasia (reflecting proactive reductions and fewer turnarounds).

• Outlook Guidance:

• FY26 Full-Year Adjusted EBITDA: Revised downward to USD 375 - 450 million (previously USD 450 – 550 million

• FY26 Adjusted EBITDA Margin: Revised downward to 8% – 10% (previously 10% – 13%).

• FY28 Adjusted EBITDA Target: Maintained at USD 750 – 850 million

• Headwinds: Softer global demand, continued global overcapacity, higher feedstock costs, elevated European energy prices, lower US ethylene margins, soft demand in the European surfactants market, and [of course] tariff uncertainty.

• Tailwinds: The pace of market decline is slowing [let’s hope – again], selective end-markets are stabilizing, and industry rationalization is accelerating [This is undoubtedly true – don’t you agree?], offering cautious optimism for recovery

And finally, in this earnings edition, Dow Chemical. Again it’s tough to tease out surfactant information from the whole company. I think most of the surfactant related business is in the Industrial Intermediates and Infrastructure segment (confusingly abbreviated as II&I. So here’s what I learned about Dow’s II&I business from the release and earning call transcript (full disclosure, unlike with Stepan and Croda, I didn't actually listen to the whole call (or any of it) – I just skimmed the transcript and asked Google Gemini 3.1 Pro what it could pull out of it re the aforementioned II&I). In any case, I think most readers know, Dow’s been having a tough time overall. OK – Here we go; Dow’s II&I business. Dow (whole company) reported full-year 2025 net sales of $40.0 billion, an operating EBITDA of $3.3 billion, and a GAAP net loss of $2.4 billion. Within the Industrial Intermediates & Infrastructure (II&I) segment, the Industrial Solutions sector faces what they call top-line pressure from local price compression and lower ethylene oxide catalyst sales, partially offset by good seasonal demand for deicing fluids (two cheers for the bad weather!). To optimize asset footprint and counter margin compression, the company successfully commissioned new cost-advantaged alkoxylation capacity across North America and EMEAI in 2025. This capacity deployment is meant to capture higher-value downstream growth in the home care, pharma, and energy markets.

Revenue & Profitability:

• II&I Segment Q4 2025 Net Sales: $2,688 million (down 9% YoY; down 5% QoQ).

• II&I Segment FY 2025 Net Sales: $11,163 million (down from $11,869 million in 2024).

• II&I Segment Q4 2025 Operating EBITDA: $(36) million.

Operational

• II&I Segment Q4 Volume: Decreased 1% YoY and 2% QoQ.

• II&I Segment Q4 Local Price: Decreased 9% YoY and 3% QoQ.

• Sales decreases driven by lower local prices and lower ethylene oxide project-related catalyst sales, which were partially offset by seasonally higher demand for deicing fluids.

• Commissioned new cost-advantaged alkoxylation units in North America (NAA) and Europe, Middle East, Africa, and India (EMEAI).

• Shifted production capabilities to support higher-value downstream surfactant end-markets, explicitly targeting home care, pharma, and energy applications.

Outlook Guidance (whole company)

• Net sales expected to decline 2% to 4% QoQ.

• Cost reduction actions expected to yield a ~$10 million EBITDA.

• Higher demand for deicing fluids and typical seasonal improvements expected to generate a ~$5 million EBITDA, partially offset by lower spreads.

• Higher planned maintenance activity expected to create a ~$15 million EBITDA decrease.

• Headwinds: Continued local price compression, lower market spreads, and broader macroeconomic softness in associated industrial applications. Prolonged weak demand in building and construction end markets, which heavily pressures the aggregate II&I segment operating rates.

Who’s doing well at the end of the surfactant value chain? Ecolab for one. They reported decent results from their products and services in I&I cleaning, ie:

• Sales $4.2 billion, +5%. Organic sales +3%, led by accelerating growth in Food & Beverage, Pest Elimination and Life Sciences, and continued strong growth in Specialty and Global High-Tech. This accelerating performance more than offset a combined 2% headwind from basic industries, Paper and a short-term impact from lower distributor inventories in Institutional.

• Operating income margin 17.0%. Organic operating income margin increased 140 bps to 18.5%.

• Diluted EPS $1.98, +19%. Adjusted diluted EPS $2.08, +15%.

By the way, yes I know that P&G and Unilever released earnings in February also. This blog post is long enough already and I need to digest the information so I think we’ll cover these together in the March blog. Is that OK?

