Surfactants Monthly - April 2026

Huge month. I sent out six newsletters to blog subscribers. Subscriber means you are on the email list to get reminders that each month’s blog is published. You don't have to pay! Anyway, the theme was War! -focusing on the impact on surfactants of the whole kerfuffle with Iran. I also made a YouTube video. Here’s that:

If you haven’t read the newsletters, I’m going to put here below, some of the key charts and graphs. You will soon get the picture of what is going on. Here we go:

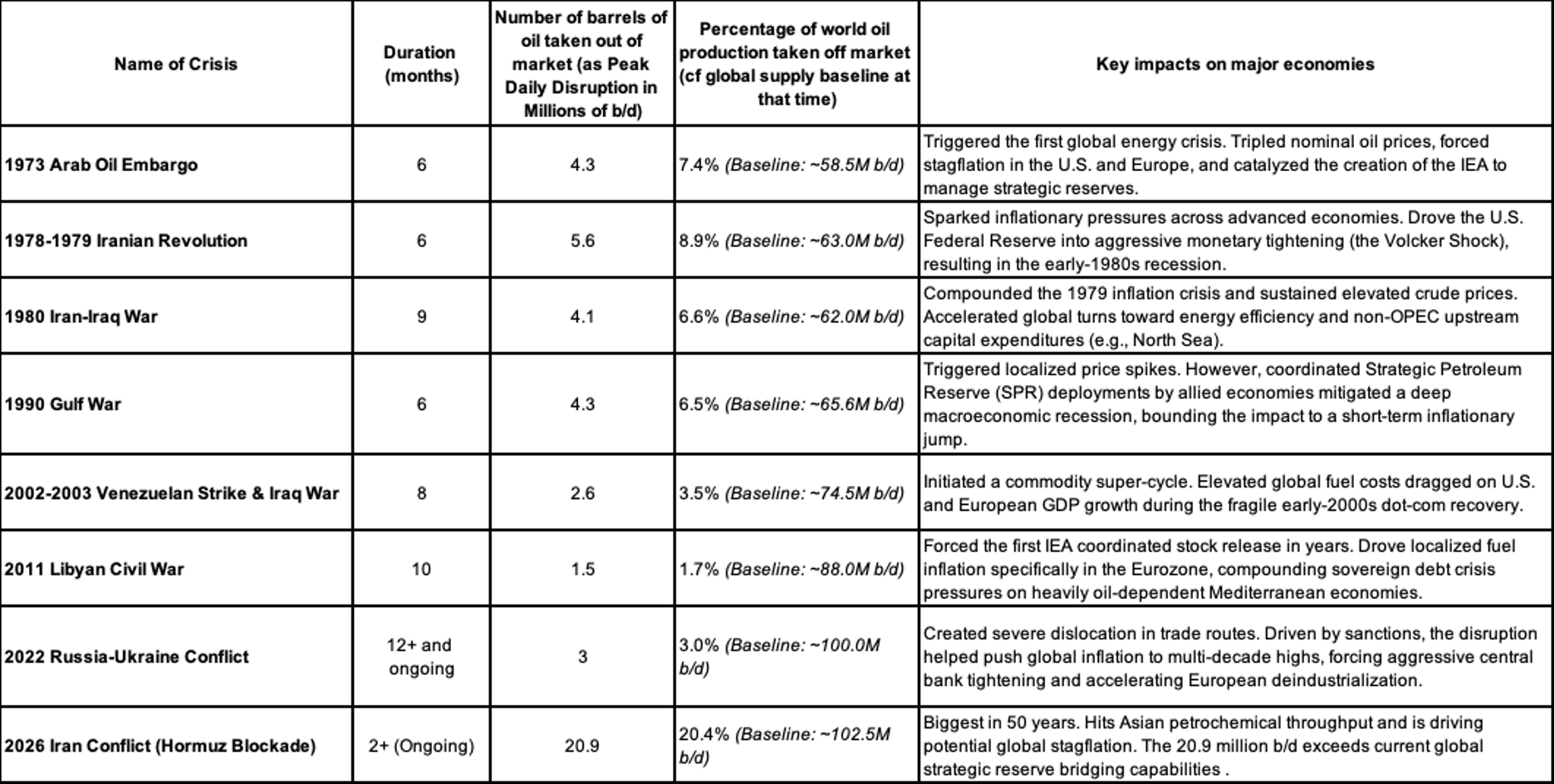

Biggest Oil Outage Ever as % of Global Production

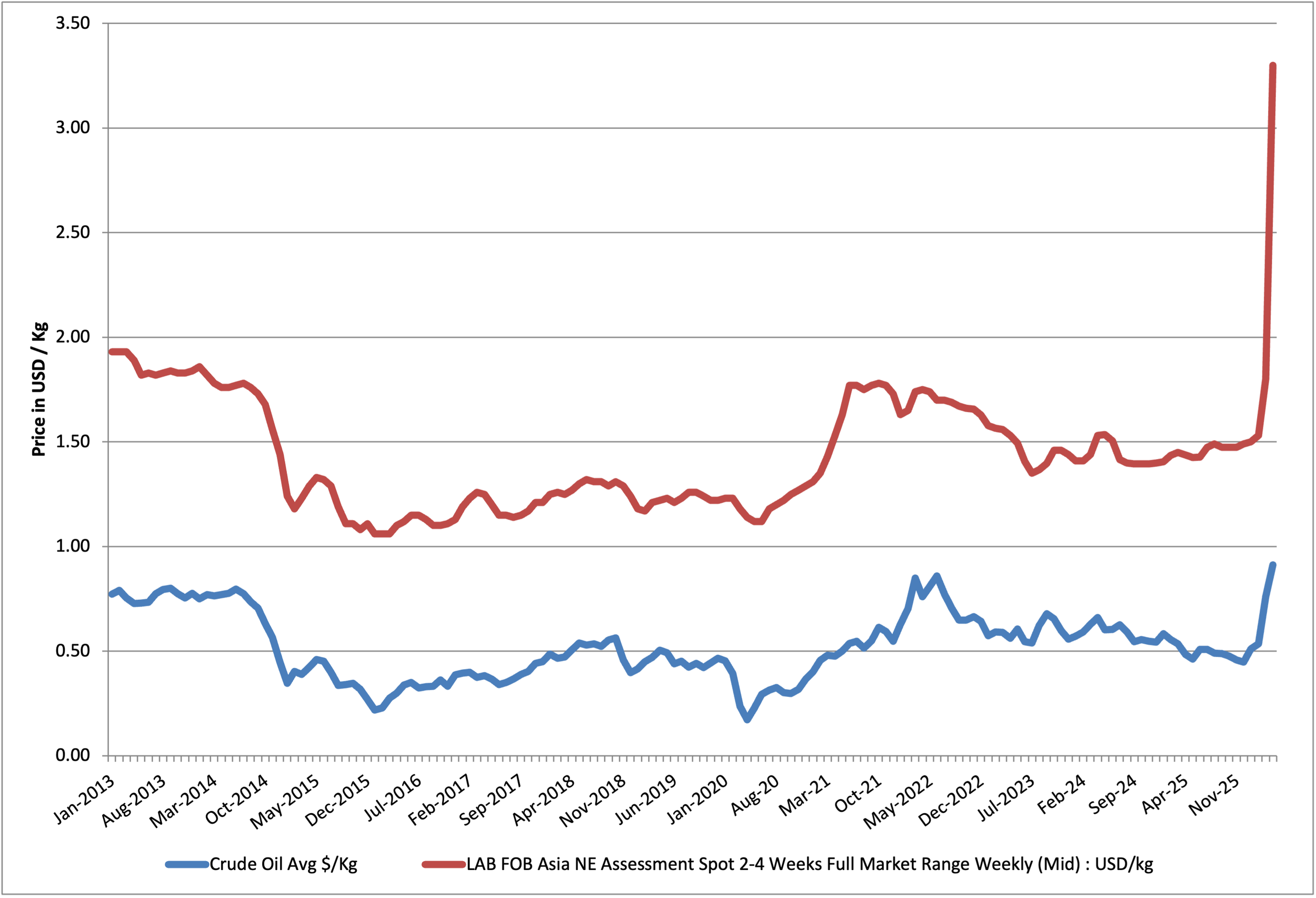

LAB to the Moon (source ICIS, FOB NEA)