OK then. How are you feeling after all that? There’ll be more next month. I’d be interested to hear from folks out there in companies that don't publish annual reports, or whose reports bury the surfactant business under a bunch of other stuff. I know we joke about the tip-line here, but it is open (It’s not a phone line. You just email me!) and we keep everything confidential and as anonymous as you like. Many regulars use it.

And only a dime

As we went to press (I love saying that – although, as you know there is no actual “press”) last month, Clorox acquired Gojo. The great Beauty Independent (They are really great and I have no business connections with them.) wrote a great analysis of the deal here. The deal is worth $2.25 billion, valuing the Gojo at 2.4x sales and 11.9x EBITDA. The acquisition diversifies Clorox away from volatile retail markets by securing a big foothold in the professional channel, which generates 80% of Purell’s (Gojo’s big brand) $800 million in annual revenue. However, the transaction has drawn cautious investor reactions as it elevates Clorox’s leverage to 3.6x EBITDA and pauses share repurchases during a period of existing corporate performance challenges. Read the whole thing. It’s a good read.

An unsexy deal?

By the way, you probably heard. ACI has a new president and CEO this year, Jennifer Abril (formerly of SOCMA). Welcome Jennifer! The blog has always enjoyed the support of ACI. Also I note that the ACI has brought on a brace (that’s 8) of new team members and they are all so young. Great to see fresh energy and vibes in the industry!

Vantage dropped a bit of a bomb on the oleo supply chain. The company, on January 28, filed a petition for the imposition of Antidumping Duties and Countervailing Duties on Imports of Certain Fatty Acids from Indonesia and Malaysia. Wow OK, then. Clearly the company is keen to protect its core fatty acid from tallow (and imported palm, presumably, though I’m not sure how much of that there is) business. Here’s more information from the actual filing. And I quote:

“The merchandise subject to these Petitions is certain fatty acids (CFA), which are organic acids made of a hydrocarbon chain with a carboxylic acid group (i.e., an organic acid that contains a carboxyl group (-C(=O)-OH) attached to an R-group, sometimes also written as R-COOH, R-C(O)OH, or R-CO2H) at one end with a carbon chain length (i.e., the number of carbon atoms in the fatty acid chain) of C6, C8, ClO, C12, C14, C16, or C18, with an iodine value below 105 g/100 g and with a ratio of free fatty acids to triglycerides ( also known as the “degree of split” or “DoS”)) of at least 97 percent, including single fatty acid (also referred to as “pure cut”), and blends containing a combination of two or more carbon chain lengths.

CFA is also commonly called pure, pure cut, fractionated, or distilled fatty acid or mixed, mixed cut, or blended fatty acid, with the terms pure, pure cut, fractionated, and distilled typically referring to specific single-chain fatty acids that have been separated from a mixed natural source such as animal fat or vegetable oil using processes like hydrolysis (the breakdown of fat molecules by water, catalyzed by acid, base, or enzymes (lipases) to yield glycerol and free fatty acids), distillation, and crystallization, and the terms mixed or mixed cut referring to combinations, blends or mixtures of different single-chain fatty acids also derived from a natural source such as animal fat or vegetable oil using processes like hydrolysis, distillation, and crystallization. Common names for pure, pure cut, fractionated, or distilled fatty acids forms include stearic acid and oleic acid. Common names for mixed or mixed cut fatty acids include coconut fatty acid, hardened coconut fatty acid, topped coconut fatty acid, topped hardened coconut fatty acid, palm kernel fatty acid, hardened palm kernel fatty acid, topped palm kernel fatty acid, topped hardened palm kernel fatty acid, palm fatty acid, palm stearin fatty acid, palm”

It goes on. You can read more at a bunch of places which report these filings. I found a few things to be interesting. One is “Specifically excluded from the scope are CF A containing 90 percent or more, by weight, of fatty acids with carbon chain lengths of C6, C8, or C 10 ( or any combination thereof).” [not surprising right?]. They allege dumping margins of 20.8% to 72.03 % for Indonesia and 64.67% to 94.41% for Malaysia. The unfair subsidies are detailed in an appendix 3 here.

They list the offending producers and exporters in an Appendix 1 here. Many familiar names on there, I see.

They also list a veritable rogues gallery of US importers of the offending fatty acids in an Appendix 2 here. I personally know folks at many of these companies.

What does this all mean? The existing 16 – 19% (++) are not enough clearly.

I have to pause here while I hire an additional brace of operators for our tipline. OK there. So, if you are i) Vantage, ii) Listed on Appendix 1 or iii) Listed on Appendix 2. I’d be interested to hear from you. Thanks.