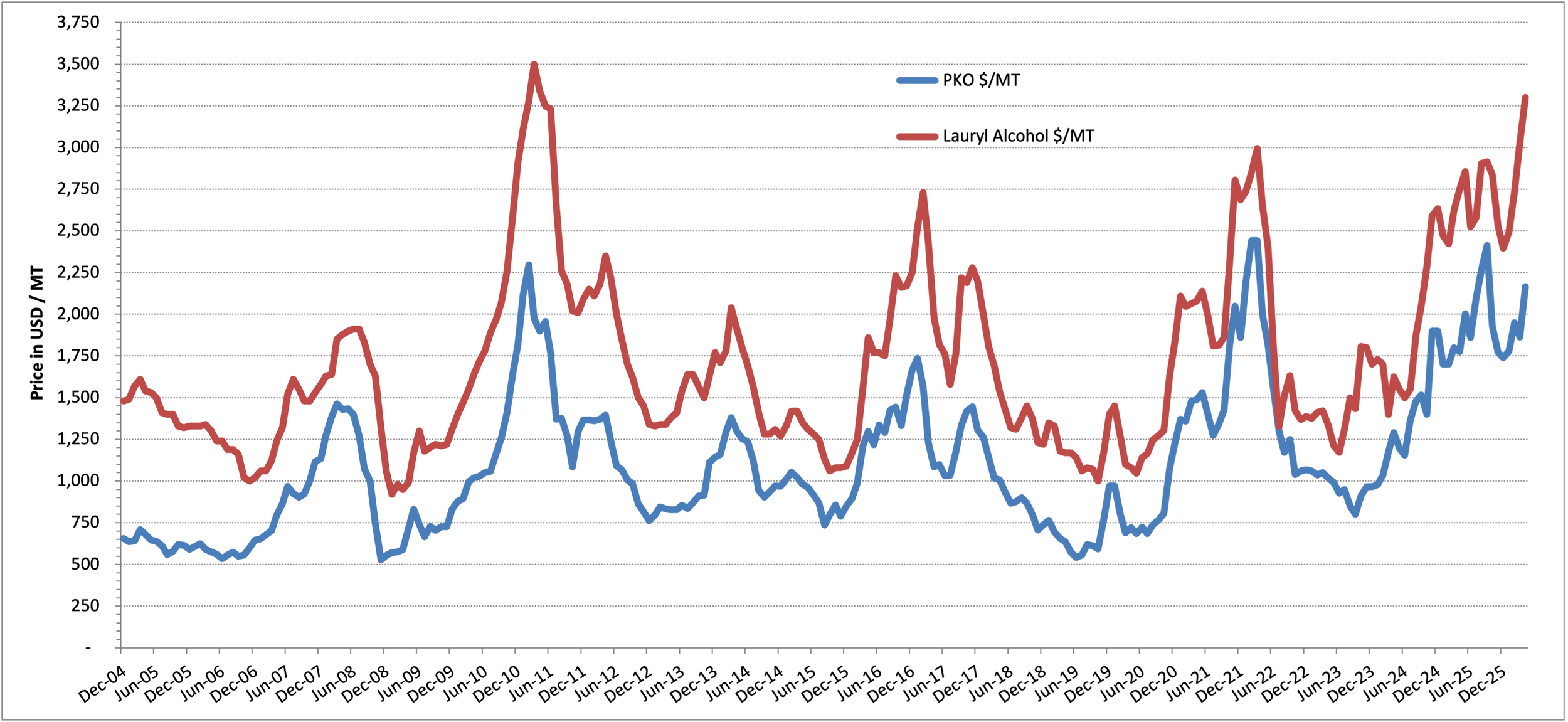

Palm not going to save us

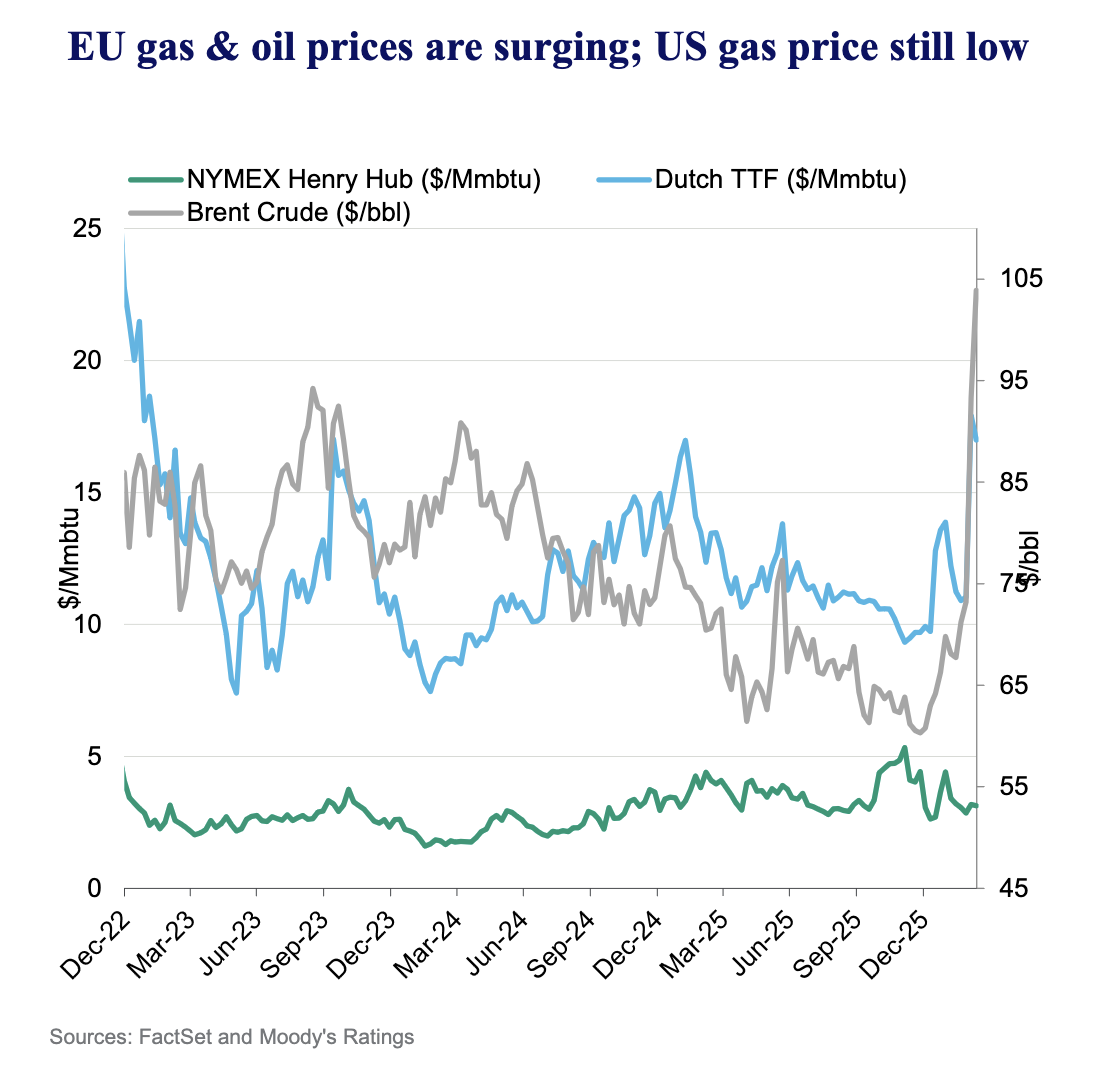

Yeah but…’merica!!

and ‘merica again !

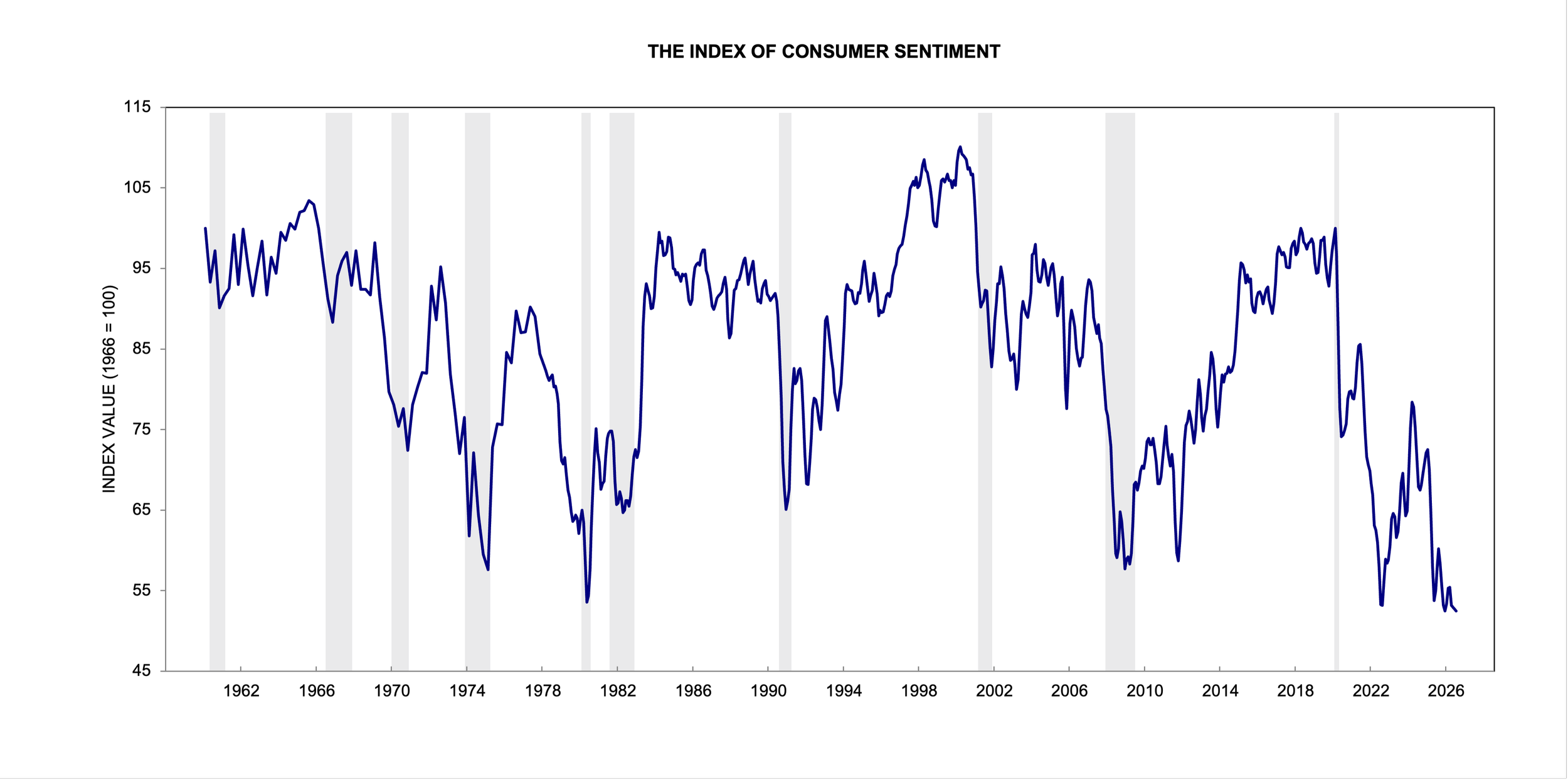

Oh.. but American Consumers ….

Head spinning yet? Well, join me this week in Jersey City as we get deep into the effects of the war on our business with a special morning session called Conflict and Consequence. Still time to register. We start on Wednesday morning, May 6th at 8.30AM

News from the Food Supply Chain:

I’m going to be brief for this blog because, honestly, I am short of time. I just got back from speaking at the Council for Producers and Distributors of Agrotechnology (CPDA) meeting in Austin, TX and I have to finalize my talk for World Surfactants. I’ll no doubt be updating it until the morning of as there is so much happening.

So what about the CPDA?. Here are my impressions.

They love surfactants. The package which goes in the tank along with herbicide and pesticide etc. is called the adjuvant mix. Many surfactant companies were involved in the meeting, e.g. Indovinya, Stepan, Croda, Integrity Bio, Syensqo etc. It’s a hot market compared with consumer products these days.

Having said that – farmers themselves are hurting. Costs are going up (no kidding – fertilizer, fuel etc) and prices down in the main.

Biopesticides (they call them biologicals also) are a hot topic. They’re still a small part of the market – best estimate I could get was about maybe 5 – 10% but lot of work going on and overall growth fo 8-9% per year. The use of these, some of which are live microbes is driving interest in new adjuvant surfactants, such as those Integrity is selling there under the Verosurf name (Cool name – Truth in Surfactants?!)

Brazil is a biopesticide hotspot with 60% of soy crops in Brazil using it.

The ESA (endangered species act) is driving interest in DRAs (Drift Reduction Adjuvants). The big actives makers (Bayer, Syngenta, Corteva, BASF) are very keen to see drift reduced. It’s all about droplet size and modelling in Wind-tunnels and drones and such. Apparently there are only 2 approved windtunnels for this work in the US - Battelle Institute and the University of Nebraska.