It’s open…

Someone at ACI asked me about macauba oil as a palm alternative. I must admit, I’d heard the name but not much else. Food Navigator magazine (my well thumbed copy) tells me that said oil, has a plant yield of approximately 2.5 metric tons of vegetable oil per hectare per year, and is comparable to that of conventional oil palms in its productivity, but it requires less water and is more resistant to drought. This means macauba palms can be cultivated for oil production in less fertile soils and on degraded pastureland in the drier regions of Brazil, eliminating the need to clear rainforest for its production. I’m not sure about the comparable claim as I’d always pegged modern palm plantations at 4 – 5 MT / hectare, although it does vary a bit down at the smallholder farms and such. Nevertheless there’s a fair bit of activity, particularly be the Fraunhofer Institute who has their own page on the idea here. BASF also has some products based on the oil, which I now recall we reported here a while back. UPDATE (from the tipline): Around the end of 2024, BASF signed a contract with INOCAS for the supply of macaúba oils. After the contract was signed, incompatibilities were identified, which ultimately led to the termination of the contract in April 2025. Nevertheless, macaúba remains a promising renewable feedstock for BASF. Hallstar and Cargill also are reportedly working on it. Is this the next frontier for palm-type oils? I don't know, but I thing its’ worth keeping an eye on. And of course – that tipline remains ever open.

I think we’ve had enough of these for now, don’t you?

One of our great readers – and they are all great – the greatest readers in the business, wrote in after reading about the Thyssen Krup / Novonesis (no need now for a pronunciation lesson if you read last month) enzymatic catalysis collaboration. He notes and I quote [redacting to remove names and such as is our custom]: “I performed an enzymatic fat splitting process with great success more than 15 years ago. At XXXXX in XXXXX we regularly split thousands of tons of rapeseed and sunflower oil with a dedicated lipase. Our splitting cost were slightly higher than hydrothermal splitting. The absolute game changer is the scalability. You just need an agitated tank and get splitting degrees of 98%. So you could turn your tank farm into a big fat splitting unit.v There is also another company in XXXXX performing enzymatic fat splitting. That worked so well that they shut down their splitting tower. This company has absolute low trans linseed oil fatty acid for food application. The problem is that most lipase are only active at higher pH values. But that leads to mayonnaise, due to the formation of soap. There are only on or two lipases on the market that also work a lower pH and have an excellent performance. But yes, it is a promising technology. So, stay very tightly tuned my dear readers. Where can you learn more first-hand knowledge of these developments. Jersey City. May. Here .

Quickie: Our good friends at Colonial Chemical announced a new distribution deal with Advanced Chemical Concepts (ACC), providing regional distribution coverage for HI&I Cleaning and Vehicle Care surfactants, as well as select Personal Care accounts in Michigan, Ohio, Illinois, Indiana, Kentucky, and West Virginia..

The great Craig Bettenhausen wrote a nice summary of some impressions from the ACI meeting here. It agrees with much of what I say in the video and here in the blog – so it’s a great read! Check it out.

I read in HAPPI that P&G has launched 3 new improved versions of the legendary Head & Shoulders Shampoo. Here. Two out the three, Smooth and Silky Shampoo and Hydrating Coconut Shampo, are built on a SLS / CAPB platform with, puzzlingly, a smidgeon of SLES just ahead of the preservative on the ingredient list (can someone explain this – some patent caused thing or what is it?). The third one, Sulfate Free Shea Butter Sampoo is built on lauramidopropyl betaine, sodium cocoyl isethionate and sodium lauroyl sarcosinate among other things. This got me thinking. I don't recall P&G being that big a user of isethionates. It was more of a Unilever thing. Turns out, however, isethionates and particularly the LAPB/SCI combo turn up in a few products, in addition to the new H&S including, Head & Shoulders BARE Pure Clean Anti-Dandruff Shampoo, Pantene Sulfate Free Shampoo with Rose Water, Pantene Infinite Lengths Sulfate-Free Biotin and Collagen Shampoo [fantastic name!], a couple of Aussie and Herbal Essences shampoos and a few Olay syndet bars. Also some acquired brands like Ouai, Native and Tula use them. Do they buy the SCI or make it in house? I’m guessing buy but I don't know. Let me know if you do.

Infinite Length - courtesy of SCI

The great CEFIC and Roland Berger published a study on the state of the European Chemical Industry. You can get it on the Roland Berger website. We bemoan Europe here regularly but it’s worse than I thought. Here are some key points:

•Between 2022 and 2025YTD, announced closures in the European chemical industry increased sixfold from 2.9 Mt to 17.2 Mt per year, and doubled between 2024-25YTD, totaling 37 Mt in 2022-25YTD and representing ~9% of the European chemical production capacity

•These capacity closure announcements have been made mainly within upstream petrochemicals (17.8 Mt, 48%), followed by basic inorganics (11.7 Mt, 32%), polymers (5.4 Mt, 15%), and specialty chemicals (2.0 Mt, 5%) – Number of announcements is more evenly split between segments

•Within petrochemicals, ~50% of the total announced capacity closures concern nine steam crackers which corresponds to a 16% net reduction in European steam cracking capacity, all located in integrated chemical clusters, putting these clusters under increasing pressure

•Closure announcements span across Europe, with the largest shares in key chemical industry countries including Germany (8.8 Mt, 25%), the Netherlands (7.2 Mt, 20%), UK (4.5 Mt, 12%), France (3.9 Mt, 10%), Italy (2.5 Mt, 7%), Belgium (2.3 Mt, 6%), Spain (1.6 Mt, 4%) and the rest of Europe (6.0 Mt, 16%)

•Across these countries, ~20,000 direct jobs are cited to be affected

•In 49% of the cases, companies indicate energy cost competitiveness as the primary rationale for closing, followed by demand-related considerations (19%), overcapacity (9%), and regulatory factors (8%)

Mckinsey also published a chemicals study. Here’s a snippet “ Meanwhile, Europe’s chemical producers face a prolonged slowdown driven by energy cost disadvantages and weak industrial output. Many specialty chemicals are showing signs of commoditization as technologies diffuse and differentiation narrows.”

At more or less the same time, INEOS had their debt downgraded by S&P. Hardly surprising.

My comment: This surely is a strategic matter. You need chemicals to live and defend yourself. Where will Europe get theirs from? The US? Middle East? China? Sad.

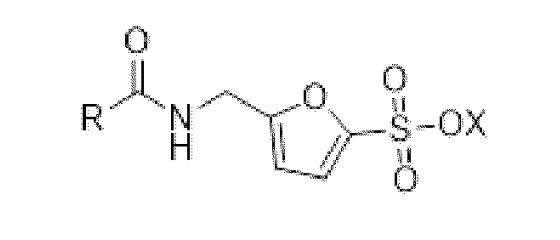

New surfactant alert. Unilever patent WO2026002784 was recently published which claims A furan-based anionic sulphate free surfactant comprising: a) a head group comprising i) a furan ring ii) a sulphonate group attached to the furan ring b) an amide containing linker group; and c) a hy- S-OX drophobic alkyl tail group having a carbon chain length of 8 to 18. It looks like this.

So what do you think? I dunno about that amide linkage. I guess it’s needed. But furan products should be cheap right – from corn, sugar beet and wood waste and such?