The soil microbiome is becoming a big deal. Making sure surfactants friendly to that is important.

Apparently adjuvants always used to be about spreading, wetting and surface tension. Now it’s those three plus osmotic pressure, water retention in soil and shelf life. Interesting right?

The industry doesn't like MAHA. They view the movement as anti-farmer and, frankly, anti-American. Glyphosate was called the “ball bearings” of the food supply – meaning absolutely essential.

I was struck overall by the level of tech and data intensiveness of many small family farming oprations. Lots of innovation going on with formulations and application methods, particularly drones.

If you are not in this field, take a look. If you’re not part of CPDA, you should be. By the way one of their board members will be speaking at our event in Jersey City.

The Other News:

Sick of Clean Beauty yet? Not so fast. It is still a thing and it’s worth studying. Barbara Olioso wrote a good article (https://www.ulprospector.com/knowledge/21246/pcc-who-defines-clean-beauty-now-how-retailers-and-coalitions-are-setting-the-new-standard/ ) on the UL site recently. In summary: The regulation of cosmetics marketed as clean is managed through frameworks established by retailers and industry coalitions rather than centralized legislation. Retailers including Credo Beauty, Whole Foods Market, Sephora (owned by LVMH), and Ulta Beauty enforce formulation standards by restricting specific materials; Credo excludes 2,700 ingredients, Whole Foods excludes 240, and Sephora excludes 50. Upstream chemical hazard characterization is also coordinated by the Know Better, Do Better (KBDB) Collaborative, a group comprising ChemForward, Beautycounter, The Honest Company, Dow, Inolex, and the Environmental Defense Fund. To secure distribution through these channels, cosmetic formulators must comply with these retailer-specific ingredient exclusion lists, sustainability metrics, and supply chain certification requirements.

It frequently impresses me the amount of innovation in the laundry sector. Henkel’s Purex (I read in HAPPI) has introduced new concentrated liquid detergents. I went over to the Purex site to see what they are built on: SLES, LAS, Laureth-12 and Sodium Cocoate. Nothing too fancy, although that L-12 caught my eye. I thought it was more of a creams and lotions type ingredient. Apparently Purex uses it but I couldn't find it in any other big brands. Thoughts?

Evonik continues to be the commercial leader in glycolipids. Why do I say that? They continue to be the only company of which I am aware that has a plant with tens of thousands of MT/yr capacity and an address where I can go look at it. If someone else in glycolipids has both those things, please let me know. Anyway, they won an award at IN-Cosmetics for their Rheance SOFT GO, which (It says here) is a “skin barrier-strengthening, sustainable cleansing agent” What’s in there? Glycolipids, Glyceryl Oleate and Glycerin. Nice eh?

Unilever’s Seventh Generation makes dish detergent. It’s been a while since I looked at their product ingredients. So let’s take a look what’s in there ! I went over the Target site and the ingredient listing is easily accessible. It’s (I quote): water, sodium lauryl sulfate (plant-derived cleaning agent), lauramine oxide (plant-based cleaning agent), glycerin (plant-derived foam stabilizer), decyl glucoside (plant-derived cleaning agent), magnesium chloride (mineral-based viscosity modifier), citric acid (plant-derived ph adjuster), tetrasodium glutamate diacetate (synthetic processing aid), sodium citrate (plant-derived processing aid), benzisothiazolinone (synthetic preservative), methylisothiazolinone (synthetic preservative), plant-derived fragrances: canarium luzonicum (elemi) gum nonvolatiles, citrus aurantium bergamia (bergamot) fruit oil, citrus aurantium dulcis (orange) peel oil, citrus nobilis (mandarin orange) peel oil, cymbopogon citratus (lemongrass) leaf oil, tangelo oil. What do you think?

I guess the mainstream alternative is Dawn in the US and that contains Water, Sodium Lauryl Sulfate, C10-16 Alkyldimethylamine Oxide, Alcohol Denat., Deceth-8, C9-11 Pareth-8, Sodium Chloride, PPG-26, PEI-14 PEG-24/PPG-16 Copolymer, Fragrances, Phenoxyethanol, Methylisothiazolinone, Acid Blue 9. So some alcohol ethoxylate and polymers that 7th Gen doesn't like.

Comes down to preference and performance - Image by Grok

Another thing out of IN-Cos was that Wacker and Amyris (remember them?) have a partnership. It doesn't say about what, but my guess is it has something to do with finding a good alternative emollient to silicones (where Wacker is strong). Still a hole in that market. Amyris seems to be in a sort of partnership business model mode now (don't dare call it contract research!), using their synthetic bio. Good luck to both!

BASF news: (https://www.basf.com/hk/en/media/news-releases/asia-pacific/2026/03/apac-26-25) BASF Hannong Chemicals Solutions Ltd. (BHCS), the joint venture between BASF and Hannong Chemicals, announced the inauguration of its new non-ionic surfactant (NIS) site located in the Daesan Industrial Complex in Seosan, Chungcheongnam-do, Korea. Built on a site of approximately 12,234 m², the site is operated by BHCS, the joint venture established with a shareholding structure of 51% BASF and 49% Hannong Chemicals, and began trial operations in January 2026. No mention of capacity.