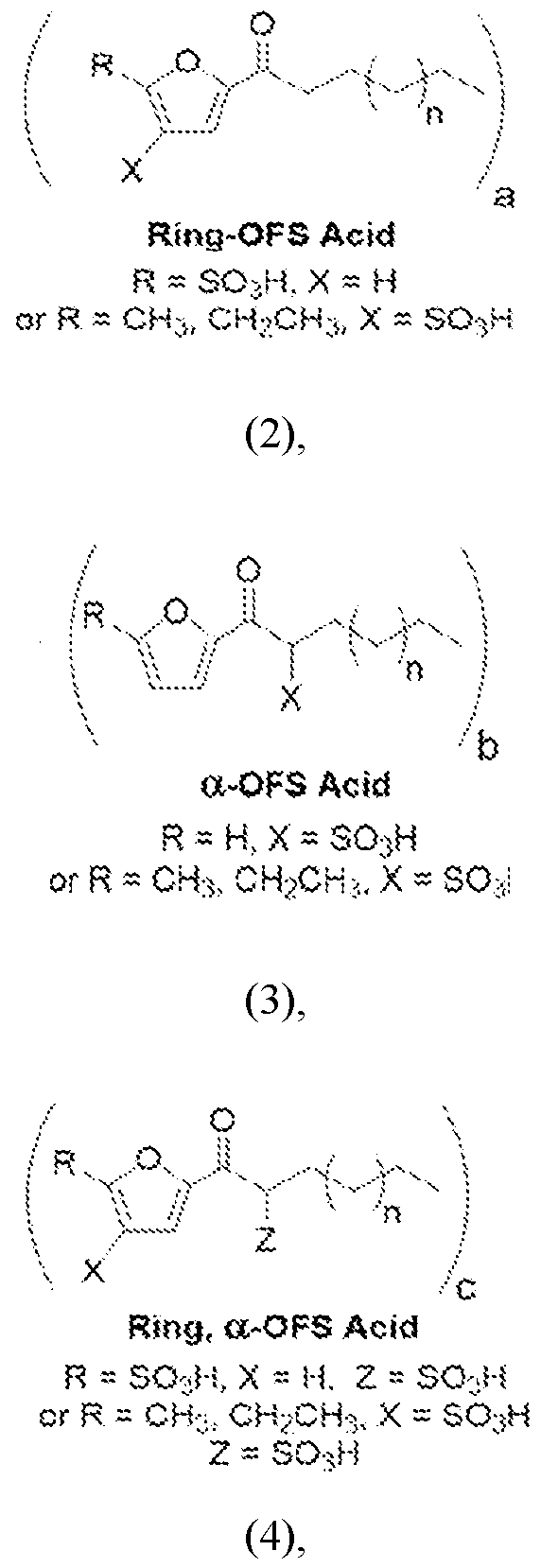

Another new surfactant: And you may be reading this here first: Speaking of Furan based surfactants: (That’s 3 colons in a row. You don’t get that in ChemicalWeek!). Sironix has launched a new anionic range based on Furan - called Furasoft. They say (quoting) “The Furasoft™ line uses proven furan structures for the first time in personal care applications, delivering unmatched performance and sustainability compared to conventional petrochemical surfactants. Both ingredients are engineered to integrate seamlessly into a wide range of personal care formulations, including shampoos, body washes and hand soaps.” You can read more here. The press release also say (and this is interesting) that Sironix has “demonstrated its production process at half-ton scale. Most recently, the company successfully completed a demonstration for its Furasoft™ -LFS product at Pressure Chemical and an established, commercial sulfonator, achieving a major milestone by using one of the incdustry’s most widely recognized and scalable surfactant manufacturing processes.” I think we know what that means and that is encouraging. I looked for an INCI Name(s) and could find any on their site. I’ve asked the company. (BTW - I’ve noticed this trend where folks are launching products into PC and being coy about INCI names. Anyway, let’s see.). I’ll come right out and say I kinda like the tradename. “Fura” connotes the supply chain and “soft” is a real old-school callback to so-called soft acids, the name given to linear alkylbenzene sulfonic acids which are biodegradable, unlike their predecessor branched alkylbenzene sulfonic acids. So you will see tradenames like Biosoft and Calsoft from Stepan and Pilot for their LAS. Very cool. I also like that the name is kind of reminiscent of a character from a Mad Max movie (Google it - played by Charlize Theron). Anyway coming back to a name or structure, I will put it here if / when I get it. In the meantime, there are some Sironix patents out there that may provide some clues, particularly this one. The patent discloses some ring and not-ring (and mixed) sulfonated oleofuran structures, like the ones in the figure below. Overall this is a great development for the industry. A solid alternative to the wide range glycolipid efforts out there. I am rooting for Sironix.

Straight outta Sironix Patent

As of Feb 17th, P&G’s Tide EVO is finally available nationwide. I’ve written about it enough here and even made a video about it, which has somehow ended up with 3,400 views. Go get some and let me know what you think.

I’m warming to Syensqo (the name that is. I’ve always quite liked the various iterations of the company). They recently launched a bio mass balance product Rhodasurf B7 UP. It’s BMB laureth 7. The march of BMB continues.

I’ve written glowingly about Integrity Biochem here and I’m biased as I’m an advisor to their board. I can tell though, their concept and supply chain is unique and incredibly powerful. This is a profitable company killing it with new technology in the oilfield and mining and now in Agrochemicals and HI&I and PC. When people ask me who are the real commercial breakthroughs so far in the new biobased field, I say Evonik in fermented biosurfactants and Integrity in biobased surfactants. Here’s a blog post about their activities in Ag.

Dioxane – can’t get away from it right? Well you almost can now. If you want to get below 1ppm (one part per million) in the surfactant (100% active. In the actual surfactant!), talk to the great Italian engineering innovators, Ballestra. New tech profiled here.

The very active and growth oriented Rossari of India continues to make waves globally. As I read in Chemical Weekly: Rossari Biotech Ltd, has signed a non-binding Memorandum of Understanding (MoU) with Saudi Arabia’s Sadara Chemical Company to explore the possibility of supplying key raw materials for the Rossari’s proposed speciality chemicals plant in Saudi Arabia. Earlier in March last year, Rossari had inked an MoU with Rabigh Refining & Petrochemical Company (Petro Rabigh), a joint venture between Saudi oil giant Aramco and Japan’s Sumitomo Chemical, for the development of propoxylates and ethoxylates manufacturing in Rabigh, Saudi Arabia. As per the deal, Rossari would source the ethylene oxide and propylene oxide from Petro Rabigh to manufacture the ethoxylates. Nice.

Another super-active Indian company, Galaxy Surfactants just announced more news re Mexico where they have partnered with the distributor Disan, to serve that market. There’s a lot happening.

And another Indian company (who I actually do not know that well) Khurana Specialities Limited has announced contracts for a new alkoxylation plant in India, based on Ballestra’s leading Enhanced Loop Technology. Very cool.

OK that’s it for the news. Just some market news then music to complete perhaps the longest blog in blog history. You’re welcome.

Market News

Asia's fatty alcohol ethoxylates (FAE) market is under upward price pressure, driven by escalating feedstock fatty alcohol mid-cuts C12-14 costs, which have risen since early January. FAE spot offers for March shipments are higher, compounded by limited spot availability due to a regional plant shutdown for maintenance. Despite the return of Chinese players from holidays, demand remains tepid, and trades are sluggish in Southeast Asia due to Ramadan. The Indian market shows higher demand for FAE imports, but cheaper Chinese material may create competition. Looking ahead, FAE spot offers are expected to remain firm on costs, with demand picking up as inventories are replenished, and China-origin material posing competition in India. Upstream, palm kernel oil costs fluctuate, with strong demand in Indonesia. China's ethylene oxide domestic prices are edging lower, with ample supply meeting subdued demand, though rising upstream ethylene prices may provide price support.

Global fatty alcohol markets exhibit mixed trends. In Asia, mid-cut prices are rising due to strong demand and higher feedstock PKO costs, with limited spot availability from upcoming plant turnarounds, and an increase in demand is expected ahead of the Lunar New Year. Long chain prices, however, are generally softer. The US market faces sufficient Q1 supplies meeting weak demand, leading to downward price pressure and discouraged imports, despite firm lauric oil costs and competitive petrochemical alcohols. European Q1 contract prices have fallen substantially, driven by softer feedstock costs and ample supply, resulting in stable to soft spot prices amid sluggish demand. Noteworthy developments include the postponement and simplification of the EU Deforestation Regulation and a new trade deal between Indonesia and the EU which could boost trade through tariff elimination.

The Asian linear alkyl benzene (LAB) market is stable after the Lunar New Year holidays, with suppliers holding firm on offers despite non-committal buyers. India's LAB market is sustained by tight availability due to ongoing plant maintenance, which could ease by March. The downstream LAB sulphonate (LAS) market in Asia is firm, with suppliers favoring export destinations for higher netbacks. Suppliers anticipate firmer demand from March as buyers prepare for the manufacturing season. Upstream, spot benzene prices in South Korea are edging higher, supported by firmer feedstock, but overall market momentum is constrained by holiday-reduced trading. Jet kerosene prices are higher due to US-Iran tensions. Sulphur prices are softening globally, reflecting weaker demand, while Chinese soda ash producers face a downbeat outlook due to anticipated inventory overhang and stable demand. Production updates include ongoing plant maintenance in India and Egypt, with an Egyptian LAB plant scheduled for an early April shutdown.

Music Section

I had a pretty decent game of golf in the freezing cold at ACI in Orlando. Thanks so much to P&G as always. And thanks to Billie Gilbert for everything she has done for us at ACI and beyond. She will be missed.

Our foursome that day included someone with a good solid musical taste. She pointed me toward the American blues / psych / heavy / stoner rock band, All Them Witches, which I have had on the blog here but not that much. So let’s dig into the catalog shall we?

Here’s the most recent release, Red Rocking Chair. Bluesy opening, following by an Iommic riff which will make you smile (if that’s your thing). Yes, and that’s a violin.

Here’s an old one. Understand now why they call themselves an American rock band.

Real hippies are cowboys – did you know that?

And the delightfully named “Hush I’m on TV”

Super-bluesy – The Marriage of Coyote Woman.

Followed inevitably by the The Children of Coyote Woman

And, sadly, by The Death of Coyote Woman. That intro, I feel like I should use at one of my talks.