Bio-Mass Balance continues to grow, despite the additional cost. Shell and Syensqo note that they are working together on mass-balanced ethylene oxide (EO) solutions to agricultural and industrial markets. Verified under the ISCC – the International Sustainability and Carbon Certification Carbon Footprint Certification (CFC), these EO-based solutions are made with Shell Chemicals’ lower-carbon feedstocks, enabled through the use of carbon capture utilisation (CCU) credits via a mass-balance approach. I think this is a good arrow in the quiver for PCF reduction.

Tired of AI Slop yet? Lab Muffin Beauty Science is a Youtube channel run by Michele Wong, an Australian Chemist. This video, while pertaining to cosmetic formulation is generally relevant. Do you do any of these things? It is a great investment of 30 minutes, this video.

More palm news out of Indonesia (not sure it’s good). Indonesia has confirmed that the B50 mandatory biodiesel program will take effect on July 1, 2026. Agriculture Minister Andi Amran Sulaiman announced this initiative, which will raise the palm oil-based biodiesel blend in subsidized, low-grade diesel (known locally as Solar) from 40% to 50%.

Key points of the B50 Implementation:

•Effective Date: July 1, 2026.

•Purpose: To bolster national energy self-sufficiency, reduce foreign exchange spending on fuel imports (estimated savings of US$9.18 billion), and utilize abundant palm oil resources.

•Import Cessation: Indonesia will officially cease importing diesel fuel starting July 1, 2026, coinciding with the launch of the B50 program.

•Impact on Subsidies: The policy is expected to reduce fossil fuel consumption by up to 4 million kiloliters and provide subsidies savings of roughly Rp 48 trillion (approx. US$2.8 billion) in its first six months.

•Trial Progress: The Ministry of Energy and Mineral Resources indicated that B50 trials, covering vehicles, trains, ships, and heavy machinery, have shown positive results.

•Industry Response: The Indonesian Palm Oil Association (GAPKI) stated that while raw material is sufficient, the shift may reduce crude palm oil (CPO) exports by approximately 3 million tons annually, suggesting a need to increase production to maintain both domestic supply and export volumes

OK what else? Here’s something interesting. Eastman has introduced a new foam booster for sulfate free shampoos. It’s called Kalidex, a certified, readily biodegradable foam booster and thickener developed for sulfate-free personal care formulations. The company spotlights that the ingredient allows formulators to reduce total surfactant levels while maintaining performance in shampoos, body washes, and facial cleansers. The company claims that testing shows a 30– 45% average increase in foam height and, beyond lather performance, Kalidex also functions as a viscosity modifier. This gives formulators a single ingredient to address multiple formulation challenges in sulfate-free cleansing systems. Seems interesting right? I couldn't find an INCI name. What’s with companies launching new PC ingredients and being coy about the INCI name. BTW, Gemini doesn't know, Grok thinks something cellulose related and ChatGPT basically guesses everything and by the time I was done, I had no idea where we were. Perhaps someone would like to use the tip line?

You know what to do - Image by Grok

The Laundress sold their company to Unilever and then had a kind fo feud with them. THe Founder has started a new laundry company called Lindry. High end expensive detergent. Here’s the formula for one of them- A lot of APG (which is actually quite cheap these days) and a sultaine. Could work…? Water, Lauryl Glucoside (plant surfactant), Decyl Glucoside (plant surfactant), Coco Glucoside (plant surfactant), Cocamidopropyl Hydroxysultaine (plant surfactant), Glycerin, Fragrance, Benzisothiazolinone, Citric Acid, Sodium Hydroxide

Conrad Plimpton, who acquired Inolex in and 1981 chaired the board until 2013 passed away on April 19th. RIP. He made a huge impact on our industry.

More fascinating Biosurfactant news: biosurfactant developer AmphiStar has launched AmphiNova®, a proprietary platform of more than 80 biosurfactant molecules. The company says (and I partially quote and paraphrase from the PR) that the platform expands the range of sustainable, high-performance surfactants available to the market and enables further development and optimisation of new molecules. These new molecules combine strong functional performance with a sustainable production approach. Each molecule is selected and optimised for specific properties, combining core surfactant functionality with additional performance benefits depending on the application.

AmphiStar is employing a dual approach to bring AmphiNova to market. Firstly, the company is building a pipeline of partners across relevant industries, establishing Joint Development Agreements (JDAs) on specific AmphiNova molecules to support market entry with strong technical and commercial alignment. These partnerships enable targeted and strategic co-development. JDAs are reserved for specific markets and regions where deep collaboration makes strategic sense. In parallel, AmphiStar will launch selected AmphiNova molecules directly to market in the coming year. These new commercial grades will expand AmphiStar’s portfolio of personal and home care biosurfactants beyond its current four products, AmphiCare® A & L and AmphiClean® A & L, which were launched in October 2024. They represent the first in a series of additional biosurfactants to be

introduced through the platform. A life cycle assessment completed in March 2025 highlighted the sustainability profile of AmphiStar’s biosurfactants compared to conventional alternatives, including a four-fold reduction in CO2 emissions, an 18-fold reduction in water deprivation, a 5.5-fold lower impact on human health and a 15-fold lower overall environmental impact.

If anyone else is doing this, please get in touch and give me the details.

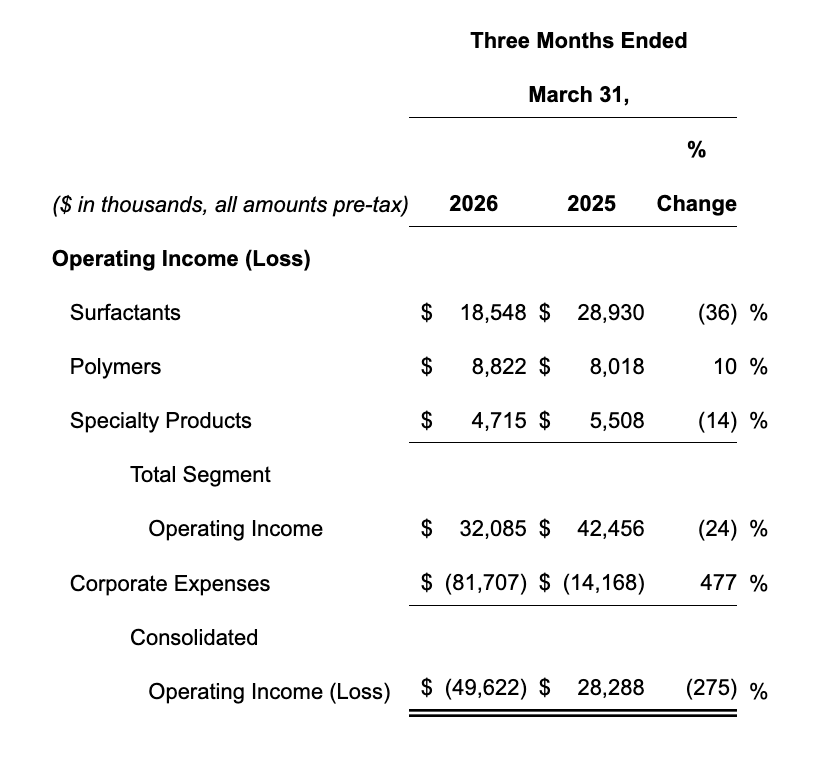

Stepan reported a very tough first quarter for 2026 and this is not surprising given market conditions established already plus the effects of one month of the Iran war. Here are some of the key points. :

Company as a whole:

Reported net income was a $41.4 million loss versus $19.7 million of income in the prior year. The current year loss resulted from a previously announced $65.4 million pre-tax restructuring charge. Adjusted net income was $10.3 million, down 47% versus the prior year, largely due to lower Surfactant earnings and higher interest expense. The higher interest expense reflects lower capitalized interest income due to the start-up of the Pasadena, TX site.

EBITDA was a negative $16.5 million versus $58.0 million in the prior year. Current year EBITDA was negatively impacted by the $65.4 million restructuring charge. Adjusted EBITDA was $49.6 million, down 14% year-over-year.

Organic sales volume was flat year-over-year as strong demand within Crop Productivity, Oilfield and Industrial Cleaning was offset by soft European Polymers demand.

In Surfactants:

Surfactant net sales were $453.7 million for the quarter, up 5% versus the prior year. Selling prices were up 2% primarily due to pass through of higher raw material costs, improved product and customer mix, along with pricing actions. Organic sales volume was up 2%, driven by strong demand within the Industrial Cleaning, Oilfield and Crop Productivity end markets. Total sales volume declined 2% due to the Philippines divestiture in the fourth quarter of 2025. The Company achieved volume growth in all global regions except Asia. Foreign currency translation positively impacted net sales by 5%. Surfactant adjusted EBITDA(2) for the quarter decreased $7.2 million, or 15%, versus the prior year. This decrease was primarily due to higher overhead due to production timing differences in Asia, competitive pressures in Mexico, the severe cold snap in the U.S. and higher oleochemicals raw material costs.

Here are the segment operating income results

On the earnings call, Luis Rojo, CEO said that the company is seeing raw material price inflation because of the US-Iran war (no surprise there!). And, raw material availability continues to be a challenge as the war has affected supply chains. The company will continue to pass on higher raw material costs through price increases, and it has been “very successful” in doing so in most of its businesses.

He also said that “the consumer is still resilient, the consumer is still spending” and Stepan has not seen declining consumer demand. In some markets, consumers were trading down from branded to private-label products, but this was not a “radical” move that hurt Stepan’s businesses, he said. [I wish I was that optimistic. Time will tell, I guess.]

Market News:

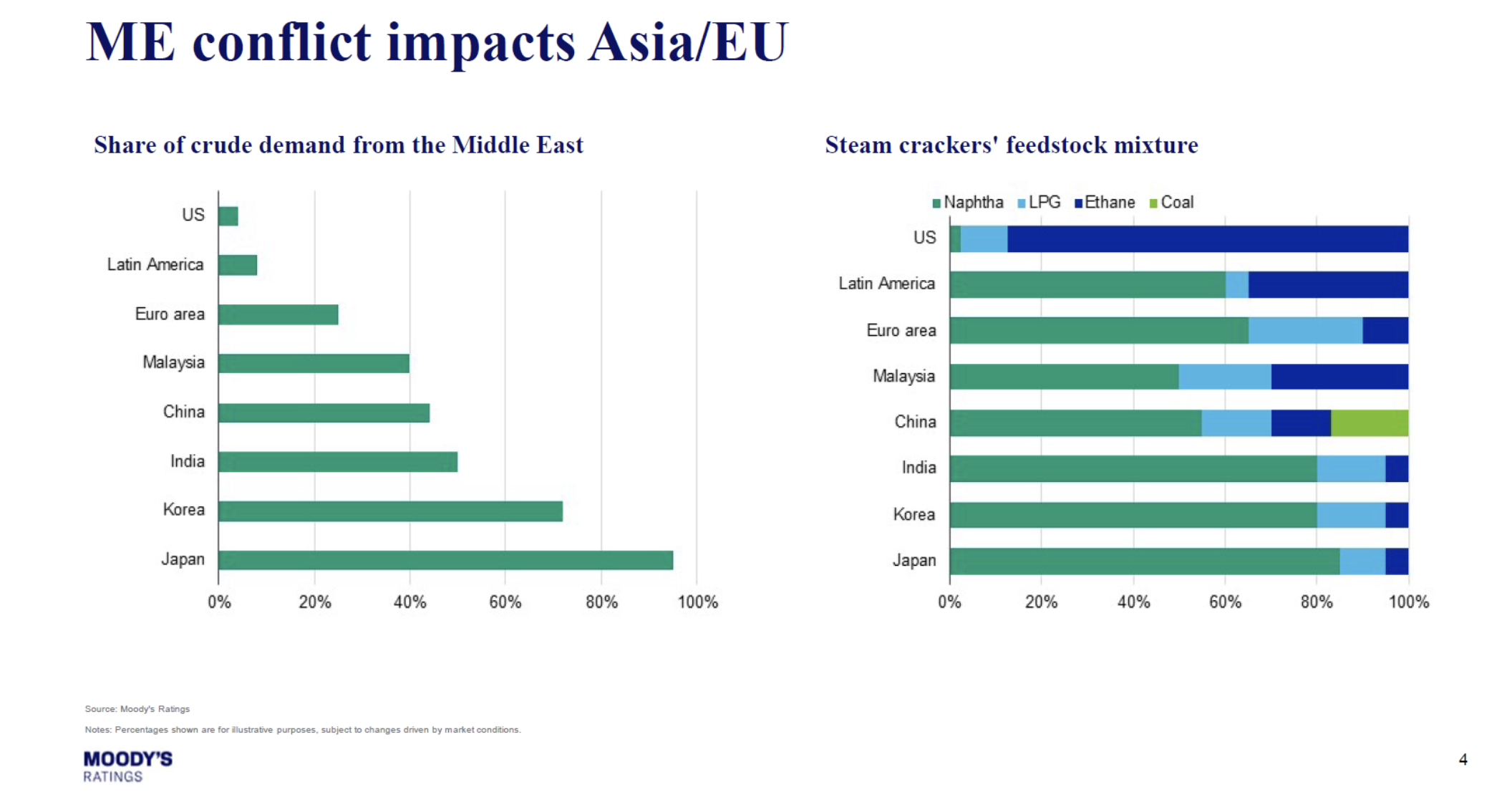

Asia's fatty alcohol ethoxylates (FAE) market. is experiencing a downward price revision for spot offers due to decreasgin feedstock costs for fatty alcohol mid-cuts. Demand remains largely muted, with buyers retreating to the sidelines amidst global economic stagnation, inflation concerns, and geopolitical tensions in the Middle East, which are also driving up fuel and freight costs. Spot trades are limited to small, needs-based parcels. The market outlook remains uncertain, with continued US-Iran war weighing on demand and buyers expected to remain on a need-to-buy basis. Upstream, Malaysian PKO prices have fallen, and demand for mid-cuts is waning, while China's ethylene oxide prices remain flat with suppressed demand despite tight feedstock supply. China's factory activity, however, saw expansion in April.

Global fatty alcohol markets are showing varied trends across regions. In Asia, mid-cut and long-chain prices are softening due to declining feedstock PKO and weak demand, compounded by geopolitical uncertainties and holiday lulls, though short-chain grades see price increases from improved demand. Spot availability is limited by plant maintenance. The US market is finalizing Q2 contracts with upward price pressure, driven by rising feedstock and input costs from geopolitical conflicts that are also lengthening lead times and reducing spot availability, despite ample supplies and below-average demand. A new universal tariff scheme adds further complexity, though its full impact is still unclear. Meanwhile, Europe is experiencing record-high spot prices for mid-cut fatty alcohols, supported by persistent supply constraints and high feedstock costs, even as PKO values trend downwards. Q2 contract prices in Europe also reflect significant increases due to these pressures, and the region is anticipating potential linear alkyl benzene shortages and ongoing petrochemical supply chain disruptions.

The Asian linear alkyl benzene (LAB) market is gaining in price level, driven by tightening supply from plant output reductions and soaring feedstock costs for kerosene and benzene. Despite strong buyer resistance to escalating prices, some are accepting higher numbers due to urgent needs, while others retreat from the market. India's import and domestic LAB markets are also rising amidst persistent supply shortages. The downstream LAB sulphonate (LAS) market in Southeast Asia is firming aggressively, with prices surpassing LAB values as a bit of a buying frenzy takes hold due to anticipated near-term shortages and disrupted sulphur supply. Global geopolitical tensions continue to severely impact crude feedstock availability and logistics, contributing to the supply crunch and elevated prices across the value chain, further compounded by various plant maintenance shutdowns in the region. Ouch!

The Music Section:

It doesn't seem like I’ve listened to much this month. Apart from of course this song – in three versions

I’m told this is the original by the Temptations.

People seem to like this one better – by Edwin Starr.

This is the first one I heard, back in the day. And hence it is my favorite. Frankie Goes To Hollywood (Extended version for you. No extra charge! Super bass line.)

That’s it. Hey look. Do yourself, your company and your career a favor and join me in Jersey City this week (Wednesday start). http://events.icis.com/website/8544/